Investing With M1 Finance

An adventure into the realm of dynamic rebalancing

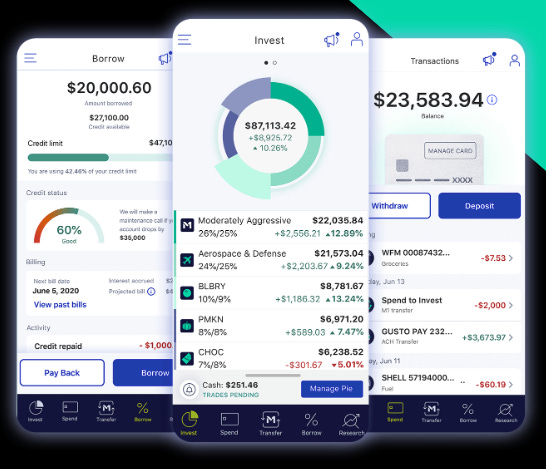

Taking A Look: M1 Finance

I recently made an M1 finance account, and have been impressed. Here’s a $10 bonus link to sign up. It’s a fascinating platform, and supports many different types of accounts. I just opened a joint account to get someone else involved with investing (and avoid any professional data fees), and I’ve been impressed enough that I thought it was worth sharing.

I think it strikes a nice balance between a self-managed portfolio and an automated Vanguard/Fidelity portfolio. The sleek and intuitive interface is fun and rewarding to use. Almost as if Vanguard somehow paired up with Robinhood. (There’s no confetti or anything, but the interface is very modern and smooth).

THIS PORTFOLIO HAS BEEN UPDATED. CLICK HERE FOR THE UPDATED VERSION OF MY PORTFOLIO.

I think M1 is a great place to put a small part of your portfolio. I’ll always recommend Vanguard (or Fidelity, at least), and automated investing, but M1 offers a new type of automated investing that’s a lot of fun. Who doesn’t want investing to be fun? Unfortunately, the best investors are incredibly boring.

I think M1 strikes a nice balance between fun and prudent.

What Is M1 Finance?

According to Wikipedia, “M1 Finance (commonly abbreviated as M1) is an American financial services company. Founded in 2015, the company offers a robo-advisory investment platform with brokerage accounts, digital checking accounts, and lines of credit. M1 offers an electronic trading platform for the trade of financial assets including common stocks, preferred stocks, fractional-share ownership, and exchange-traded funds. It provides margin lending, automatic rebalancing services, automatic dividend reinvestment services, and cash management services including debit cards. The company receives payment for order flow. The platform has over $6 billion in assets under management. M1's headquarters is located in Chicago, Illinois. As of November 2021, the company had over 500,000 members.”

M1 lets you create your own portfolio, much like a robo-advisor would. I’m not a fan of robo-advisors. They cost too much and the options are far too limited. Some allow a bit of customization. I think Wealthfront lets you add custom pieces to a portfolio. However, most automated investing platforms like robo-advisors charge an enormous fee, usually 0.35% or more.

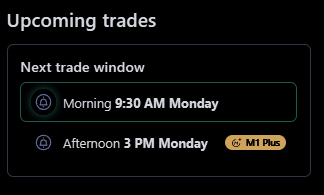

M1 has competitive margin rates, a 1% yielding checking account, a 1% cashback debit card, and a credit card. Deposits are available immediately. Investing is done in windows, with buy and sell orders being handled in blocks at the open (and again at 3pm for M1 Plus members. You get one free year of M1 plus which has a few other nice perks.)

M1 tries to automate as much as possible. You can set your allocations however you like, and it will invest in your portfolio, attempting to maintain the allocations you selected. Dynamic rebalancing means that new money is invested first in under-performing issues, attempting to bring the portfolio in-line with your chosen allocations. I have my own thoughts on this.

You can set a maximum cash balance before M1 will invest. This is set at $25 by default, but if you set it higher, it may result in lower trading costs. You can also choose to rebalance at any time.

Dynamic Rebalancing

I’ve always preferred using rebalancing bands, which means only rebalancing my portfolio when a holding has deviated too far from it’s intended allocation. To me, allocations are about how new money is invested. While many people believe a portfolio should try to stick to its allocations, I believe this is wrong-headed.

Essentially, M1 uses a 0% rebalancing band with a $1 minimum deviation. As such, it will invest more heavily in under-performing issues. This has its ups and downs. In short, rebalancing reduces risk, but many studies show that frequent rebalancing can (and does) mute returns.

I believe this logic comes from index funds, which by nature, necessarily remain “perfectly” weighted to their constituent index. M1 treats your allocations as if it were an index. While this isn’t a huge deal, it’s something I’d like to see changed. I think the platform is a fun way to invest, and could encourage good behavior.

An important piece of information to mention is that M1 conducts its trades from 9:30am-10am or so. For M1 Plus accounts (you get 1 year free of Plus), there’s a second trading window at 3PM. If your account is under 25k, you can only use one window per day, to avoid the possibility of day-trade violations. If you have a regular M1 account, you can only use the morning window.

This can be a turn-off, but it really does encourage better behavior. There’s absolutely no justification for people to be going in and out of the market or turning their portfolio over unnecessarily. It’s best to stay the course, and I think M1 does a good job of making that an interesting and fun process.

You can, at any time, decide to buy or sell anything in your portfolio, but this is done manually. Alternately, you can adjust the allocations and the portfolio will dollar-cost-average its way toward the target allocations using new deposits. (Again, you can choose to rebalance at any time, and it’ll sell/buy securities until your target allocation is back to where it started.)

Altogether, it’s a fascinating platform. My main concern is the spreads paid for portfolios buying many different issues. As such, I try to construct portfolios that use the most-liquid options available to limit trading costs.

The Good Stuff

M1 is great for behavioral investing. While I like to keep most of my assets with Vanguard/Fidelity, I always enjoy having other smaller portfolios where I can “exorcise my demons”. This lets me stick to my boring investing plan while still having fun in the market.

Their current margin rates are around 1.6% (and I believe this goes to 2.6% when M1 Pro expires, which costs ~$90/y or so), which is an incredibly competitive rate.

Companies and ETFs each have their own logo, and everything is organized into slices/pies. The application on iOS and desktop looks sleek and well-organized. The feature I like the most is the ability to design my own portfolios, and share them with others. There’s thousands of portfolios available to browse through. You can add them to your portfolio, use them entirely, or mix and match many different portfolios into one.

The margin rates are very competitive, which should be a great tool for taxable accounts that wish to spend against their portfolio value rather than selling securities. It’s also great for those wishing to use a bit of leverage. I do encourage people who are younger to put on some leverage, usually 10-30%, but this increased exposure/risk can scare people out of the market, so it needs to be done with caution (and hopefully the advice of a professional).

Their product offering is pretty impressive for a newer firm, and I think they’re doing a good job. You could theoretically use M1 for all of your finances, from investing, to checking, and savings. Their 1% APR is pretty competitive, and 1% back on debit transactions is great. Unfortunately, you need M1 Pro for some of the features, like the credit card. Rather than an annual fee, it’s part of the M1 Pro package.

I’ve had an absolute blast making portfolios and sharing them. I can invite my friends on and even create portfolios specifically for them. I love the pie/slice system, which lets me organize everything exactly how I like. It’s just plain fun. I find myself checking the app and tinkering around a lot, and if I’ve learned anything, it’s that it’s important that we are happy/content with investing.

Portfolio Construction

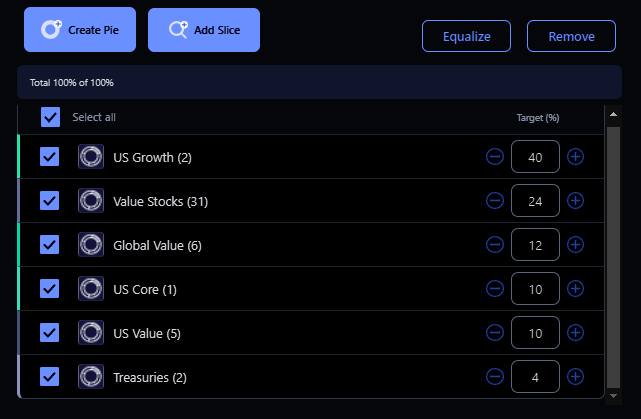

This is the fun part to me. You can select from virtually the entire universe of listed stocks and ETFs. I do think this will trip-up some novice investors, who may not appreciate the effects of buying fractional shares. That said, I was able to find all the ETFs I needed (although some low-liquidity and newer ETFs aren’t listed, like $AVLV).

I’ve been working on several portfolios that I can share with others. I’ve always loved building portfolios, but it’s usually something I do on-the-job and can’t share with my friends or FinTwit. However, I can make my own M1 portfolios and share those!

While building my portfolio, I did notice that if you decide to invest in stocks, that it’s very easy to create a wildly out-of-balance and volatile portfolio. As such, I would recommend sticking to ETFs and highly-liquid large cap issues. You want to ensure that everything you invest in is liquid enough, or you risk losing a chunk of returns.

M1 conducts their trading in blocks, which should greatly improve slippage compared with typical fractional share investing. They do take payment for order flow, which is to be expected with free commissions. Only Vanguard offers truly PFOF-free trading (Fidelity claims to not accept PFOF, which may technically be true, but they execute fractionals against their book and profit quite a lot off of trades, it just may not be called “PFOF” necessarily). All that said, PFOF is a part of retail trading, and I recommend mutual funds to avoid it.

If you’d like to invest in the same portfolio as me (or any part of it), all you have to do is click this link right here. I’m not an affiliate or being paid or anything, although I’ll get a $10 bonus for a referral (which will probably just go to my boyfriend, full disclosure). I only put 4% into treasuries. If you’d like the same portfolio but with 7% in treasuries, just click this link instead.

Portfolios:

Remember, you can alter these portfolios however you like. If you increase/decrease the treasury allocation, split the remainder between US Core, Value Stocks, and US Growth (in that order).

I’ve been building portfolios for ages, and must say that I wouldn’t recommend stock-picking at all, and that one of the drawbacks to M1 is that it does seem to encourage stock-picking. I recommend limiting your stocks allocation to 25-30% maximum, and ensuring you have at least 25 holdings, with nothing over 6-7% allocated.

That said, once you’ve learned how to use it, it’s rewarding and fun and a very interesting new way to invest. I have a very large number of portfolios that I’ve created, and am happy to share if anyone is interested in seeing others.

All-in-all, I’d give M1 a 9/10. I’d prefer if they didn’t do dynamic rebalancing, but there’s very little to complain about here. Using a simple portfolio of ETFs would, in my opinion, be the most efficient way to use M1. However, you don’t really need M1 to keep a portfolio of a couple ETFs balanced. It’s a big help when you use a combination of stocks and ETFs, which is what I’m doing here.

If you have any questions, just drop a comment or hit me up on Twitter. I love to help, and would very much love to see more people investing responsibly for the long-run, avoiding intraday trading, derivatives, and other habits that should probably be curtailed. No offense! I can overtrade sometimes too, it’s a very human instinct.

Much love, and good night. I have to go to work, and I’ll come back to add more here later.💕💕💕

—Avery

For those who’ve asked for it, here’s a link to my “Value Stocks” portfolio, click or copy-paste: https://m1.finance/vFY6My-QdWN5

Remember, I don’t recommend going over 25-30% in allocations to stocks, but you can slot this into an existing portfolio or add your own additions to it. You could, for example, put 75% into $SPY and the rest into this portfolio. You could go shopping and pick out portfolios on the site, or build your own from the bottom up!

Addendum:

Accounts are free to set up, and there’s a bonus if you deposit X amount in your first 14 days. You can also transfer accounts to them, for which they’ll give you a pretty decent bonus payment for. However, they appear to charge $100 for outbound transfers and another fee for closing an IRA. As such, I would not recommend sending a Fidelity portfolio here, as they may deny paying for a transfer BACK to Fidelity if you decide you don’t like it.

Instead, I’d send it to IBKR and *then* send it to M1. Fidelity is where I send my funds when I need my transfer fees reimbursed, but they typically only reimburse accounts with 25k, although they’ll cover fees for smaller accounts upon request.