Building a Global Portfolio

Using ETFs or Mutual Funds to create a "proper" Portfolio

I hope you’re ready to read a lot of writing with no backspacing. Consider it a stream of consciousness in text format. 😉

If 2022 has taught us anything so far, it’s the importance of building out a properly constructed portfolio. Following the GFC, the US has had historically low rates. Combined with a lack of antitrust enforcement (let alone antitrust, consumer protection, net neutrality, or any other legislation), US technology companies enjoyed a decade-long ascent to the top of the S&P 500/Nasdaq, and propelled US indices ahead of the rest of the world.

No, I won’t be getting into fixed income allocations today. Equities only. FI allocations are highly dependent on your age and current assets.

Formerly an industrial powerhouse, the United States offshored a large number of formerly unionized workplaces and manufacturing has largely moved to locales with even less regulation and oversight. As such, short-term profits booked by industrials went up, while sustainability and revenue durability has become more volatile and unpredictable.

In 2019, commission-free trading landed in the US, granting many new market participants access to stock-trading, cheap margin debt, and fractional share purchases allowing people to start investing with only a few dollars. From retail flow data, and the now-defunct Robinhood API, we’ve seen a distinct trend: Retail tends to be fixated on high-attention stocks, primarily growth, tech, and IPOs.

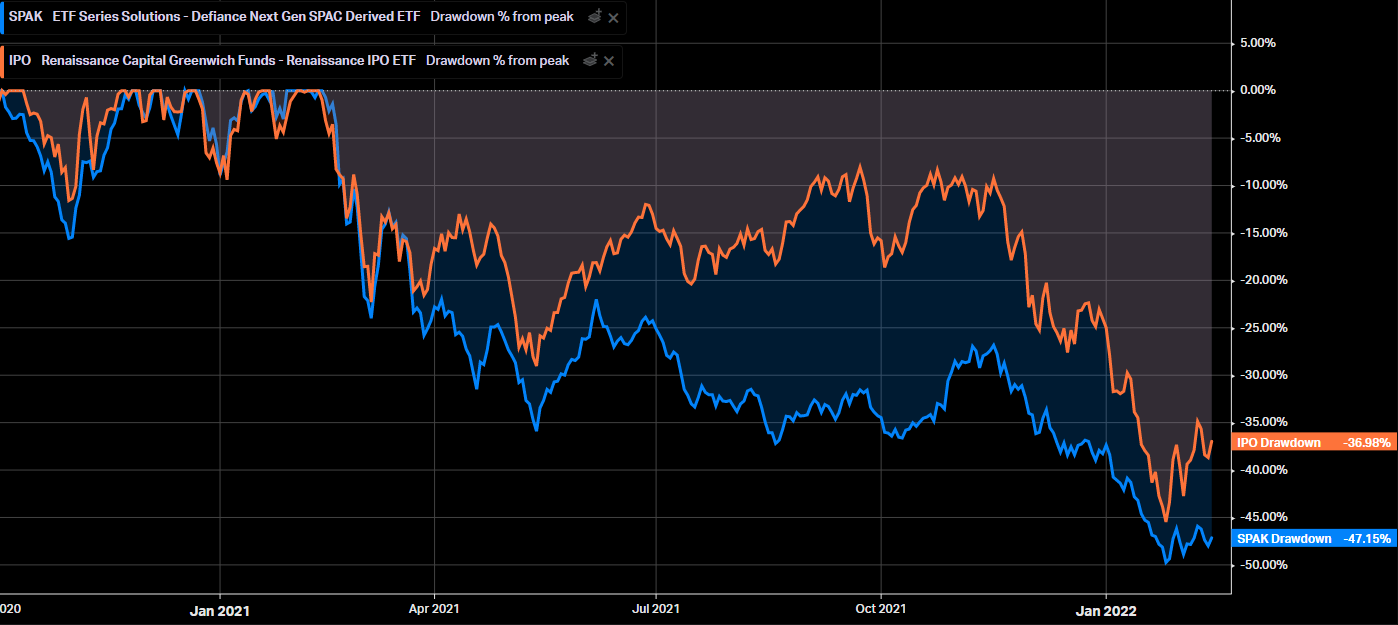

For a while, we even saw aggressive buying (and shilling) for SPACs. This hasn’t gone well for investors.

The Renaissance IPO ETF $IPO and Defiance’s $SPAK ETF are currently in -37% and -47% drawdown, respectively, after improving some. $IPO was down -45%, and $SPAK hit -50%. High-attention stocks have been under intense selling pressure from institutions and “smart money”, as FinTwit/StockTwits attempts to buy each and every dip.

So, let’s take a look at investing in the world of stocks, and avoid hyper-focusing on the hot new product. (Besides, it’ll probably be managed by Chamath and tank -175%. I swear, his SPACs should trade below 0, but I digress…)

For a benchmark, we can use $VT / $VTWAX which holds every tradable security on the planet.

62.20% North America

10.40% Emerging Markets

16.40% Europe

10.70% Pacific

0.20% Middle East

$VTWAX: (Note: Holdings last updated on 12/31/2021, before growth drawdowns.)

The S&P 500, however, is much “growthier” with 36% in growth names, as opposed to the worldwide average of 32%. (Again, from 12/31).

However, if we look at the Total Market Index using $VTSAX, we get a slightly different factor exposure, as more mid and small-caps are added by market weight. We still have 36% growth exposure, but only 29% in large caps, as opposed to 33%.

With small-caps selling off, it may be prudent to allocate more to $VTI / $VTSAX or a total market index.

For international exposure, $VEA for developed markets and $VWO or $IEMG for EM are the most obvious low-fee index choices, with compelling expense ratios and good liquidity.

Some may prefer to avoid EM, and others consider China uniquely risky. At current valuations, it may be worth considering China, or using a more smartly-managed fund for China/EM exposure. $EMXC indexes Emerging Markets while excluding China, although I’m not a fan of that here. $AVEM and $DFAE each offer a factor-tilted exposure to EM, which solves for many of the issues facing investing in China.

While a one-shot buy of $VT or $VTWAX would give somebody full cap-weighted exposure to the entire world, we should be aware that growth can’t outpace value forever, and that value has far outpaced growth over the past 14+ months.

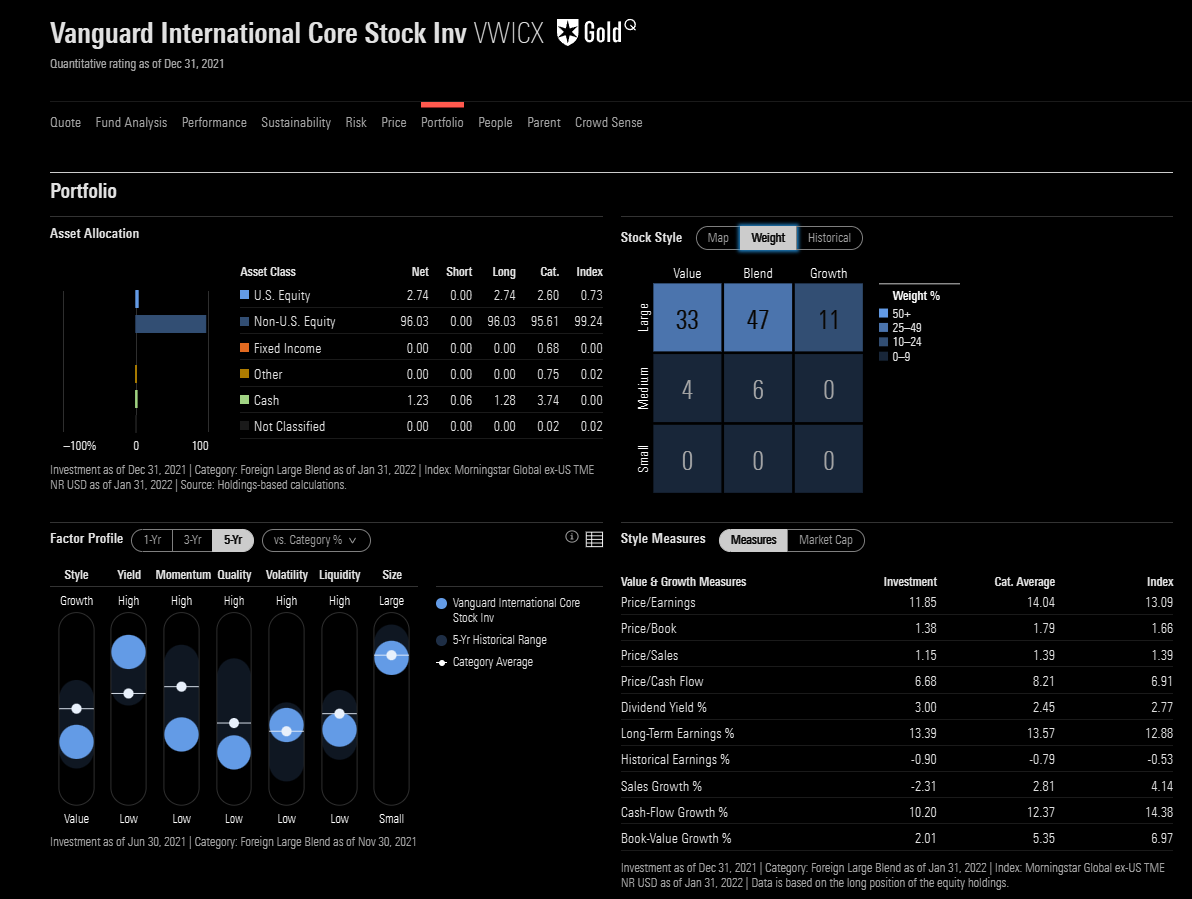

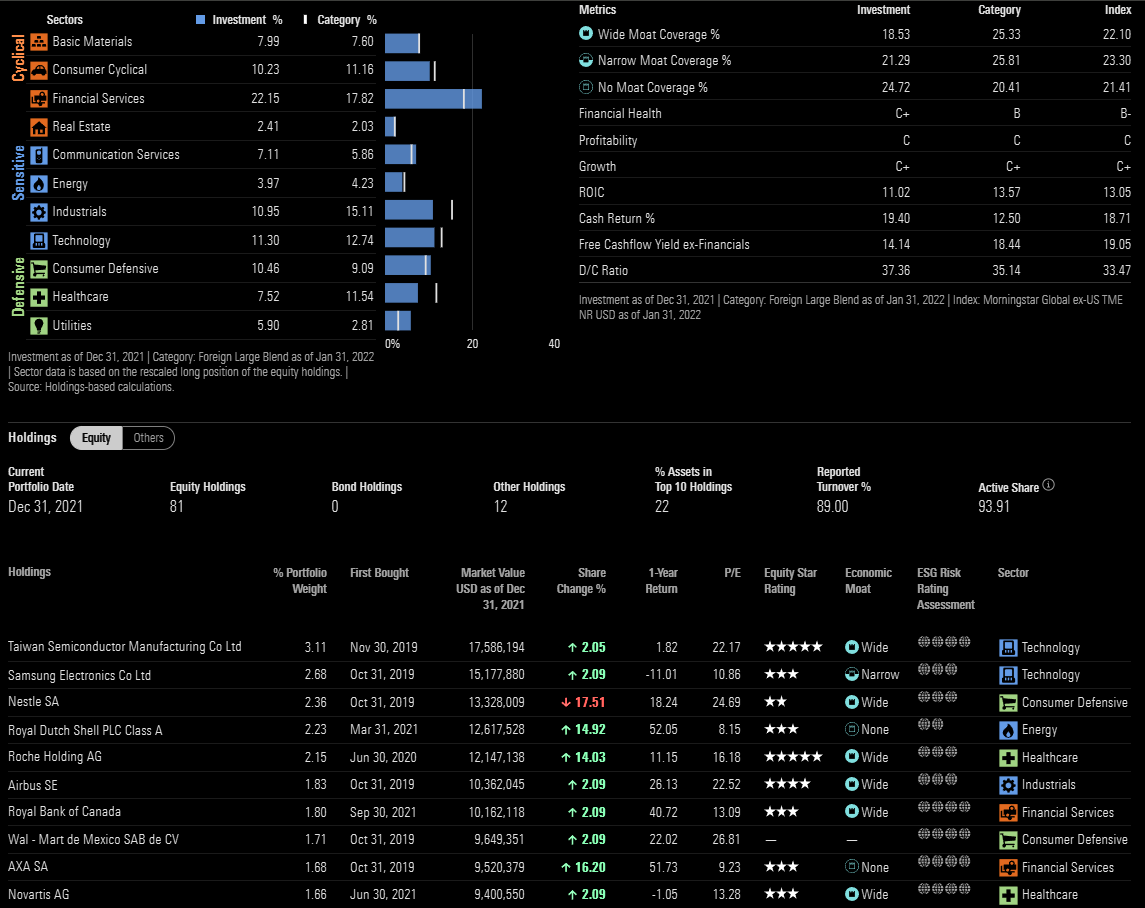

For foreign exposure, I’ve found $VWICX, a newly launched Vanguard fund, to have an excellent selection of securities. For foreign value, $VTRIX offers an excellent management team. Both portfolios are praise-worthy, and a lot of thoughtful construction went into each. $VWICX can act as a replacement for $VEA, and $VTRIX is less expensive than $EFV (EAFE Value).

Let’s take a look at what’s inside $VWICX, and you can be the judge:

I think that a good sample portfolio would look something like this:

$VTI or $VTSAX for US exposure, or $VOO / $VFIAX if someone only wishes to hold large-caps. Either is fine.

$VEA or $VTMGX for indexed Developed Markets exposure seem like the best picks. $VXUS includes both DM and EM exposure.

$VTRIX, $VWICX, $DODFX, or $EFV can be added to ex-US holdings to help balance out the US’s growth tilt without underexposure to FANGMAN stocks. There’s also Avantis International Value, $AVIV, and $IDV for international dividend-payers. $VEA has the tightest spreads, followed by $EFV and $IDV. All have a 1-cent spread most days and trade very close or at intraday indicative NAV (aka “fair value” on the underlying assets).

The value factor is more pronounced in international markets, and with the US in a serious growth drawdown, it’s likely best to stick to a market-cap weighted low-fee index fund for domestic/US exposure. I like using $AVUS and $AVLV for a total market fund and a large-cap value fund. These are all designed for the long-run.

For managing emerging markets exposure, I would use $AVES, $DFAE or $DFCEX for tilted exposure, $AVEM for multi-factor exposure, and $VMMSX for an actively-managed mutual fund from Vanguard. $FNDE from Schwab provides a fundamentally-weighted index, but Avantis and DFA are backed by academic rigor and use back-tested factor weighting. Avantis has the most rigorous screens, and I believe they provide the best factor-tilted funds for long-term investment. The bid-ask spread on many should be taken into consideration, as you can easily lose ~0.05% or more of your invested capital on the spread alone. (This is another good argument for using mutual funds whenever possible, to ensure you receive 100% of your deposit’s value back in the form of mutual fund shares. This is the law.)

For indexed exposure to EM, there’s $VWO and $IEMG as well as $VEMAX for mutual funds. These are the lowest cost options, but are market-cap weighted only, and do not feature any factor tilting. ex-US markets tend to be more value-oriented, as financials and energy take up a much larger market share.

How I’m positioned today (a bit simplified):

(March 2022 Update: Due to Russia’s threats of invasion, I slowly moved funds out of EM entirely, as well as a portion of my international holdings. I’ve re-invested these in Latin America, commodities, energy, and miners. Funds added: $ILF, $LATAF, $VDE, $XLE, $SSENX, $VGPMX. I plan to trade away most or all of my energy/commodity exposure to reinvest overseas, and am not adding new money to energy/commodities/miners.)

65% US

35% US: $VOO S&P 500 / $VFIAX / $AVLV

10% US: $VTI Total Market / $VTSAX / $AVUS

5% US: $VTFAX Vanguard FTSE Social Index (slight growth-tilt, no energy)

14% US: $COWZ, US Large Cap Cash Cows (value)

1% US: $VUG (Growth balancing)

29% DM

16% DM: $VEA / $VTMGX / $SCHI (as $SWISX, mutual fund) / $FNDF (or $SFNNX, the mutual fund)

8% DM: $VWICX, Vanguard Core International Stock / $DODFX Dodge & Cox International Stock (both are value-tilted)

5% $EFV / $VTRIX for EAFE/international (value)

6% EM

4% EM: $DFAE / $DFCEX (DFA Emerging Markets) / $VMMSX

2% EM: $AVEM (Avantis EM)

This is a pretty simple portfolio, but it can be made much simpler:

65% $VTI

29% $VEA

6% $VWO / $IEMG

If you have access to Vanguard mutual funds, you’ll have a plethora of options to tailor your portfolio. Why do I have $VFTAX when it has no energy? Because $COWZ and $EFV and $VTRIX have loads of energy names in them. I also think that oil companies may underperform the market, and will adjust accordingly. They’ve just had two horrible days, despite crude prices going up 2%, many were down -2%.

That said, I prefer the energy names in $VWICX, $VTRIX, $COWZ and $EFV to the high-priced ones found in $VOO. I also prefer the mid and small-cap energy names in $VTI to the large-cap names. (Update: I wrote an analysis on $VWICX and some comparable funds in a separate issue.)

In short, I’m looking at a mostly neutral US portfolio with a fossil-fuel free allocation that’s growth-tilted, but offset by ex-US value and SMidcap value and energy names.

Charting some of the relevant funds I’m using in 2022:

(note: $VWICX and $DODFX have not updated today, we can extrapolate to ~$10,300 YTD)

Again, the most simple allocation would be to own all the stocks in the world with $VT / $VTWAX. This includes SMidcaps, which may or may not be desirable.

100% $VT / $VTWAX

or, you can mix and match to create your own blend. Most advisors recommend at least 20% in international stocks, which is my minimum. If US markets are on a warpath, like in 2020/2021, I’ll make an exception. Not in 2022.

60% $VTI

40% $VXUS

To exclude small caps, I’d use:

60% $VOO / $VFIAX (S&P 500) or $VFTAX (Social Index which excludes energy and ESG controversies. I use both.)

40% $VEU / $VFWAX (Vanguard DM index funds)

To exclude EM:

60% $VOO / $VFIAX

40% $VEA / $VTMGX

In the future, we’ll explore some of Vanguard’s less-obvious choices, as they have many funds that beat their respective benchmarks, or provide a more desirable factor exposure than simply holding the indices.

I highly recommend using Morningstar and their 15-day free trial to read up on (and save PDF copies of) any funds that interest you. While Vanguard is the best out there, Schwab has some interesting “Fundamental” index funds that I like to use as an alternative to a value fund.

P.S. The top holdings for $VWICX: https://investor.vanguard.com/mutual-funds/profile/portfolio/VWICX/portfolio-holdings

Honestly, this is my kind of value-tilted portfolio. It even holds the $VEA ETF for liquidity, rather than holding onto a bunch of cash like many other fund companies.

Incredibly well-balanced.

P.P.S. If you’d like another interesting fund, check out $VQNPX for a US-based fund that attempts to beat the S&P 500, or $VDEQX for a growthier fund that tries to beat the Total Market Index and contains many actively managed funds. Note, active management costs far more than indexing, but remains affordable with Vanguard funds. I wouldn’t use them for a lifetime, but for a year or two, they can be great.

P.P.P.S. One of my favorite funds from the 2010’s was $VWUAX, which had a horrendous year in 2021 after returning 50%+ in 2020. $VWILX is the international counterparty. Each did tremendously well in 2020, and both have Baillie Gifford as co-managers. BG is an excellent management team, if you ask me. However, they are VERY aggressive about owning growth and these funds should be approach with the utmost of caution. Their growth sleeves are often more volatile than $QQQ. As such, they can (and do) return less (or more) than the Nasdaq, and pose difficulties for portfolio balancing. ($VWUAX is in $VDEQX!) $VIGAX is the only “safe” “growth” index option with Vanguard (also known as $VUG). $VVIAX / $VTV is the value counterpart. Together, they make $VLCAX, based on the CRSP Large company index.

P.P.P.P.S. For a fun trick, you can combine $VWNDX (active large value) with $VIGAX (indexed large growth) and beat the S&P 500 by a few %. At least in 2022, you can. $VWNDX is beating $VVIAX by several percentage points. That all said, it’s best to stick to indexing unless you’re willing to PAY for ADDITIONAL RISK. Not the best deal, I’ll admit. But it’s fun!

Enjoy the green today. Let’s hope Russia doesn’t do a sneak-attack or something…

—Avery

Edit: Fixed “$VWICZ”. The correct ticker is $VWICZ”

Excellent overview. Thanks for your thought stream..