2022: Staying The Course

2022: Staying The Course

Investors who've stayed the course have vastly out-performed those who haven't

Good morning! This issue is meant primarily as a pep talk and a discussion on indexing, using mutual funds, as well as when and if to use Vanguard, Fidelity, or even TD/Schwab. I share my thoughts here, without backspacing or any editing, just some occasionally images pasted in to keep things moving. I’ll come back and fix typos and re-edit if I have the time and feel like it.

The #SPX is down -5.16% YTD

While it’s been a rough year, the #SPX cash index is only down -5.16% after being down -12.49% just 10 days ago. That’s a 7% return in only 7 trading days. Over the past six months, the average retail account is now down approximately -32%. That’s absolutely brutal.

I often talk about staying invested, as the market tends to go up sharply right when the least number of investors expect it. This is, essentially, why market timing never works out for investors. If you’re still trading with anything more than a funny money account, I beg you to reconsider. If you’re trading, make sure to log everything. You absolutely *MUST* be tracking to see if you are beating the S&P 500, and you better be beating it handily. If not, you’re better off relaxing or working another job, or just saving a bit more.

We all want to think we’re the exception to this rule, but the hard fact is that we are not. We all want to be smart. We want to be special. We want to “figure it out”. For a while, I thought I had everything figured out, with all of my funds running successfully. But even as a professional, I can’t possibly know if my “skill” is luck or actual skill. I am not prepared to bet my retirement on it if I don’t have to. I don’t have to. So I won’t.

As Jack Bogle has said, “I don’t know a single person who’s ever been able to time the market consistently. In fact, I don’t know a single person who KNOWS a single person who’s been able to do it consistently.”

I agree with this 100%, and I’m in the rare group of people who were lucky enough to successfully time the market, both exiting and entering, on multiple occasions. Do I think I’m a good market timer? No. I think I’m brutally lucky. There’s no way for me to prove otherwise.

When the market began it’s drawdown in 2022, I knew the #NDX was overvalued, and merely made sure my assets were shifted to value. While this is a form of market timing, I sin a little from time to time. As the markets were down to -12% or so, I rotated back into a more traditional S&P 500 allocation, as growth appeared to be oversold relative to value, and I was worried value would underperform after such an excellent performance vs. the index.

Fortunately, I was right. But I’m not sure it was the right thing to do. Switching from value to the S&P to growth is all a form of market timing. While I try to keep most of my portfolio in the S&P 500 for domestic allocations, I’m certainly guilty of using value and growth funds when I see the factors gaining momentum. This is something I need to work on myself.

Where To Invest?

")

I tell everyone to use Vanguard. They have no profit motive. They have the best selection of funds at the most competitive fees. I know they’re going to be there with their low fees, excellent service, perfectly managed funds, the most academically robust research behind their indexing methodologies, and I know they’re not going to get bought out by Blackrock or JPM or Schwab or another big player.

When it comes to my retirement, I will certainly look around at other ideas, but it’ll be Vanguard I use to handle my RMDs and glide path into retirement. While I’d use a target date fund, I prefer treasuries to corporate bonds, which brings me to another subject.

Does Fidelity Fit In Anywhere

Fidelity does fit in. Unlike Vanguard’s $3,000 minimum investment for most mutual funds (it’s only $1,000 for their Target Date series and STAR Fund, the latter of which invests in many different Vanguard-managed funds, most active), Fidelity has a $0 investment minimum.

While Schwab/TD also have low-fee index funds, they have a much longer lock-in period on funds and they charge $25-75 for outbound ACAT transfers. You do not want to be with a brokerage that charges for ACAT transfers. The only brokerage who will cover your ACAT charges that DOESN’T charge ACAT fees themselves is Fidelity. This is typically for accounts with over $25k in assets, although they’ve been known to do it for less.

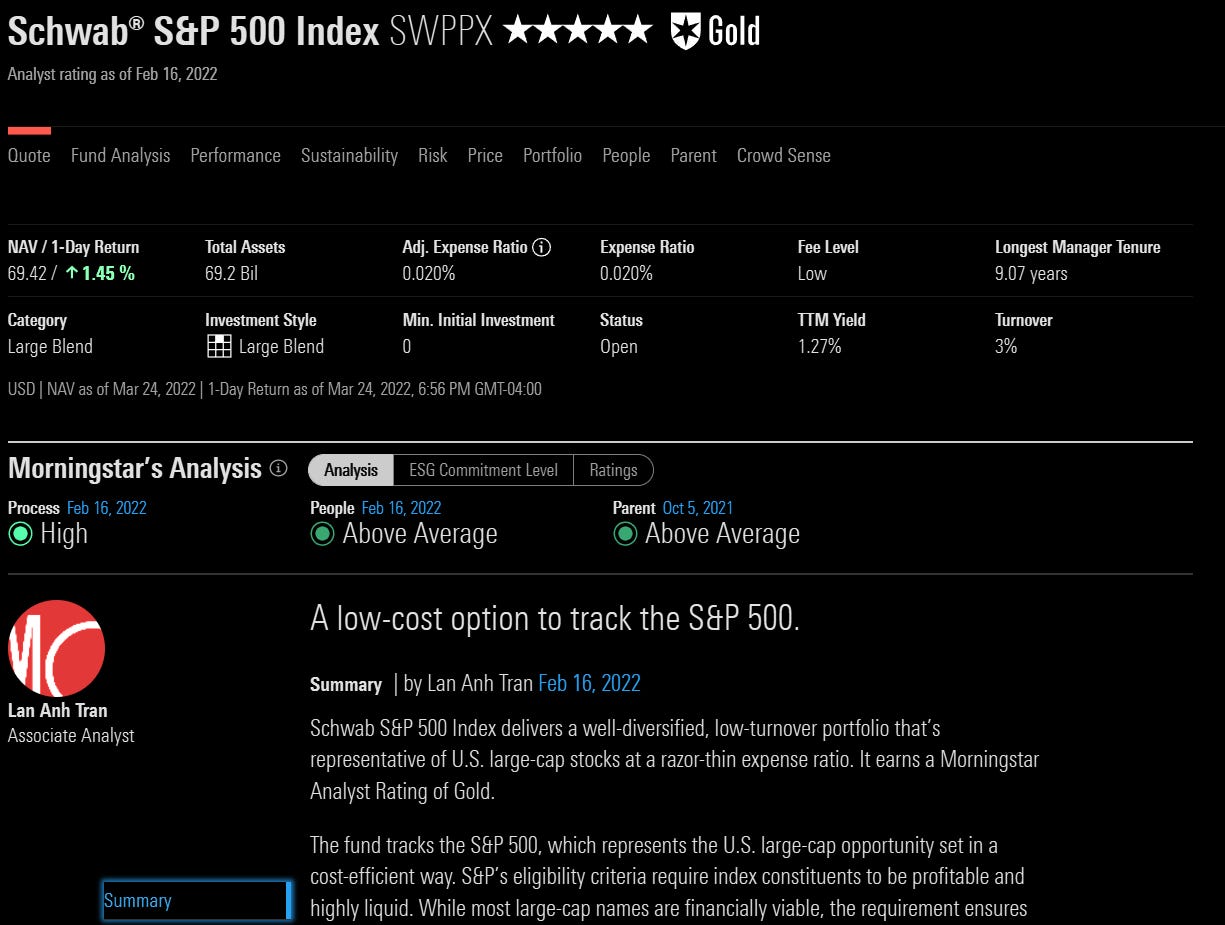

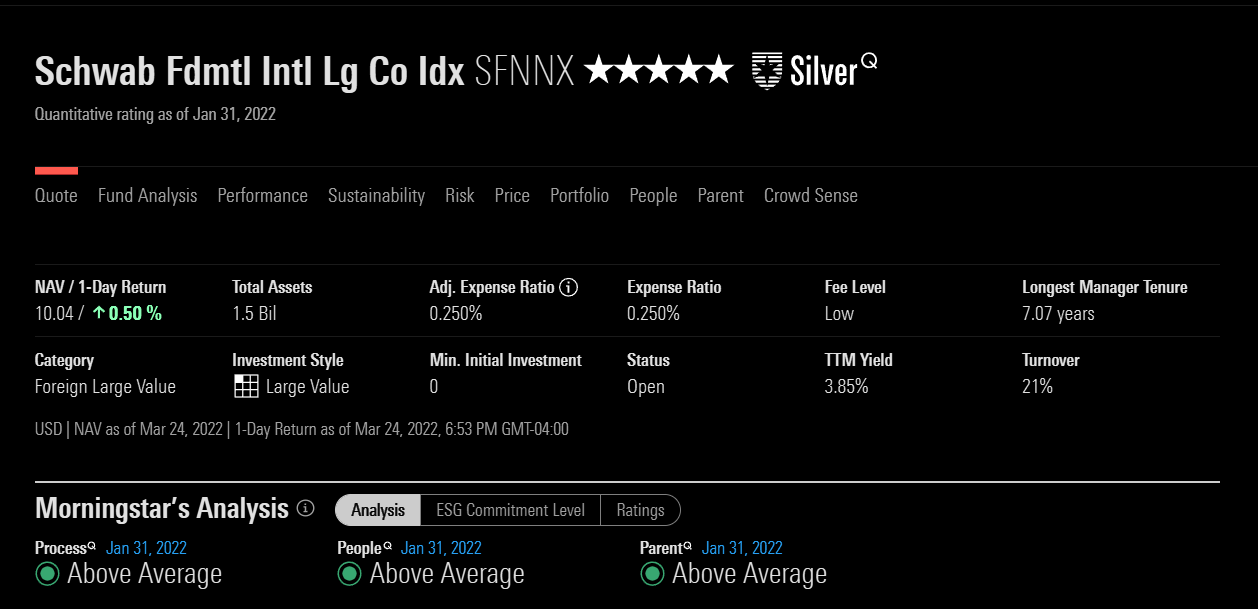

So, if you’re with Schwab/TD currently, go ahead and take advantage of their index funds like $SWPPX for the S&P 500 and $SFNNX and $SWISX for international funds. Unfortunately, they only have a handful of funds. Fidelity has a wider selection of low-fee index funds. (Vanguard’s entire line-up is low-cost, even their active funds. Expect to pay 3-6x as much for active management with Fidelity/Schwab vs. Vanguard. You may want active management in the future, and your goal is to get to Vanguard one way or another so that you have the most robust selection and the most efficient and well-run funds on the planet).

With Schwab/TD funds like the ones mentioned, you can build up an account to $25k and then have Fidelity reimburse your ACAT transfer to them. This will let you access Fidelity’s fund line-up, $0 minimums, and the ability to trade between funds freely.

If you sell out of a fund with Vanguard, there is a 30 day cooldown before you can buy into that fund again. This helps protect the fundholders from unnecessary buying/selling to meet redemption and purchase requests. Schwab/TD have a 90-day lock-in period whenever you buy a fund, which is more restrictive. They also have a $50 fee for anyone who dares sell a fund before 90 days. Vanguard never charges for this; they just prevent you from buying BACK into the fund.

So, away from Schwab/TD you go. Make sure Fidelity pays for that nonsense, though.

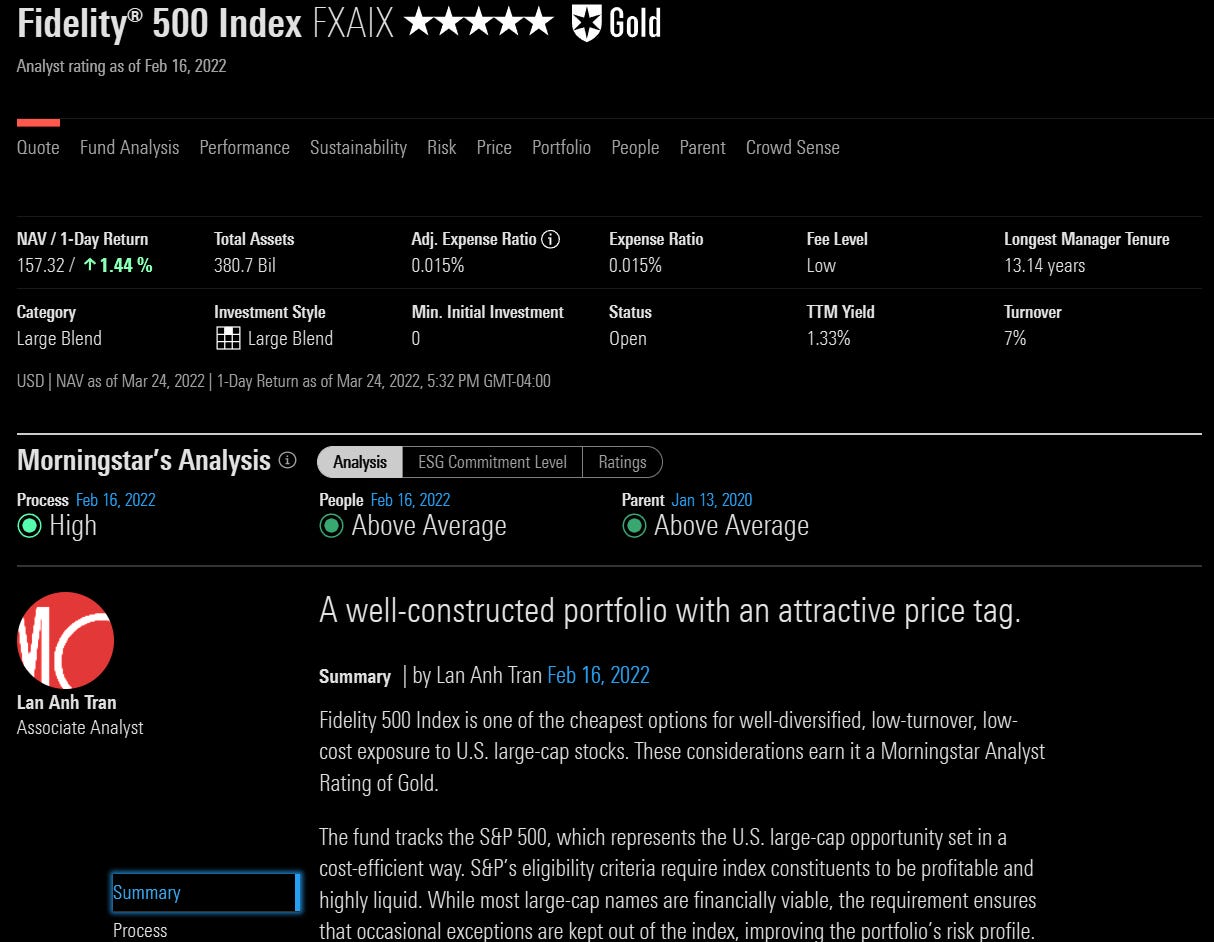

Once you’re with Fidelity, you may need to wait for your 90-day cooldown from any Schwab/TD funds you’ve purchased to elapse. You can put any new money into $FXAIX or $FSPSX for the S&P 500 or international indexes. They also have low-fee factor funds, like $FLCOX for large value. These are, in my opinion, where Fidelity starts to become less appealing than Vanguard.

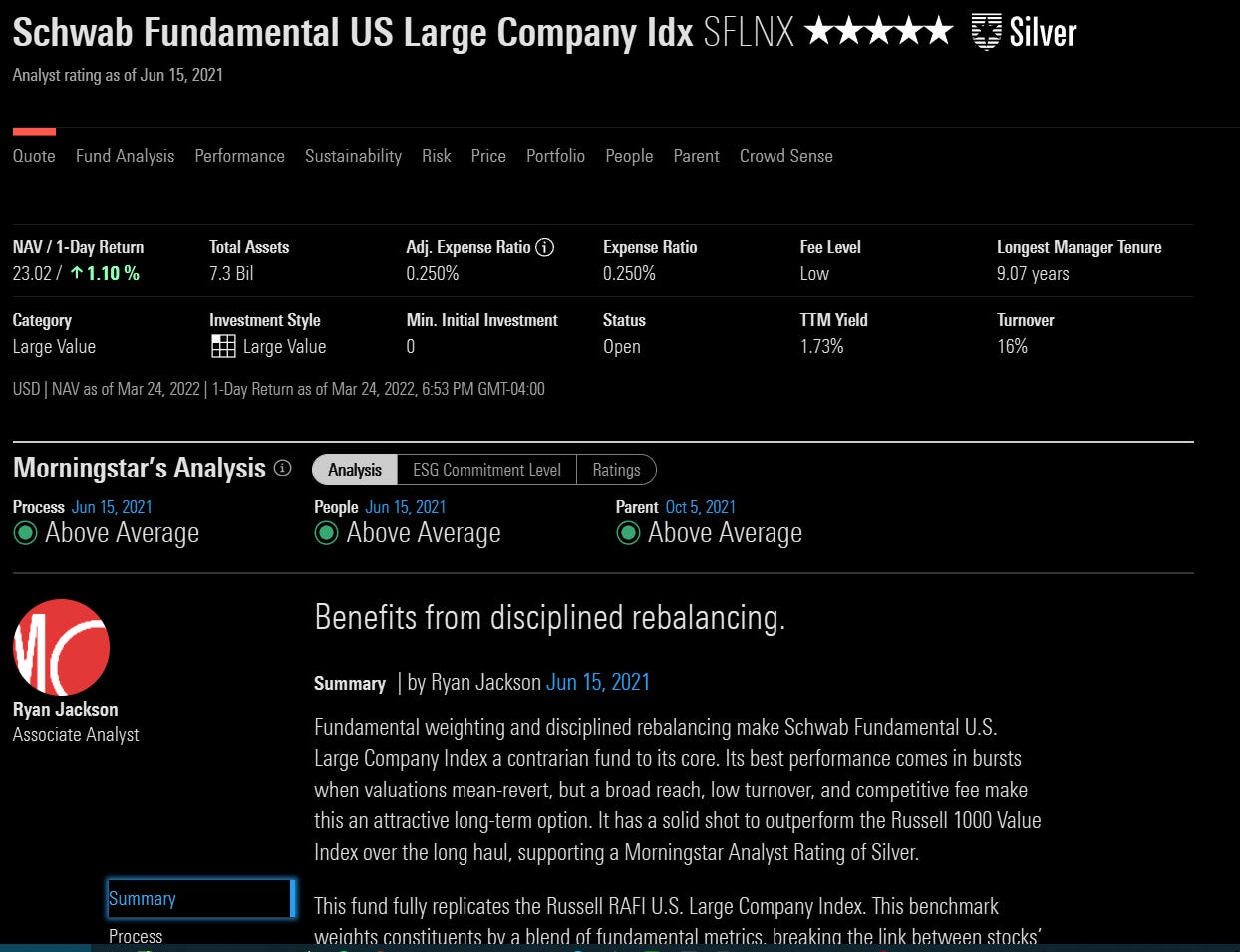

While the most basic funds have a cost advantage, and there are even zero-cost options, Fidelity’s factor funds aren’t as well-run. Schwab’s index funds, especially $SWISX, have too few holdings with only 750 or so. The equivalent Vanguard fund holds ~6000 stocks), have no cost benefit over Vanguard, and slightly underperform their Vanguard counterparts. Fidelity’s international funds hold 2500+ and are much more diversified than Schwab’s, so I’d rate them as the “next best” option to Vanguard’s offerings.

That said, while building an account to a higher balance, or if you’re unsure of allocations, Fidelity’s frequent trading policy can be the most lenient, and their $0 minimums means you don’t need to transfer $3000 to get into a new fund. With Vanguard, if you want to put $500 into a fund, you’d need to first put $3000 into it, and then withdraw $2500, getting locked out of the funds you transferred out of for 30 days. (You can always make automatic contributions to funds, whether in cooldown or not).

As for active funds, Fidelity has a lot of closet index funds that charge truly ridiculous fees, like 0.89% for a sub-par large value fund. On the other hand, Vanguard has multiple funds that charge ~0.28% and these funds have out-performed their Fidelity counterparts. Fidelity has more funds in total, with funds for things like Latin America, as well as Natural Resources. They charge a lot for these funds, and there are always ETFs better suited to the task, unless you specifically want active management. Vanguard doesn’t like to maintain funds with only a single sector or theme, although they do have Energy, Healthcare, Real Estate, and Technology mutual funds. With Vanguard active funds, they don’t rely on single managers, but instead use multiple teams of managers. Many funds are also complemented by Vanguard’s Quantitative Equity team, which keeps costs lower and helps increase the risk/reward of funds, often with many smaller holdings.

When value or growth are in the driver’s seat, outsize returns can be generated using the right actively managed fund. As IRAs don’t have access to leverage, an actively managed fund can invest in more highly levered companies in the growth/value space. From 2009-2020, Vanguard’s US Growth fund had astonishing returns. Since then, their Windsor fund has beaten value benchmarks and done well, and is up ~4% YTD. This kind of out-performance vs. the S&P/TSM can be achieved at Vanguard (almost exclusively), by combining a value or growth index fund with an actively managed value or growth fund. This is an advanced strategy, and requires a lot of planning, but does generate outsize returns.

Fidelity has too many funds, most of which aren’t able to match their low-fee ETF counterparts (Fidelity’s Latin America fund brutally lags behind the $ILF ETF, while charging more than double the fees.). Fidelity seems to appeal to people who like to go “mutual fund shopping”, and they’ve even made it easier to trade frequently.

While this flexibility is nice, especially in smaller accounts, you need to have a goal. Fidelity allows transfers under $10,000 between funds once per day. This can be useful when you’re getting your allocation set, but it shouldn’t be necessary once you’ve arrived. Once you’ve settled into an allocation, you’re going to be best served by Vanguard. If anyone’s thought of “everything”, it’s Vanguard.

“Off to Vanguard We Go!”

| A-Z Quotes")

Once you’ve gotten to Vanguard, (an ACAT from Fidelity or IBKR is free) you should already have your asset allocation determined. Vanguard has far more low-fee blend funds to help you achieve your allocation using far fewer funds than you would with Fidelity (or Schwab, which only has 6 or 7 index funds). Vanguard has a fund for everything, and the costs have always remained competitive.

- Quotefancy")

Currently, Schwab and Fidelity are losing money on their S&P 500 index funds to draw customers away from Vanguard. It’s okay to take advantage of this by using Fidelity, but ultimately, the difference is miniscule, and Vanguard should remain the end goal for as long as they serve fundholders first. (Fidelity/Schwab/etc. are for-profit and will always put their profits before yours.)

For quite some time, $VWNDX (Vanguard’s Windsor Fund, active value @ 0.28% expense ratio) has been beating up on $VVIAX, or Vanguard’s large value index fund. As such, I’ve combined it with $VIGAX to gain some alpha on the S&P 500. When growth is leading the market, this strategy works well with $VWUAX. For international funds, there’s no growth/value indices, only active funds. However, $VTRIX for international value and $VWILX for international growth have both delivered incredible returns when the time is right.

That all said, you’re probably best off investing in index funds. But it’s good to know that you have options, and that they’ll cost you a tiny fraction of what Fidelity, Schwab or, heaven forbid, some other firm may charge. (I had a small account with Putnam and after all their fees, I was paying nearly 1.5% a year. This was in 2021!!! I finally got them to ACAT my account to Fidelity. They have some great funds, but NOTHING can make up for 1.5% a year! I’m paying 0.04% at Vanguard, 0.015% at Fidelity, and 0.025% at TD with a bit of funds in a 0.25% fund.)

Vanguard is also notorious for having multiple yet similar funds to switch between for tax purposes or cooldown purposes. For example, if you trade out of $VFIAX, the Vanguard 500, but you want to get back in there, you can simply use $VLCAX, which holds the top 550 stocks instead of 500. It’s virtually the same. This also works if you have a large taxable loss in $VFIAX or $VLCAX. You can also combine $VVIAX and $VIGAX to re-create $VLCAX, or you can use $VTSAX for the total market. They even have a mega-cap index that holds the top 250 stocks! If it’s useful for you as an investor, Vanguard either already has it, or is likely planning on it.

I swear, Vanguard has options for everything. As always, you can have them convert your funds to ETFs if they’re index fund mutual shares, which may come in hand in retirement. However, ETFs shouldn’t be traded, only bought. This will take some serious discipline for most people reading this. Sorry!

Personal Investment Plan

When you’re read to head to Vanguard, you want to write up a Personal Investment Plan. This should say exactly what you want to do with your assets from now until retirement. This is the document you will look at when everyone is going crazy, when the market is in a brutal sell-off, when the next $ARKK fund comes along and you feel like you’re lagging your neighbors.

(Bonus: You’re not. Index investors absolutely OBLITERATED the returns received by average retail investors, particularly ARKK investors. The more you index for a low cost, the better you will do. This is an indisputable fact.)

Your Personal Investment Plan should be written with the assistance of a fee-only financial advisor who can act as a fiduciary. This plan is something you write for yourself, like a mix between a personal journal and a prenuptial contract. If your brain decides to divorce your body, your body gets to keep all the mutual fund money without your brain freaking out and selling it all at the lows.

Your plan should include:

Asset allocations, US/international/EM/value/bonds/treasuries, etc.

Glide path: how your allocation will change with age. Usually this is just a ratio of equities to FI. Example: “At Age 45, I will increase my fixed income holdings from 7% treasuries to 10% treasuries.” This means you are about to sell 3% of your portfolio, equities only, and buy treasuries with it.

Reasons. Reasons. Reasons. This is crucial. Are you going to invest in small value? Write down all of the reasons why. Did you commit to always buying and holding? Write down the reasons why that’s a good idea.

You will go through periods of time where the news, your friends, family, your emotions, personal finances, job-related stresses, husbands/wives/children, and others can put you in a fragile state. This is the exact time where you go back to your Personal Investment Plan.

For these reasons, you really need to get your PIP in the best possible state.

Example PIP

My equity allocation will be 50% S&P 500, 40% Total International Stock, 5% Small Cap Value and 5% Emerging Markets.

My fixed income allocation will be 70% long-term treasuries and 30% short-term treasuries. No corporate bonds, not investment grade or high yield.

Glide path:

For my equity/FI mix, starting at age 36, I will divide my age by 6 to determine my fixed income percentage. (36 = 6%)

At age 44, I’ll divide by 4. (44 = 11%)

At age 51, I’ll divide by 3. (51 = 17%)

At age 65, I’ll divide by 2 (60 = 30%)

At age 72, I’ll divide by 1.5 (72 = 48%

At age 80+, I’ll divide by 1. I want to hold 20% equities to pass on to my children.

I am going to rebalance once every 18 months starting on October 15, 2022. If any asset is off by 20%, then I can rebalance then, too.

I am investing in international stock to diversify my returns. I don’t know when or how international stocks will outperform. I know that they have before. I know it reduces volatility and risk. This is why I’m investing 40% in total international stock.

I’m investing 5% in small cap value because studies say it can outperform the S&P 500. I’m not sure if it will, so I’m only putting 5% in there. I know that small cap value is volatile and can underperform for long periods of time. If this happens, I’m just going to stick with it. The dividends are pretty good. And hey, it’s better than fixed income returns!

I’m also putting 5% into EM stocks. While I’m not a huge fan of China, they’re the biggest country and growing fast. This will also reduce risk and diversify my equities. In the 2000’s, EM stocks went up faster than anything else. It’d sure be nice if that happened again! I also know that countries like China and India have very large populations and could have a greater growth potential than a mature economy like the USA.

I am holding treasuries for fixed income, 70% in long-term and 30% in short-term treasuries. I do not want to be on the wrong side of the deal. Corporate bond holders get the worst deal from companies. There’s default risk and the possibility of prepayment or bonds getting called. I barely even understand how that stuff works! I know the US government will always pay 100% of the interest, and has never missed a payment. There’s no default risk. If the US defaults, then I’ve got bigger problems! (You can substitute the US with any other country with a reserve currency.)

Only equities beat inflation over 30-year periods, so I want to keep my equity allocation high. If the market starts crashing, I can’t change my allocation! The market crashes all the time. There’s bear markets all the time! It’s going to hurt, but I’ll just follow my plan. Everything will turn out okay in the end. Capital markets always figure out a way.

If capitalism ends, then it probably means that the Zoomers have turned society into a utopia where I never need to worry about money again. Good job Zoomers! They may seize my money, but at least no one will ever have to worry about saving up for retirement again. That was scary!

My husband/wife has a panic disorder. When the market crashes, they are prone to panic/anxiety. I need to be strong for them, but I won’t sell any assets. I will tell them about my plan, and how I need to keep depositing 15% of my paycheck each week, no matter what. I will be supportive of them but I will stick to this plan, too. I want us both to be safe, and I know they will understand when they are feeling better.

The market is going to be scary. I am going to be scared. I’m probably going to want to sell it all. I’m going to see hot new stocks and funds going up 9,837%, but I won’t buy them. I decided on my allocation, and I’ll stick to it.

I will be offered many new investment products, but I won’t buy any without first consulting a fee-only financial advisor. This is an advisor who doesn’t profit off of products, but only by giving me sound advice.

To avoid over-trading, I will only look at my balance statement once per quarter, beginning when I file my taxes.

I will deposit $100 per week into a Roth IRA which will use the same allocations.

Everything is going to be okay. Do not panic. Read this, and add any new wisdom to it when needed. Do not give up on your plan. Stay the course! You’ve got this!

For my husband/wife if they panic: Honey, I wrote this in March of 2022. I want you to know that I planned for this. There will always be times where the market crashes, and it will always feel different. We’ll always have many reasons to sell our stocks and bonds. But we won’t do it. I need you to trust me. I love you very much. Please trust that I have done everything in my power to ensure a secure financial future for us and our loved ones. I don’t know how things will be okay, I just know that they will be okay.

(Write something about how much you love/appreciate them, maybe? Up to you. It might calm them down.)

Your list should be long and exhaustive. Remember, you’re going to be reading it when you’re at your worst, when you’re most emotionally vulnerable. You want your Personal Investment Plan to be your best self, telling you “HEY! I FIGURED THIS OUT! I WORKED HARD ON THIS! DON’T WORRY ABOUT IT.” You will figure it out, and you will get it.

What Next

I usually tell people to use Vanguard’s advisor services when they’re in their 50’s to ensure they’ve figured out how they’re going to take distributions in retirement. I also recommend using Personal Capital and/or Mint’s financial planning tools. Fidelity’s “Full View” and Personal Capital have the best retirement planning assistants.

Personal Capital tries to sell an advisor service. Don’t sign up for these. You do not want or need a robo-advisor! They suck and cost way too much. Wait for them to be free, then MAYBE they’ll be worth it. Still, probably not.

That said, I’m not going to talk to you about retirement. Let’s try to get you there first. For 99% of investors, that means one thing: you need to swallow your pride and start indexing ASAP. I don’t care if you made 500% this year. I don’t care if you made 2000% last year. I’ll bet you hard money that I’ve done far better than a piddly 2000% return.

It doesn’t matter. I got lucky. You got lucky. It’d take us 36 years to find out otherwise. I’m indexing. You’re indexing. We’re all going to index. Let others pay exorbitant fees to collectively underperform the index. There’s no other mathematical possibility.

The totality of returns will be split evenly among actively managed funds, most underperforming after all the trading costs and ridiculous fees. Imagine paying for Blackrock to run advertisements in your expense ratio! Let all the traders trade. Maybe you need to delete your twitter account. Maybe you need to open a small $2k margin account where you only trade $SPY, $QQQ, $VTV, $DIA, $VUG, $VXUS, $VEA, and $IEMG? At least, that way, you’ll always be invested in SOME kind of index, even if your awful trading screws it all up.

And it will. We can’t trade forever. If we could, it’d be too stressful.

So, please stop. Index returns are enough. If not, try saving an extra 1-3% a year, and you’ll do better than literally every fund, active or not. Pick up a side-hustle. Try to do ANYTHING that isn’t trading. It’s simply a waste of time. It’s exciting, but if you’ve got a small account to exorcise your trading demons, then you can do that kinda thing WHILE you’re working. You can do it while you’re working out! I trade at the gym all the time. Mostly small accounts.

Ideally, you will have 98-100% of your assets following your plan, staying invested your entire life, and having a wonderful retirement.

Wishing you all a lovely Friday, a blessed weekend, and thanks for reading this stream of consciousness. Let’s resolve to index more and stay the course. It’s perfectly fine to just ignore the markets for a week. Try it out, see how it feels. Make sure you’re indexed and your allocations are set before hand. If so, you don’t ever need to check the market!

—Avery

P.S. There are many one-fund solutions, which I need to evaluate. Currently, I like the idea of using $VTWAX for total world stock and a treasury fund for fixed income like $VUSTX. Fidelity currently offers some Freedom Index funds (target date funds) that incorporate treasuries and TIPS in addition to corporate bonds, which I’m still investigating. They may be slightly better than Vanguard’s, but shouldn’t do anywhere near as well as $VTWAX + $VUSTX (or $VFITX, etc), let alone a smart allocation between $VFIAX, $VTMGX, $VEMAX (and $VUSTX or $VFITX).

Epic, Avery. I surrender.

great coverage