A Brief Note on Value

A Brief Note on Value

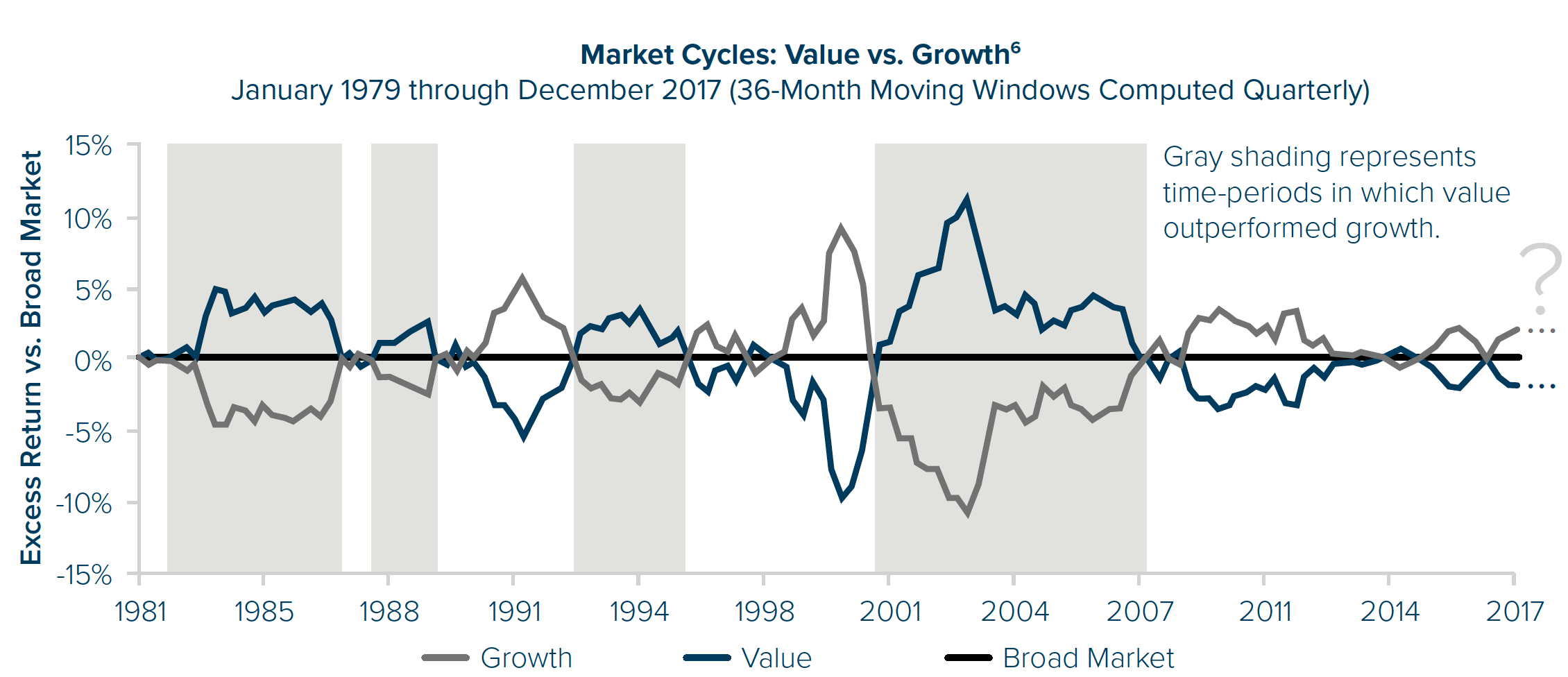

Over time, the Value Factor has consistently outperformed the market

Many investors are experiencing their first market wherein value stocks are consistently outperforming their growth counterparts. The value factor is notoriously volatile and unpredictable. Personally, I prefer a value-oriented portfolio, but will tend to invest large amounts in regular cap-weighted index funds. From there, I like to identify certain value funds that I like, and can tolerate periods of underperformance from.

Significant tax breaks, a lack of regulation and regulatory enforcement, monopolization, and the commodification of internet traffic and connectivity, resulted in a decade-plus long run for growth stocks, during which they beat the market. This isn’t the first time we’ve seen this happen.

It’s during market meltdowns like the one we’re currently experiencing that growth-investing acolytes are reminded, in no uncertain terms, why the growth factor has delivered a negative risk premium compared to the broad market. While international value stocks are sitting in positive territory for the year, many growth companies have lost 50, 75%, or more of their value in a short period of time.

A famous book called “Margin of Safety”, written in the 90’s by Seth Klarman, lays forth many of the principles of value investing. It’s a difficult book to find, but a PDF copy isn’t too hard to come by. Simply by looking at the title, we can glean a bit of information.

Investing in companies trading at attractive prices afford investors a “margin of safety” and can/do deliver increased returns without taking on too much uncompensated risk. In fact, one of the few risk factors with value investing, is that it does go through periods of underperformance, and those periods can be incredibly painful.

This leads to many people abandoning the value factor, and if studies can be relied upon, investors tend to make this decision at the most inopportune times. For example, many value investors abandoned their principles and sold issues and fund shares of robust, profitable companies, to instead invest in a portfolio of dot-com stocks, with many losing 80% or more of their invested capital. Only then, did they return to value investing: far too late, and often in time for another period of growth out-performance.

Many investors fell for the tech bubble, and it’s this sort of fate that often befalls growth stocks. By their very nature, the only means for investors to profit is through the “greater fool theory”, wherein they hope a future investor will pay more for the stock than they did. This is particularly evident with profitless growth companies, IPOs, and small-growth stocks, also known as “the black hole of investing”. Burton Malkiel called it “building castles in the sky” (which I think is an early 2000’s trance song, too).

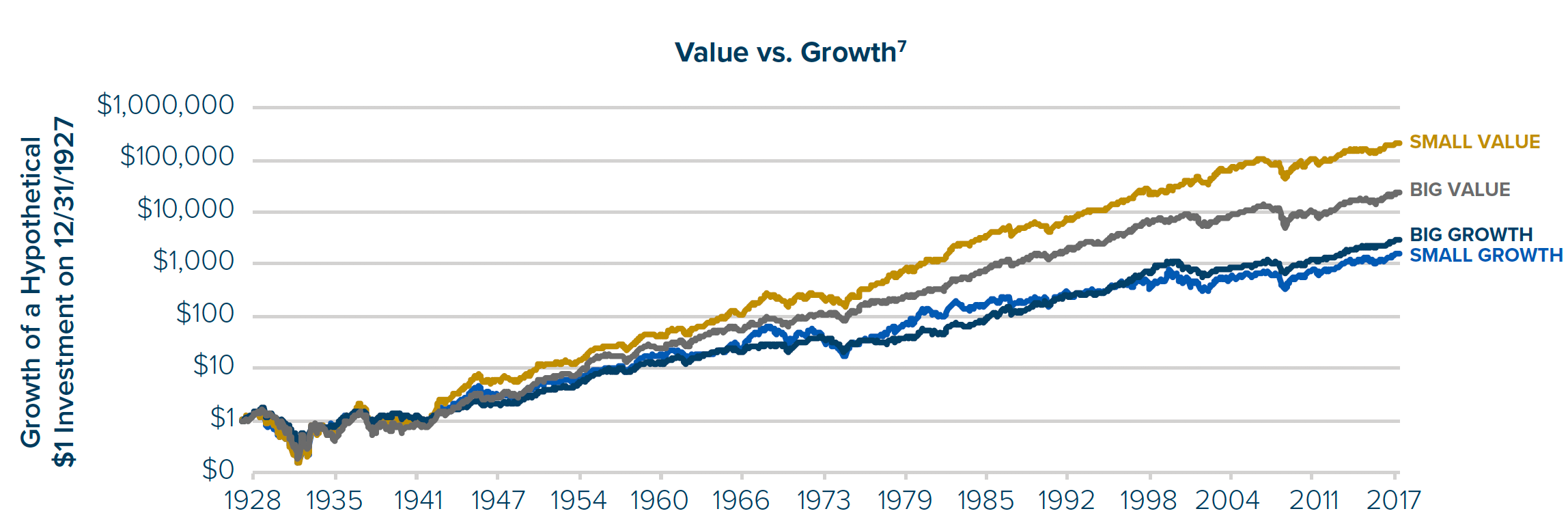

Since 1936, the 2010’s have been the worst for value investors, and this has created one of the widest gulfs in valuations in history between growth and value stocks. Yet, while many people were losing 50%+ chasing growth stocks, assuming they didn’t make any awful trades, companies like Wells Fargo gained nearly 70% in 2021. This went largely unnoticed, presumably even by Warren Buffet, who spent the year selling his WFC shares.

There’s many ways to go about investing in value, and the easiest ways include value ETFs like $VTV, or value-tilted ETFs, like $AVUS or $DFAU. Avantis (founded by ex-DFA board members) and DFA have specialized in value-tilted portfolios. Another method, and one I use, is investing in active value funds. While I don’t recommend this, it’s something I enjoy, as I like to deconstruct portfolios and the management’s decisions to find funds that I like. That said, there’s no academic backing to investing in actively managed funds, as there is with simple value index funds.

Personally, I like to use Vanguard’s $VWNDX (Run by Wellington/Pzena) and Dodge and Cox’s $DODGX for US value, Vanguard’s $VTRIX, $VWICX, and D&C’s $DODFX for value and value-tilted foreign exposure, and $DFAE or $DFCEX from DFA or $VMSSX from Vanguard (run bye Baillie Gifford, Wellington, and Pzena Management) for exposure to emerging markets.

Outside of that, I prefer to use large-cap index funds, with a small amount of money in less traditional funds that use fundamentals or cash-flow screens to create their own proprietary indices.

I’ll leave you with a quote from Anchor Capital, a value investing outfit that’s been in the market since 1984:

As value investors for 34+ years, we at Anchor Capital have witnessed many periods where growth has outperformed value, including the technology bubble in the 1990s. In all that time, the firm has stayed true to our value-oriented approach and discipline, knowing that value has outperformed growth in the long run while providing better downside protection.

During a market boom, even professional investors can get caught up in the fear of missing out. But we believe that the key to success is having patience and maintaining a long-term horizon. We think history attests to the truth of this statement.

That seems especially true in this current market, which seems quite overdue for a change in gears. Valuations are at all-time highs, and earnings growth rates are slowing. Although we are not market forecasters, and never will be, we do believe it best to be prudent in market conditions like this, and to realize that a shift to value is bound to occur sooner rather than later.

The accompanying PDF can be downloaded here: anchorcapital.com/wp-content/uploads/2020/06/Value-verse-Growth_Anchor-02-18.pdf

—Avery