Chartopia: The Wages of War

Chartopia: The Wages of War

GDP, CPI, Inflation, and forecast changes. Updated March 8th.

Note: I’ve made significant additions and revisions to this issue as of 6PM ET, March 8th.

- TryEngineering.org Powered by IEEE")

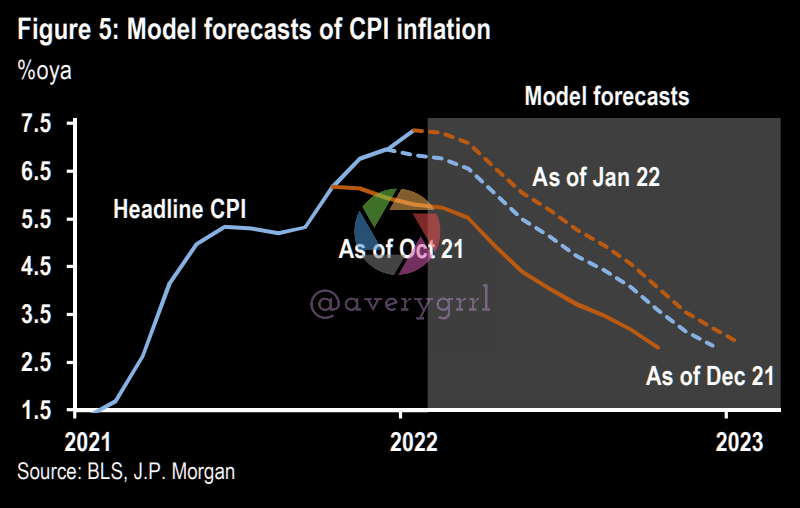

Consumer Prices 1Q-2Q22

Global CPI can be expected to rise at a sharp 6% (annualized) rate for a second consecutive quarter in 1Q22, an outcome that would far exceed the largest two-quarter gain over the last 25 years.

The recent surge in commodity prices has added pressure, and rising costs extend beyond oil to include a shocking amount of upward pressure on metals and agricultural commodities. This may be reason to anticipate inflation rates continuing at or near their current clip.

War Isn’t Always Good For Markets

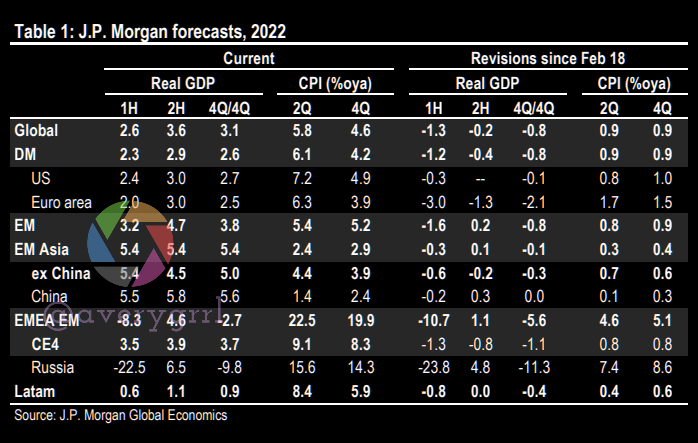

Following a week of Russia’s war on Ukraine intensifying, increasing sanctions, and a wide range of risks to commodities warrants further investigation, and revisions to global macroeconomic outlooks. The war in Russia can be expected to cut Russian GDP by 12.5% (peak-to-trough), which would be on-par with the 1998 debt default.

Expect a cut of 0.8%-pt to growth and 0.9%-pt increase to inflation in 2022.

Risks rise of a material disruption of global energy supply.

Global inflation likely to remain close to 6%ar in 1H22.

Next week: EU guides on energy policy; ECB remains cautious.

Russian energy supply varies by region. Sanctions have been aimed at inflicting significant damage to the Russian economy while maintaining the flow of oil and natural gas exports. To date, this has been accounted for in revisions. However, this week’s sanctions (notably restrictions on Russia’s access to its reserves and global banking services) are more far-reaching, and undermine crucial pillars of Russian stability: the “fortress” FX reserves of the CBR and its current account surplus

War and Commodities In Focus, GDP/CPI Revisions

I posted a situation report thread today on the Russia/Ukraine conflict. If you missed it, feel free to take a peek before continuing. (It’s split into four parts, below.)

Situation report day 12 March 7, 2022 - Russia announced new “humanitarian corridors” to transport Ukrainians trapped under its bombardment to Russia itself and its ally Belarus, a move immediately dismissed by Kyiv as “completely immoral” reuters.com/markets/asia/t… 1/4

Situation report day 12 March 7, 2022 - Russia announced new “humanitarian corridors” to transport Ukrainians trapped under its bombardment to Russia itself and its ally Belarus, a move immediately dismissed by Kyiv as “completely immoral” reuters.com/markets/asia/t… 1/4

Commodity supply lines are no longer secure and risk premia have lifted the entire commodity price complex. Any realized disruption to energy is, however, likely to be limited in duration and effects.

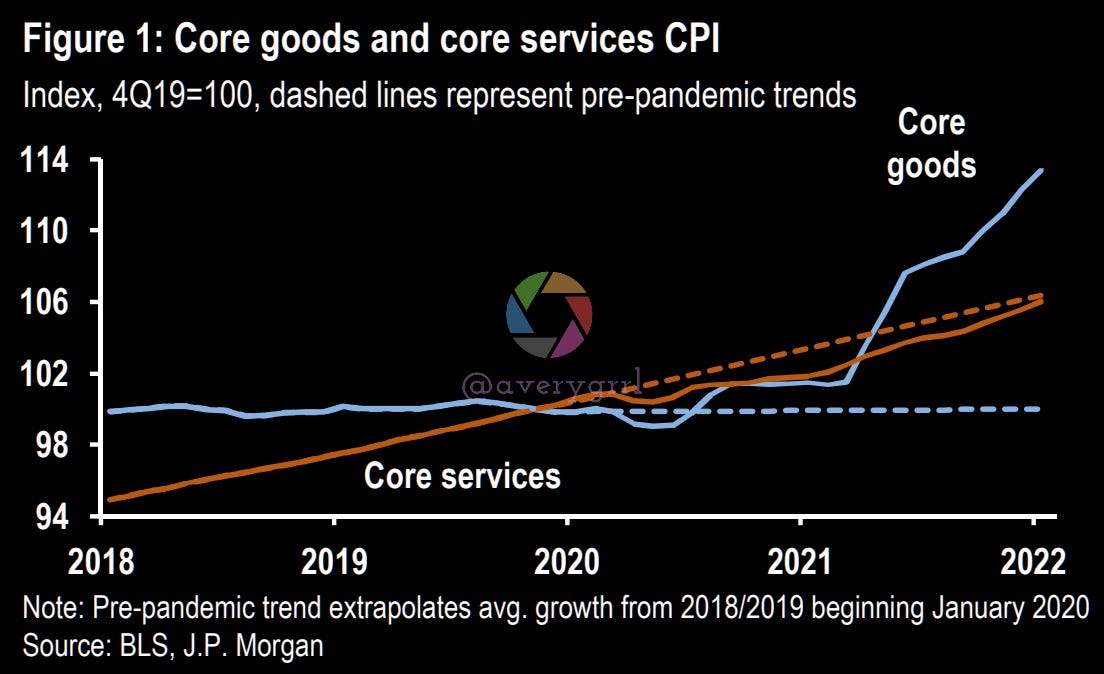

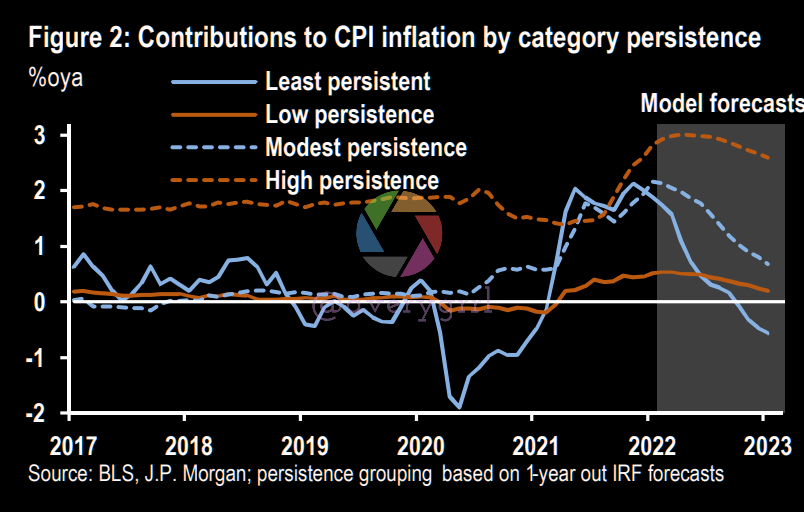

JPM GDP/CPI forecasts including revisions from Feb 16th on. The most persistent categories of inflation contributed 2.8%-pts to 7.5%oya headline CPI inflation in January.

Typical pre-pandemic persistence of such shocks could keep CPI inflation above 3%oya through 2022...

…even before accounting for inflationary pressures from tight labor markets and Russia/Ukraine conflict.

Increase in inflation expectations given more persistent inflation and recent geopolitical developments.

A sustained 6% loss of buying power will be an obstacle.

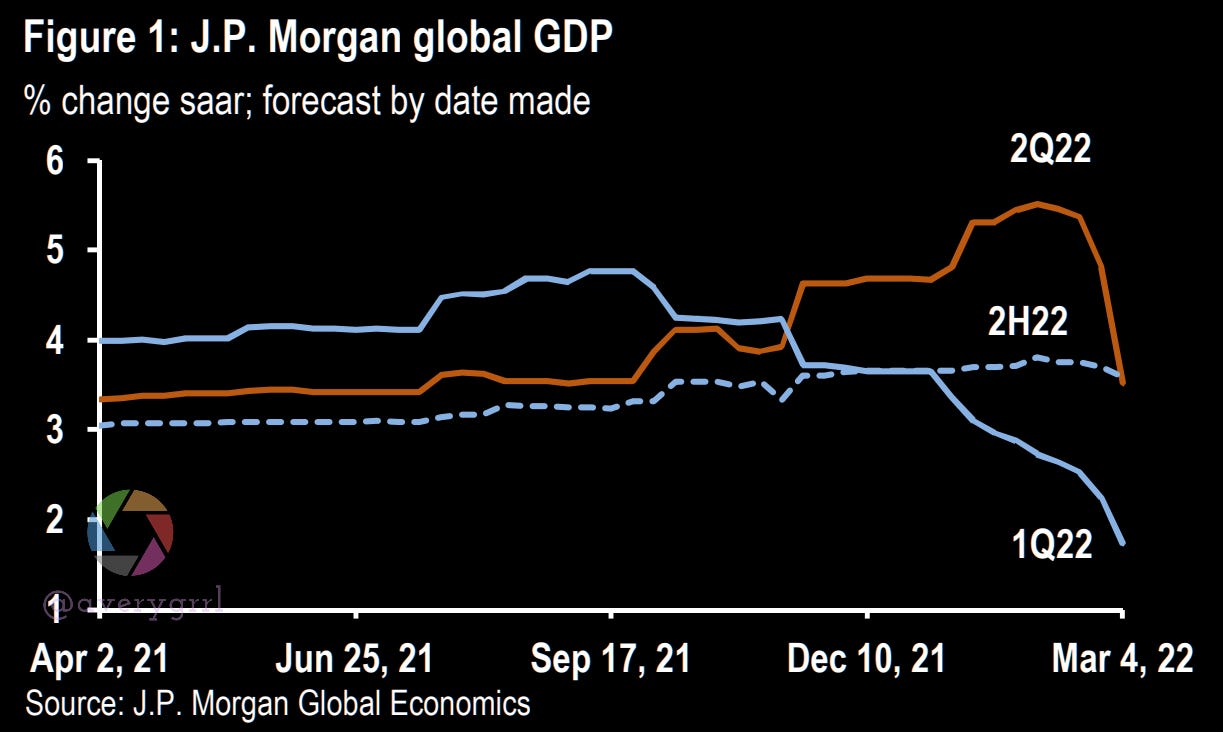

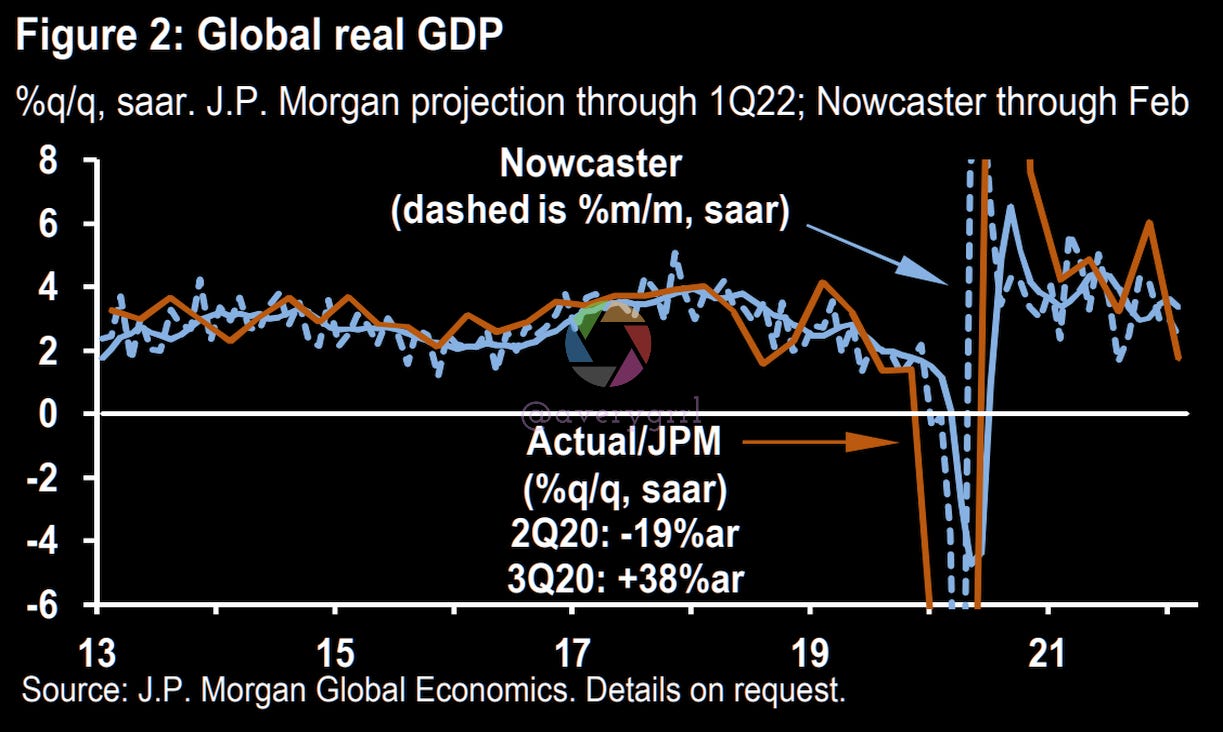

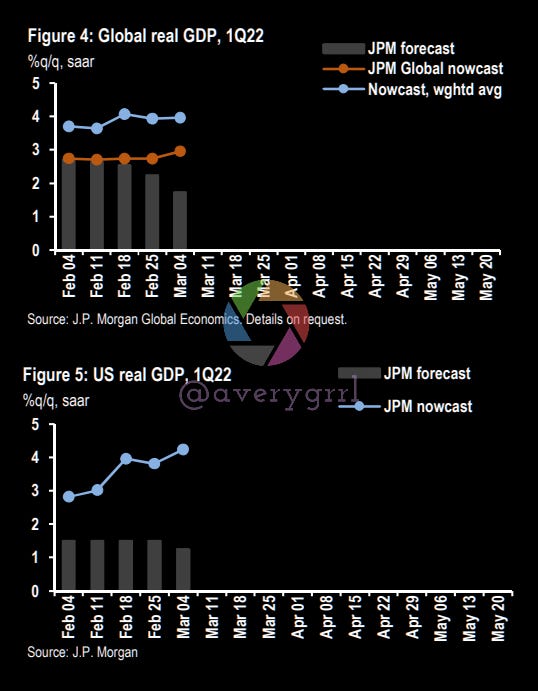

The drag at the global GDP is concentrated in 2Q and in Europe, though the situation is fluid. Prior to the war, the global economy appeared to be accelerating in January and February as evidenced by the February PMIs released earlier this week. In the US, January retail sales and the February labor market report were strong.

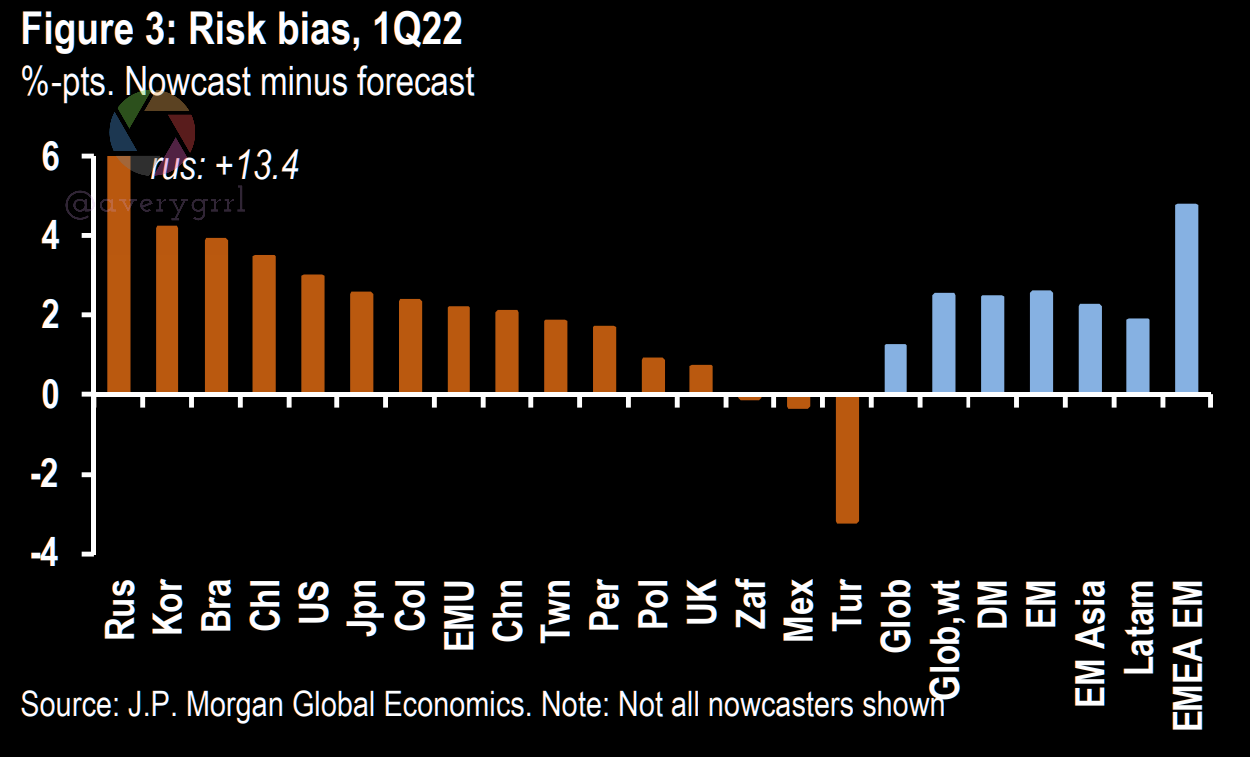

“After a flurry of downward revisions in response to the Russian invasion of Ukraine, the majority of our country-level nowcasters suggest upside risk to growth in 1Q22. Turkey stands out with the nowcaster pointing to weaker current-quarter growth than our forecast.” —JPM

Zooming out, let’s take a quick peek at Euro area and EM GDP forecasts following JPM revisions.

A look at real GDP vs. policy rates.

Commodities, and Russia/Ukraine

Russia and Ukraine are relatively small on the global stage, accounting for roughly 3% of global GDP. Although the sanctions imposed this week constrain Russia’s exports of non-energy products and its access to global financial markets, the linkages between Russia and the rest of the world are small. By contrast, 85% of Russian exports are in commodities, in which it accounts for well over 10% of global oil and natural gas production

While credit spreads have widened recently there is no sign of unusual stress building in funding markets or in EM sovereign spreads outside of Russia.

70% of Russian Oil Struggling to Find Buyers

JPM: “Building on these judgments our forecast revisions to date lower 2022 global GDP by roughly 0.8%”

The risks to this baseline scenario are skewed to the downside with a particular focus on possible disruptions to energy supply. While the US and its allies have not imposed direct penalties on Russian oil and gas, preliminary Russian crude oil loadings for March reveal a sharp drop. Nearly 70% of Russian oil is struggling to find buyers. Behind this drop, a number of oil tanker owners are taking a caution-first approach until the full picture on sanctions is clear. A potentially more significant factor is that international energy consumers are objecting to using Russian barrels.

DM and EM demand curves for oil DM real GDP growth

So, how do we look at GDP growth for DM/EM when it comes to oil pricing and demand shocks?

This is written in terms of GDP growth (as a proxy for oil demand growth) and growth in the price of oil. For expositional purposes, real GDP growth is on the left-hand side of the equation:

DM real GDP growth = 1.4+0.2*(EM real GDP growth - 4.2)-0.015*(Oil price growth)+DM demand shock

EM real GDP growth = 4.2+0.9*(DM real GDP growth - 1.4)-0.010*(Oil price growth)+EM demand shock

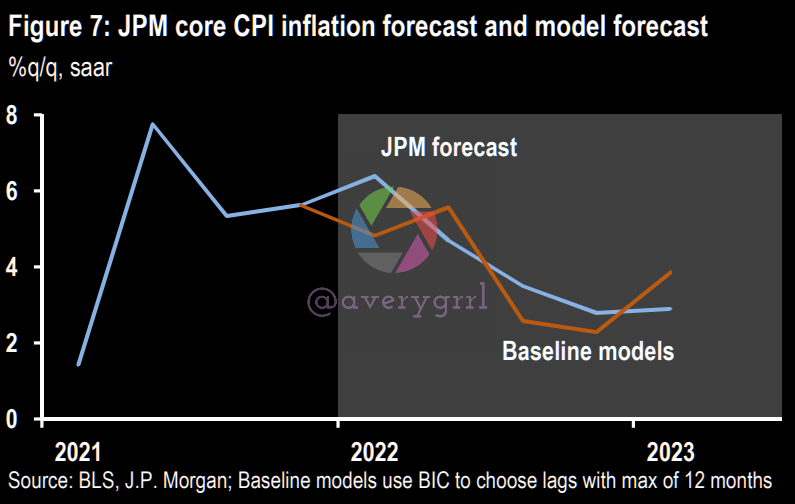

CPI/Inflation Internals

While I’m trying to stick to a quick update, here’s a rundown of CPI and inflation internals/contributors, and some more charts for your perusal.

Contributions to CPI inflation and impulse response of CPI sub-aggregates:

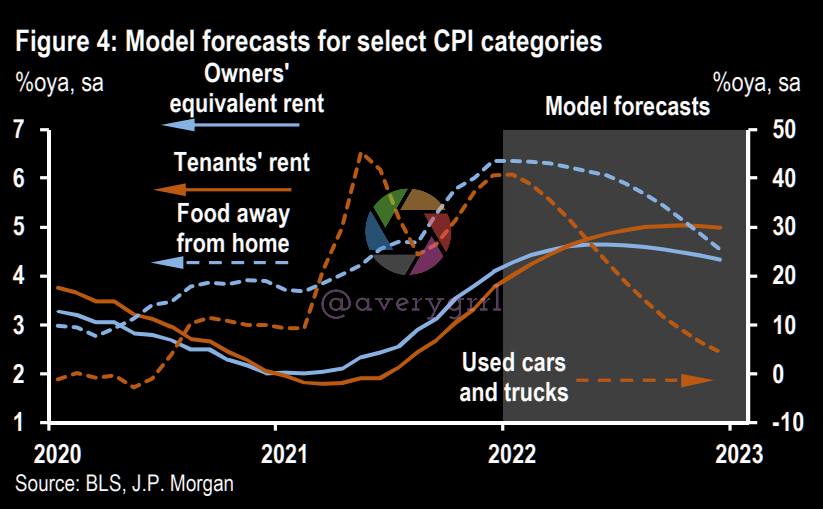

Model forecasts for select CPI categories and inflation:

Some things to consider:

Inflationary risks from rising energy, commodity, and food prices as a consequence of the Russian invasion of Ukraine and the resulting sanctions imposed on Russia by the US and other countries.

Potentially faster sequential inflation throughout 2022 than would be expected by the baseline models.

Potentially even greater inflationary risk in the coming year than expected just one week ago.

On a Q4/Q4 basis, JPM now expects CPI inflation to hit 4.9% in 2022 (revised up from 4.1%) with core CPI inflation to be up 4.3% (revised up from 3.9%).

United States

Powell signaled that the FOMC is still on track to hike 25bp in March and more throughout the year.

Russia-Ukraine conflict adds uncertainty; inflation forecast have been revised upward and GDP forecasts have been trimmed.

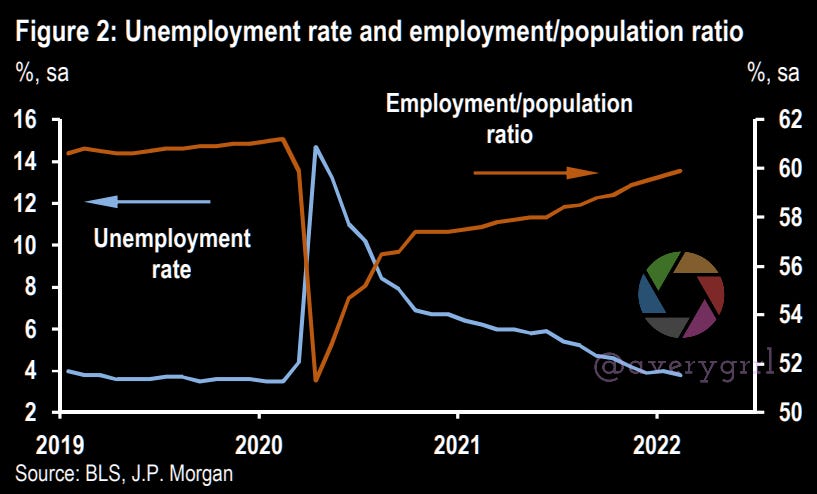

February employment report showed strong job growth (678,000) and decline in the unemployment rate to 3.8%.

Expectations for a 0.9% headline CPI jump in February with core up 0.46%

Fed Chair (pro tempore) Powell testified in front of Congress this week, and suggested the FOMC is on track to hike rates 25bp at the mid-March meeting and to carry on with additional 25bp hikes throughout the remainder of the year.

Nothing is set in stone and recent developments related to Russia’s invasion of Ukraine add uncertainty to the mix, but Powell seemed to suggest that the FOMC’s plan for tightening remains intact, even if the Committee “will proceed carefully along the lines of that plan.”

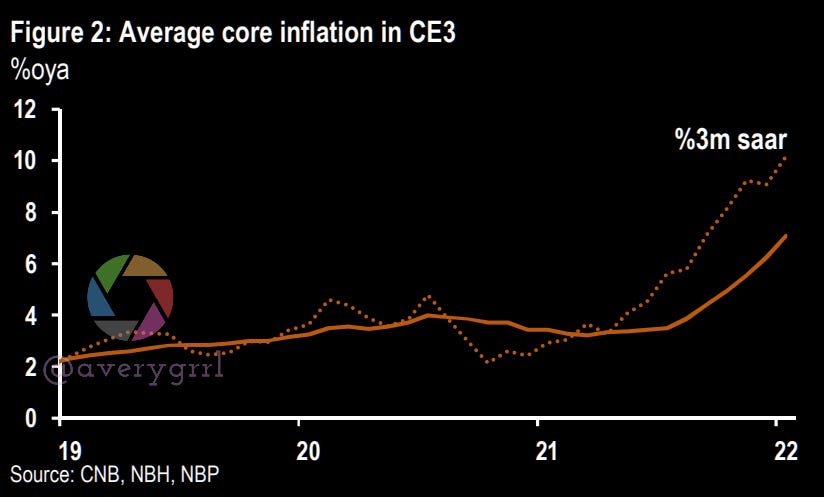

Inflation has been surprising to the upside lately and the strength has been shifting into categories that tend to have more persistent price changes.

While some of the jump in prices over the past year likely will be transitory, a good portion of it could stick around, particularly with the labor market expected to continue tightening and issues with supply chains persisting, at least to some degree.

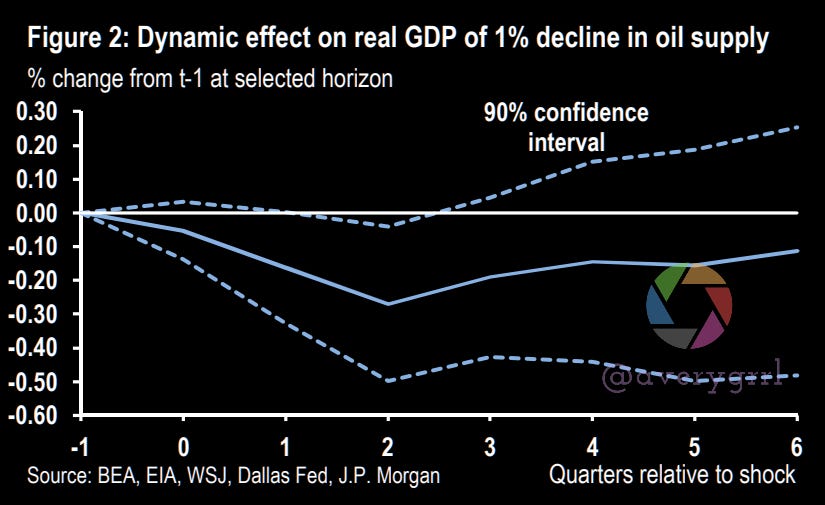

Dynamic effects on oil prices in the event of a 1% decline:

Dynamic effect on real GDP:

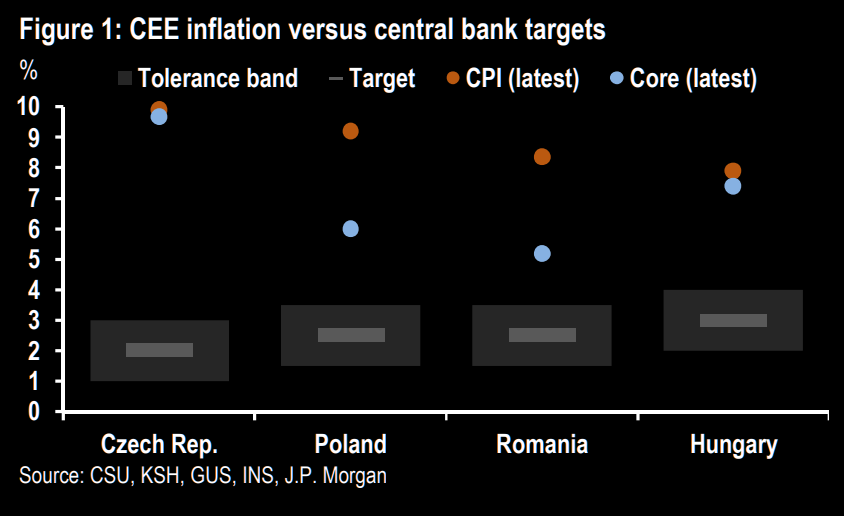

Central and Eastern Europe

A quick look at CEE nations. Due to its proximity to Russia, CEE should be watched closely as effects from an oil/supply shock can be expected to have a more pronounced impact in Eastern Europe.

Things are looking a little dicey in Eastern Europe. Household 12-month look-ahead inflation for Czechoslovakia, Hungary, and Poland are all rising:

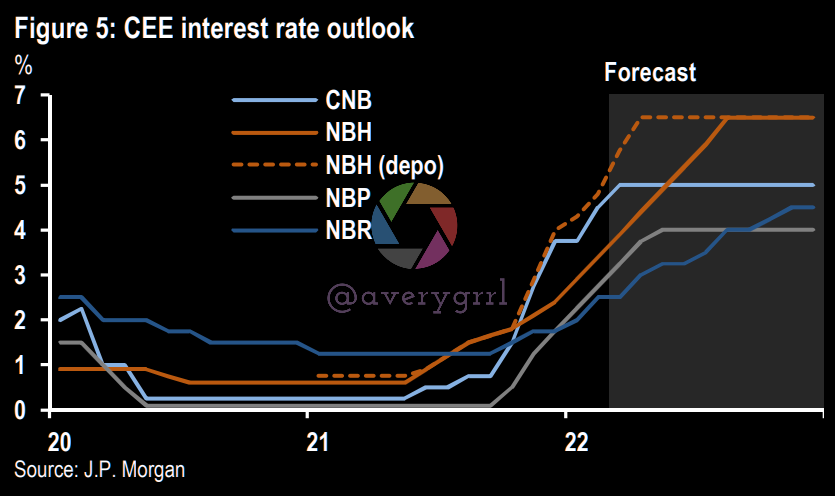

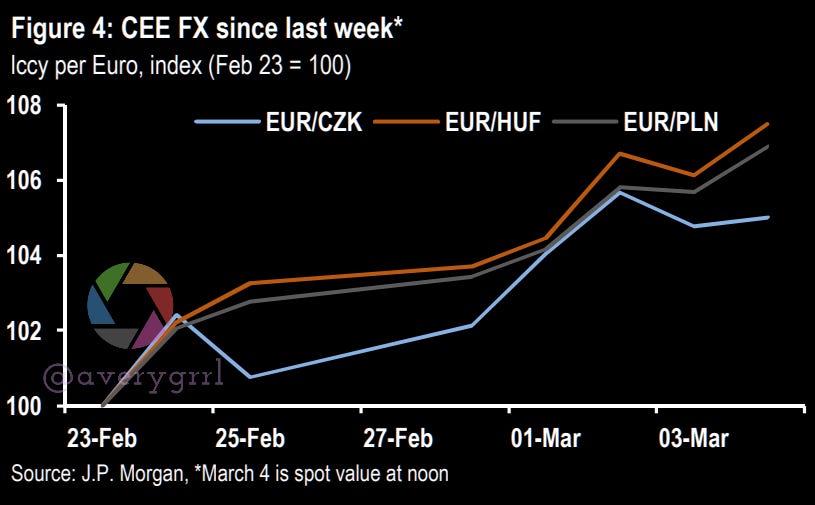

The spike in uncertainty plays out differently in the CEE than in developed market “safe havens”. Regional bond yields have been on the rise, and free-floating currencies are selling off quite quickly. As such, CEE interest rates should steepen more quickly.

JPM is forecasting a liftoff to between 4 and 6.5%:

With many moving parts and situations constantly changing, many predictions, revisions, and forecasts will themselves be volatile. Outlooks should (and will) be like subject to changes as situations develop, and uncertainty wanes. Investors are currently paying extremely high premiums for exit liquidity, as fragile portfolios begin to fall apart, weaker hands fold, and headlines focus more on short-term effects.

Historically, long-term possibilities are given less attention as news coverage focuses on attention-grabbing headlines. This has, at least in my experience, results in oversold fundamentals. At the very least, technical indicators quickly identify oversold positions. Amidst such chaos, it may be prudent to be on the lookout for M&A activity, as well as fundamental value. This comes at the cost of potential policy error, as well as conditions becoming more oversold.

The chances of a market rebound become more likely as equity valuations decrease and futures returns rise. Any breakthroughs in peace talks, supply chain issues, dovvish Fed statements, or other surprises create a scenario in which upside risks can (and will) become greater than downside risks. The market is primarily engaged in discounting downside risks, but has done a poor job of discounting similar upside risks.

(Personally, I expect the Fed to hike only ~4 times in 2022, rather than the 6-7 as we’ve seen previously from markets and Fed dot plots. Rates by 2024 are expected to rise to 2.5%, and as long as inflation remains persistent, we should expect rate increases from the Fed. However, this is a good example of the potential for upside risks to outweigh downside risks. The Fed is more likely to raise rates by 25bps than 75bps in March, for example. Going forward, this becomes more uncertain. Remember, STIR traders are notoriously poor at predicting rates liftoff, with something in the realm of 50 failed predictions for each correct prediction.)

Looking for More Overseas Data

Euro area inflation will be a big concern going forward, and the US may be a safe haven. There also me be parts of Asia and Latin America that fare better than Europe (and Russia) in the face of supply chain disruptions, a tightening labor market, and cost pressures.

Markets have currently caught a bid, as they should. Despite inflation scares, equity remains the only proven way to outpace inflation.

Something that’s important to remember is that inflated prices eventually show up as revenue on corporate balance sheets. For example, prices may be up at the pump, but energy companies will be booking higher profits for as long as this keeps up. I’ve maintained an allocation to commodities, energy issues, natural resource providers, as well as some exposure to miners and field services for both industrial and precious metals, as well as oil.

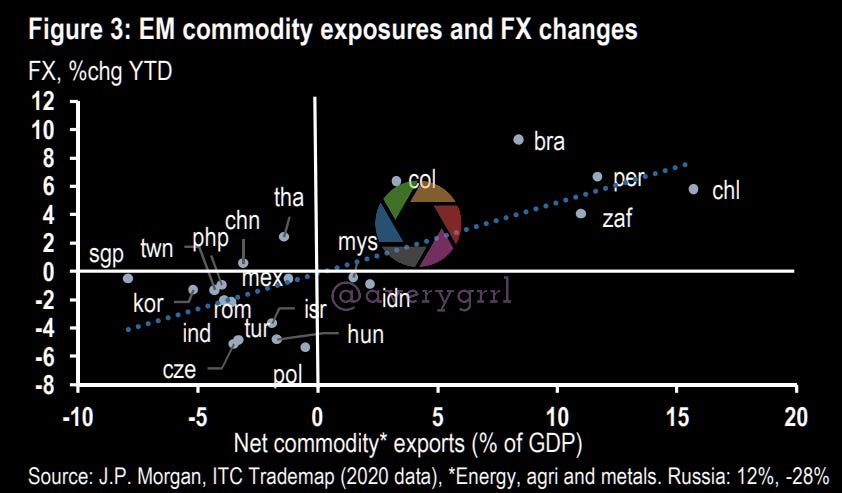

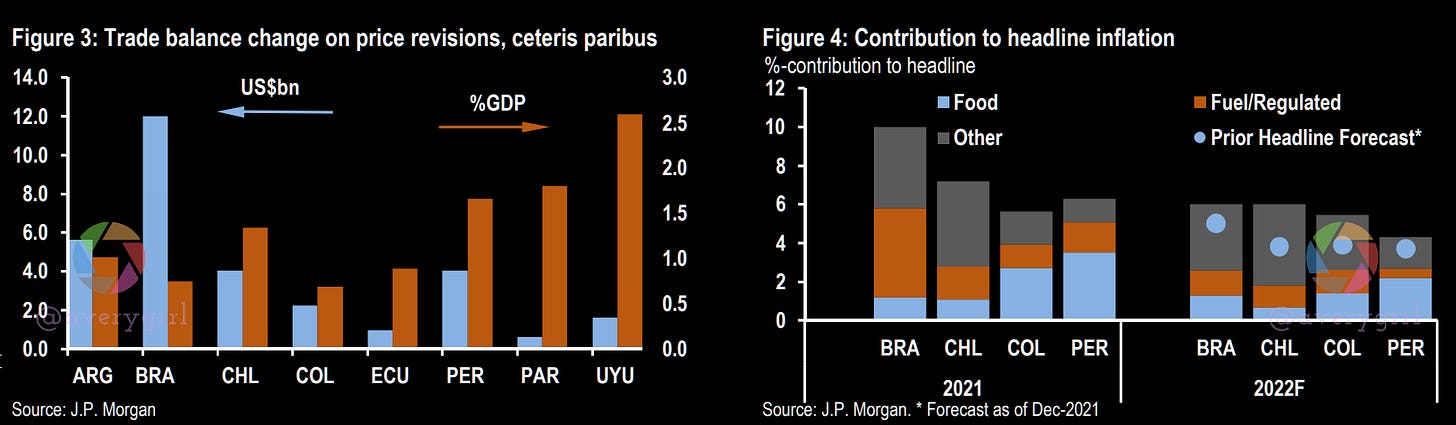

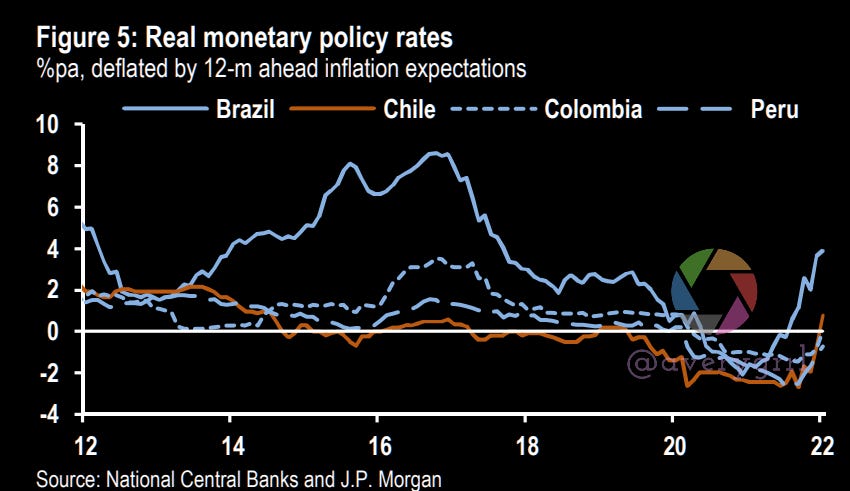

For Latin America, Brazil/Chile/Colombia/Peru are worth a look. Real monetary policy rate expectations are rising (% per annum, deflated by 12-month inflation expectations).

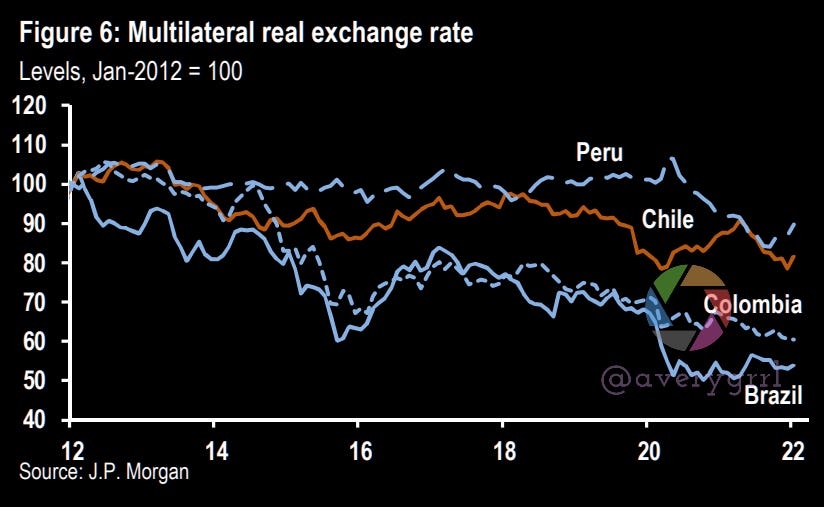

Exchange rates are somewhat mixed, but have fit into a decisively downward trend. This has given a nice boost to South American equities in USD terms. Latin America has been one of the best-performing regions in 2022.

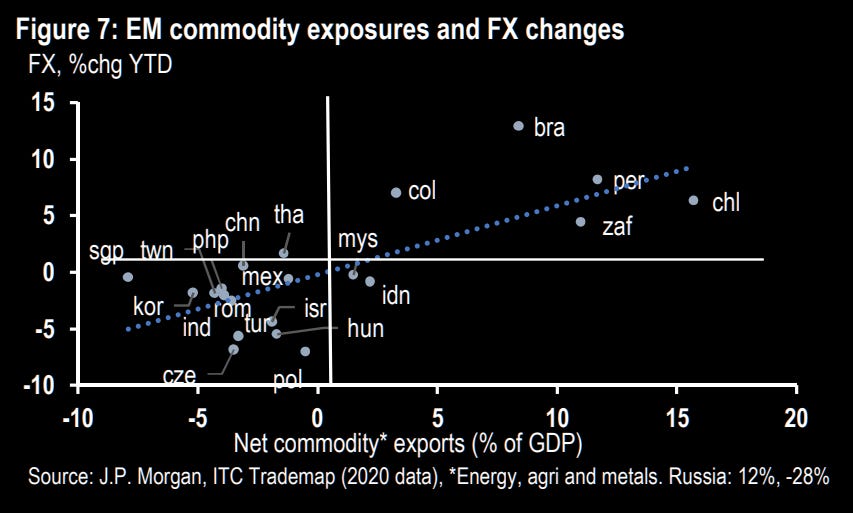

The complete FX matrix for South America is difficult to pick unpack, but it’s useful to visualize where each nation sits on the spectrum of commodity exporters (and their respective exposures to energy, agricultural products, and metals in particular.)

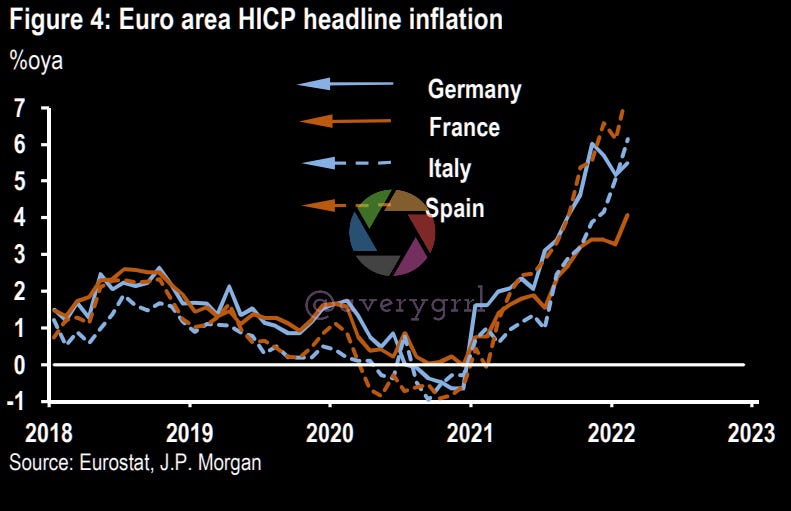

Europe

The cumulative drag on Euro area GDP due to fallout from the Russian invasion of Ukraine is now 2%-pts.

Inflation rose significantly in February (headline 5.8%oya, core 2.7%oya).

Peak inflation is expected to pass in April at 6.4%oya, with the full-year average expected to come in at 5.3%.

ECB to replace hawkish pivot with two-way optionality.

The primary channel through which war in Ukraine can impact the Euro area economy is through the price and availability of energy.

The sanctions on Russia announced so far seek to maintain the flow of Russian oil and natural gas exports while making other Russian economic activity more difficult. It is not necessary for the Russian supply of oil or gas to Europe to stop completely to have an impact that extends beyond the increase in its price.

According to commodities analysts, a sustained 15% reduction in gas supply from Russia to Europe would exceed the region’s ability to meet energy demand from other sources, forcing rationing of supply to industrial users. Beyond the risk of tougher sanctions or retaliation, there is also the potential for supply disruption on the basis of damage to infrastructure, particularly pipelines that run through Ukraine.

March 8th Update: Commodities Going Haywire

This morning, we had some of the wildest action on commodities I’ve seen in a long time. Nickel was up +250% on the LME (and halted) in a short squeeze for the history books. This is, truly, unprecedented, and I’m surprised it’s not a bigger topic.

I knew copper was important, but I didn’t think nickel is THIS important. Tsingshan, one of the top producers of nickel was under pressure to meet margin calls. Traders caught on the short side rushed to the exits in what can only be described as unprecedented short squeeze. I think this is due to Russia having the largest nickel mining firm on the planet.

“Chinese nickel titan Tsingshan Holding Group faces billions of dollars in trading losses, people familiar with the company said, after Russia’s war in Ukraine set off an unprecedented rise in the price of a key metal used in stainless steel and electric-vehicle batteries.

The paper loss stood at $8 billion on Monday, before violent moves in nickel prices led the London Metal Exchange to suspend trading in the metal on Tuesday, one of the people said. Late Tuesday, the exchange said it anticipates trading won’t resume before Friday.”—WSJ

So, what’s behind nickel? That’d be mining companies, like Glencore. The largest Nickel producer? That would be Nornickel. A russian firm that produced 236 kilotons a year as of 2020.

We’ve witnessed a historic rise in energy prices, with oil futures up 62% as of 8AM this morning, gasoline and fuel up between 60 and 110%, natural gas up as much as 181%, and Rotterdam coal futures up 209%.

100-day AVAT, or “Average Volume At Trade” was +4,626% for NYMEX Dubai Crude, and +1,900% for NYMEX Japan/Korea Marked LNG. (If you’re new to this, LNG is liquefied natural gas. Crude is the oil they pump out of the ground, and fuel/gas are the “refined products”.

See the table below for the whole picture, as of 8AM ET:

As WTI crude rises, so do the fortunes of US oil majors. Rig counts have been stubbornly rising at a rate of approximately 24 per month after plateauing in October. I’ve noticed prices usually tend to moderate shortly after these plateaus.

While we may need to wait for updated data, we’re at 650 rigs according to data from March 4th PVMI (which I’m 99% sure means Production Vendor Managed Inventory. Doesn’t matter. I just count the rigs.) Does this mean we can expect oil to fall?

Not so fast. We’re trading at $124.77 now.

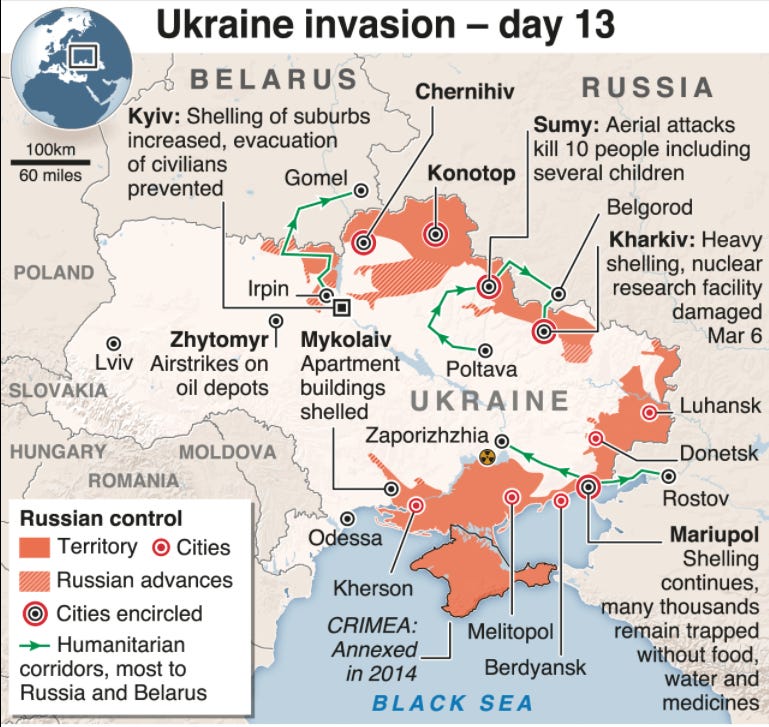

Russia’s War in Ukraine

(If you’d like to skip the war stuff, just scroll down to the next divider. There’s one section about Russian sanctions, but I do not discuss the war there.)

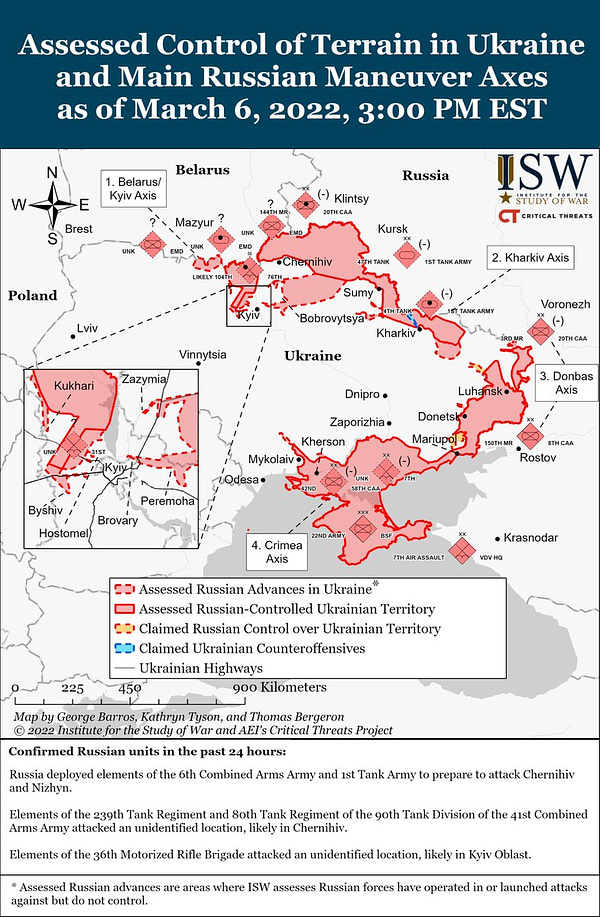

I put together a thread on Twitter, which I’ll link below, but here is a visual guide to the current situation on the ground in Ukraine. This map was updated today, March 8th.

March 8, 2022 - Russia's offensive in Ukraine continued but at a significantly slower pace as Moscow warned the West that bans on its energy exports would lead to a “catastrophic” rise in the oil price to $300 a barrel.

Several Ukrainian cities remain under siege conditions, with the southern city of Mariupol hardest hit. Encircled by Russian forces for almost a week, the city is facing shortages of water, electricity, food and medicines, according to Ukrainian and UN aid officials.

Despite deteriorating conditions on the ground, Russia has failed for three days to enforce a promised ceasefire or provide viable evacuation corridors for civilians from frontline cities, while blaming Ukraine for violations.

Ukraine's military intelligence said on Tuesday that Ukrainian forces killed Major General Vitaly Gerasimov near the besieged city of Kharkiv, the second Russian senior commander to die in the invasion.

Russia's invasion, the biggest attack on a European state since World War Two, has created 1.7 million refugees, a raft of sanctions on Moscow, and fears of wider conflict as the West pours military aid into Ukraine.

The ISW (Institute for The Study of War) has put together comprehensive analysis of the situation. For those who are interested in a highly detailed report, I recommend checking their website.

I’ve included the full-resolution (2550x3600) map from ISW here, updated at 3pm on March 7th:

You can read the whole thread here:

Russia’s Slow Military Advance

Russia has the firepower to reduce Ukraine to rubble, but its military strategy is backfiring. The loss of top-ranking officers, plus fuel, food and ammunition shortages, exposes strategic failings.

Russian President Vladimir Putin’s invasion of Ukraine does not appear to be going as the Kremlin wished. After nearly two weeks of brutal fighting, Russian forces struggle to capture Ukraine’s major population centres -- the capital Kyiv and Kharkiv in the east.

Putin drastically underestimated Ukraine’s cohesion and will to resist. Russia’s cyberwarfare machine has failed to shut down the internet enabling Ukraine’s President Volodymyr Zelensky to use social media to keep morale high.

In addition, Russia now faces a range of sanctions never inflicted on a superpower before, notably the freezing of $350 billion of assets of the Central Bank of Russia held in offshore accounts.

Putin also underestimated opposition to the war within Russia itself. His fight against fellow Slavs to “denazify” a country with a democratically elected Jewish president is likely the most unpopular decision he has ever made.

Low Morale: Young conscripts with minimal training did not know they were going to war.

Tactics: A Russian convoy stalled outside Kyiv is approximately 400km from its main supply base inside Russia. Logistics require it to be no more than 150km from supply base.

Mud Season: Rain and melting snow have made cross-country traversal difficult for trucks and wheeled armored fighting vehicles. Using roads exposes vehicles to attacks.

Command and Control: After destroying cell phone towers, Russia’s encrypted communications no longer function inside Ukraine.

Decisions: Officer corps cannot make on-the-spot decisions and must ask top military eladers for permission in operational matters.

Cyber: The Russia’s cyberwarfare apparatus failed to disable the internet, and Russian accounts have found themselves banned from social media platforms. Ukraine’s President Volodymyr Zelensky is using social media to keep morale high.

Putin’s Ukraine expedition has not gone as Moscow initially wished, but experts think Russia is not doing as badly as the Western media reports.

As the Ukraine war entered its second week on March 4, Russia channelled 95 percent of its amassed firepower into Ukraine from different directions in a bid to force its rivals into submission. But Ukrainians put up a stiff resistance, preventing the world’s second-biggest army from declaring a quick win.

After nearly two weeks of brutal fighting, Russian forces are struggling to capture Ukraine’s major population centres, like the capital Kiev and Kharkiv in the east. Russia's President Vladimir Putin expected Kiev to capitulate to Moscow just like the Crimean Peninsula, quick to surrender to the Russian forces in 2014.

Yet, according to some experts, Russia's slow and expensive advance in Ukraine should not be misconstrued as a total failure of Moscow’s military goals.

Russian Sanctions

I’ve been tracking the sanctions on Russia, with many new developments following the invasion on the 21st. Prior to February 22nd, Russia had 2,754 sanctions. Since then, we’ve seen an additional 2,827 sanctions (73 more than before the 22nd, nearly doubling the number of sanctions) placed on Russia.

I believe its important to watch these sanctions, as they can have sweeping effects on markets.

Thanks to Datawrapper and Castellum AI for charting and data.

I only intended to write a brief note, and have gone on for a bit. I’ll be back with some more insights on the situation as it develops.

March 8th: The post has been updated, and it’s not “brief” at all. Brevity and I haven’t been on speaking terms since Gorbachev was in power. Sorry.

Stay The Course

With all that behind us, I cannot stress this enough: while current geopolitical forces will have an impact on returns for short-term investors, any drawdowns will result in increased forward returns for equities. As such, it is important to view drawdowns as a discount window during which the market can be bought at a lower price, amplifying future returns.

We have already witnessed panicked selling from every class of investor, from institutions and hedge funds, to high net worth individuals, to retail. A focus on the long-term, as well as principles of value investing, should provide enough optimism and confidence moving forward.

Try not to be worried by ongoing events when it comes to your investments. While I’ve felt horrible about what the people of Ukraine are coping with currently, all I can do is donate to them and pray for them. With that said, I’d prefer the market to go down as much as possible, within reason. Scares like this are, on an evidentiary basis, a net positive for forward returns and the accumulation of future wealth.

I absolutely, and with 100% certainty believe the markets will be higher in 10, 20, or 30 years. Higher and higher. As such, drawdowns will always be buying opportunities. I do not mean “buying dips” (which is an over-used term.) Rather, sticking to a solid plan, ignoring the daily movements of the market, and simply focusing on accumulating shares is the best path forward. This mean buying the dips, the rips, and everything in-between. The market mostly goes up, and you want as much invested as possible.

Until you’re able to see the future, consider automating deposits for when you have new income to allocate. A good rule of thumb is to allocate 15% or more of all new money to investments. In addition to 401k contributions, I automatically buy mutual fund shares every payday. (For pre-tax contributions, it may be best to have a higher total allocation, as taxes will need to be paid eventually. As always, speak to a fee-only financial advisor for advice specific to your needs.)

If you have trouble looking at your balances too often, remember: your current balance is NOT a scorecard and has little to do with the future worth of your investments. I recommend focusing instead on your share count or expected dividend payouts. There are better ways to look at a portfolio than your net liquidation value, something we should all have learned in elementary school.

In fact, looking at a portfolios current value is, frankly, pretty worthless. The more one looks at the portfolio, the lower returns they get. An odd but real phenomenon. Remember to relax. A properly balanced portfolio doesn’t need babysitting. Like a delicate flower, it needs room, water, and food (frequent deposits) to blossom and grow.

A true measure of worth is how well one can save and invest, stay the course, and maintain enough strength to show discipline, patience, and foresight through thick and thin.

This is particularly important during any type of crisis, whether it’s political, financial, or otherwise. We will always have bear markets, corrections, and crashes. Only by staying the course are we ensured our fair share of market returns and the ability to meet our financial goals, despite inflation.

Let’s hope tomorrow is a nice green day, as I know a little morale boost is needed. Don’t fret, have faith in the future, stay optimistic, stay invested, keep calm, and enjoy the life you have while you have it. You only get one, and it’s your most important asset of all.

Treat yourself and your loved ones well. Don’t ever let market perturbations come between you and the life you want to lead. We made it through the Cuban Missile Crisis, the oil/stagflation crisis of the 1970’s, the panic of 1907, the tremendous 1929 crash, a global financial crisis, presidential assassinations, and far too many wars for me to count.

What feels new and urgent will, like all other emergent events, become a blip in memory. If the market survived the 1970’s, the 2020’s should be a cakewalk. We have the most accommodative political body for corporate growth in the modern world. There’s a reason the US market is over 55% of the total world market cap. The US is the best place to operate a large international business, and if the US is good at anything, it’s that.

Everything will be fine in due course. I promise you that.

Have a great night!

—Avery

P.S. For those asking why I do not charge money, I’m not comfortable doing so right now. However, I may in the future, should I decide to put more effort and time into these posts. If you would like to leave a tip, there’s a Cash app link in my profile.