Macro Rundown: Japan

Macro Rundown: Japan

Expect the BoJ to end NIRP and widen the 10yr YCC band in 4Q '22

The Nikkei 225/TOPIX

Since the epic boom-and-bust cycle of the 1980’s, the Bank of Japan has absorbed more debt than any other nation. However, the Nikkei has returned more than the S&P 500 over the past 10 years.

For a long time, many investors have written off the idea of investing in Japan. While the N225’s returns can be more volatile, it has routinely returned more than the SPX. Not until 2021 did the S&P 500 finally catch up with Japan.

The Nikkei has had quite a good run over the past 10 years +186.77% before dividends.

CPI and Core Inflation

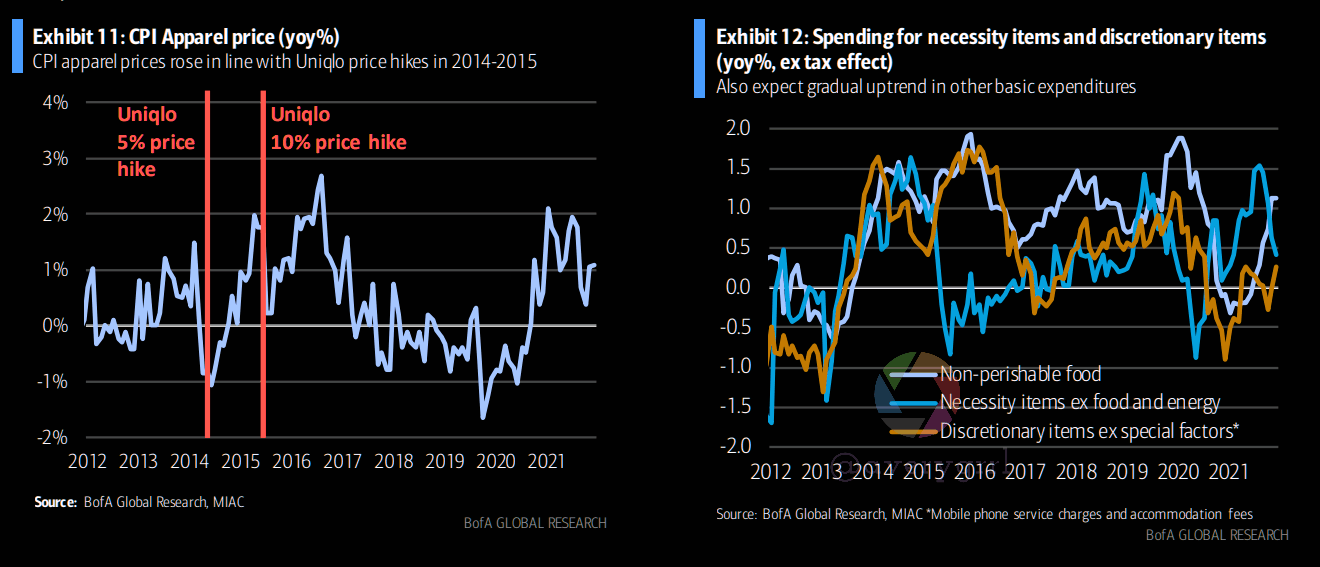

Japanese CPI remained muted during 2021, despite global inflationary trends. Japanese corporations were cautious about passing on their higher input costs amidst a slow economic recovery. Economists have raised their inflation forecasts. Rising commodity prices and cost-push inflation can be expected to affect a large number of goods, including consumer staples and apparel.

Japan-style core CPI (ex. fresh food) is forecasted near .75% YoY, but it seems safe to assume a >1% YoY target. For Japan-style core inflation, many, including myself, expect some weakness. Core inflation should average under .5% YoY in Q1, but is likely to accelerate toward 1.5%, as cuts to mobile phone service fees and other subsidies fade. Expectations in the range of +0.7% YoY, but it may be safer to expect 1% or more.

The Bank of Japan can be expected to end NIRP (negative interest rate policy), and widen the band on 10y JGBs (Japanese Government Bonds) by EOY 2022. BofA expects a one-off adjustment of policy settings in October 2022, which would put an end to NIRP and shift the upper bounds of the 10y target band to 0.5% (currently 0.25%).

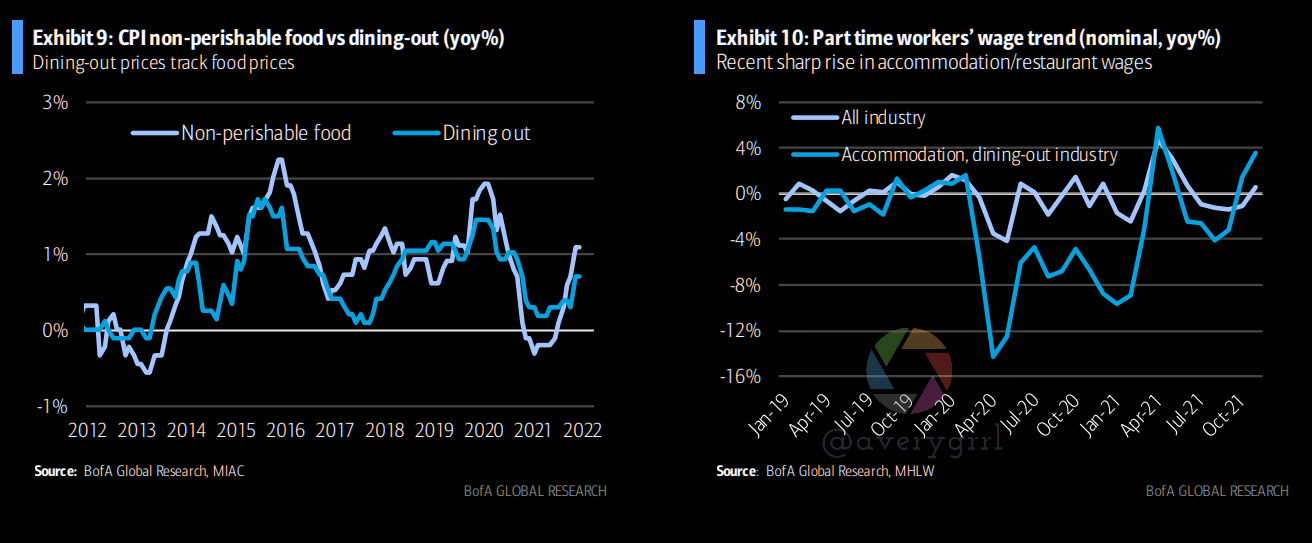

For April ‘22, CPI growth of 1.6% seems likely as energy prices spike and food prices rise, after wide-ranging price hikes were announced in December ‘21. Other CPI components such as restaurant services should also push up CPI numbers.

Japan Macro Outlook

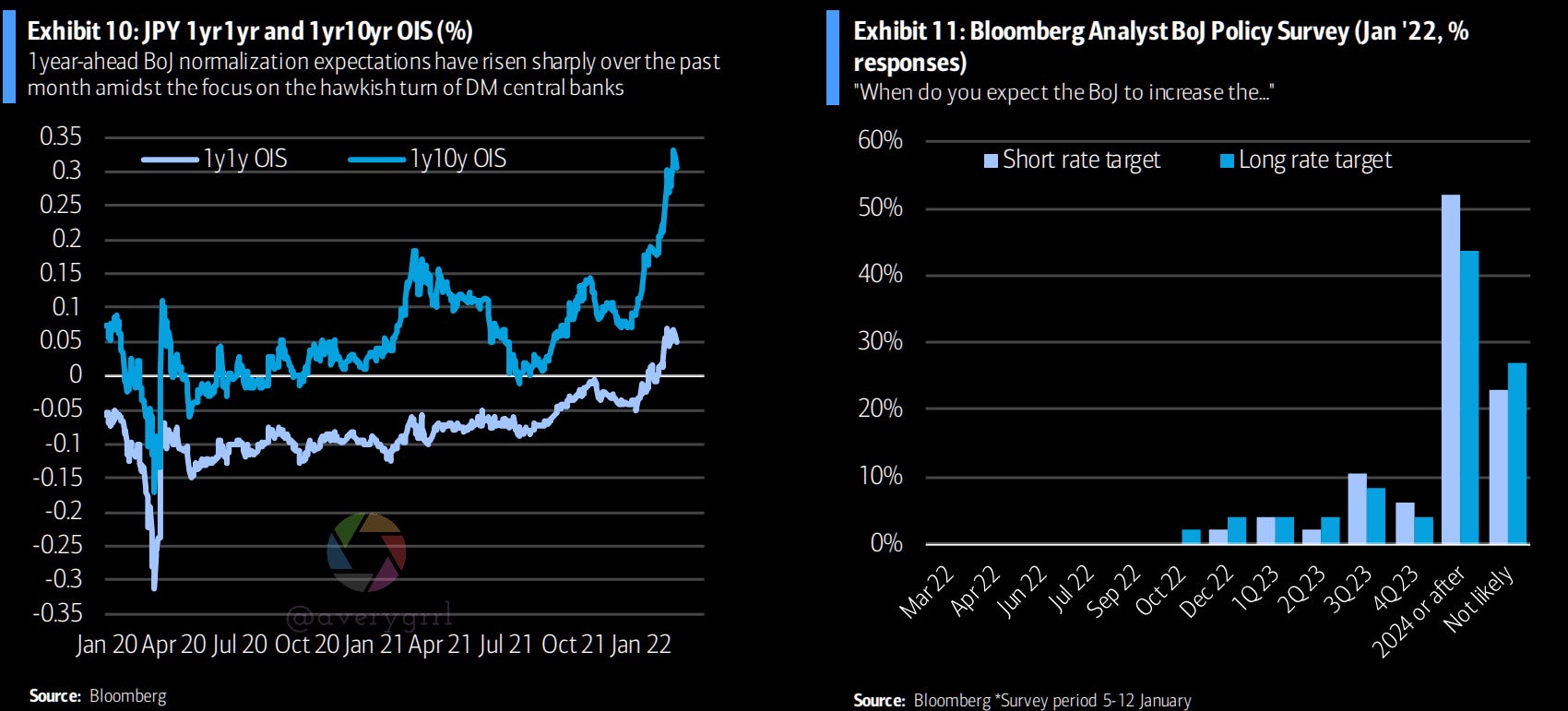

The markets have grown more and more sensitive to potential BoJ hikes, as inflation is expected to pick up sharply from April ‘22. The BoJ’s forward guidance doesn’t prevent the BoJ from making adjustments to rate targeting before achieving 2% inflation. With pressure to bring forward normalization and grow over the coming quarters, rising costs for food and energy could trigger a backlash from households.

This has traditionally resulted in lower political support for the BoJ and its easing policies. As global central banks, including the ECB give more room for BoJ action, it can now normalize negative rates without risking unnecessary appreciation in the Yen.

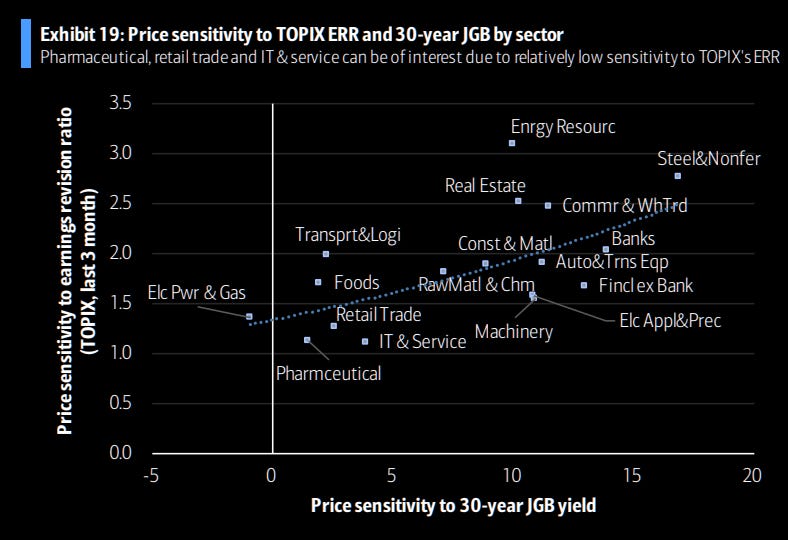

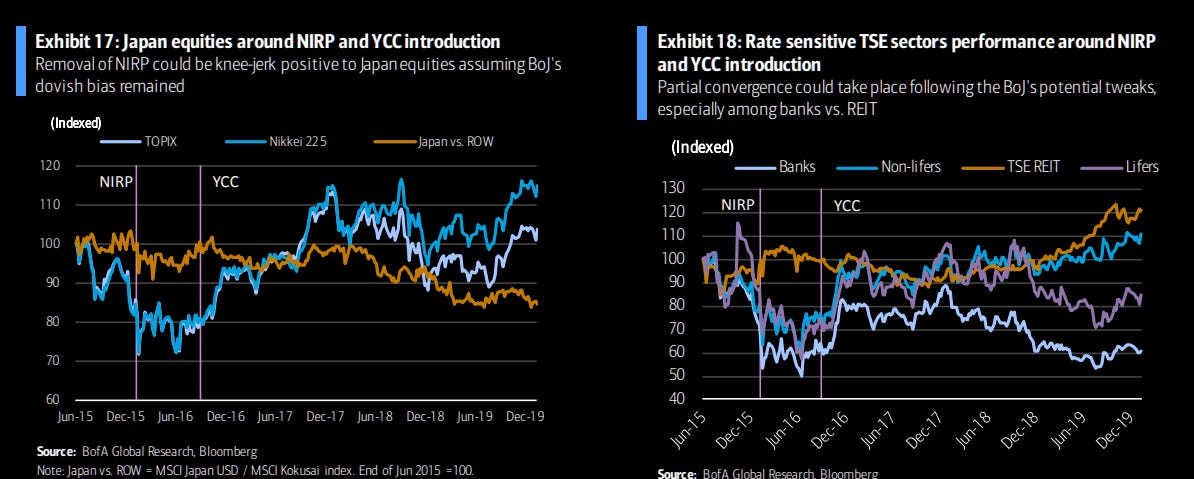

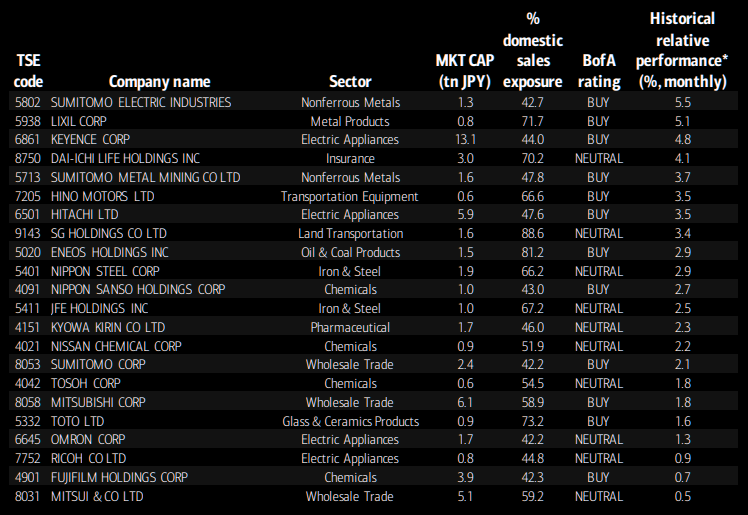

I believe a “dovish hike” could be a big positive for Japanese equities, as key rate-sensitive sectors converge. For example, banks vs. REITs, life insurers vs. standard insurers, etc. BoJ policy tweaks and cyclical dynamics could be a boon to pharmaceutical, retail trade, IT, and service sectors.

Since 2000, names with high domestic sales exposure outperformed the TOPIX as the US yield curve bear-flattened alongside JGB curve bear-steepening:

Pretty impressive outperformance. Current BofA ratings included.

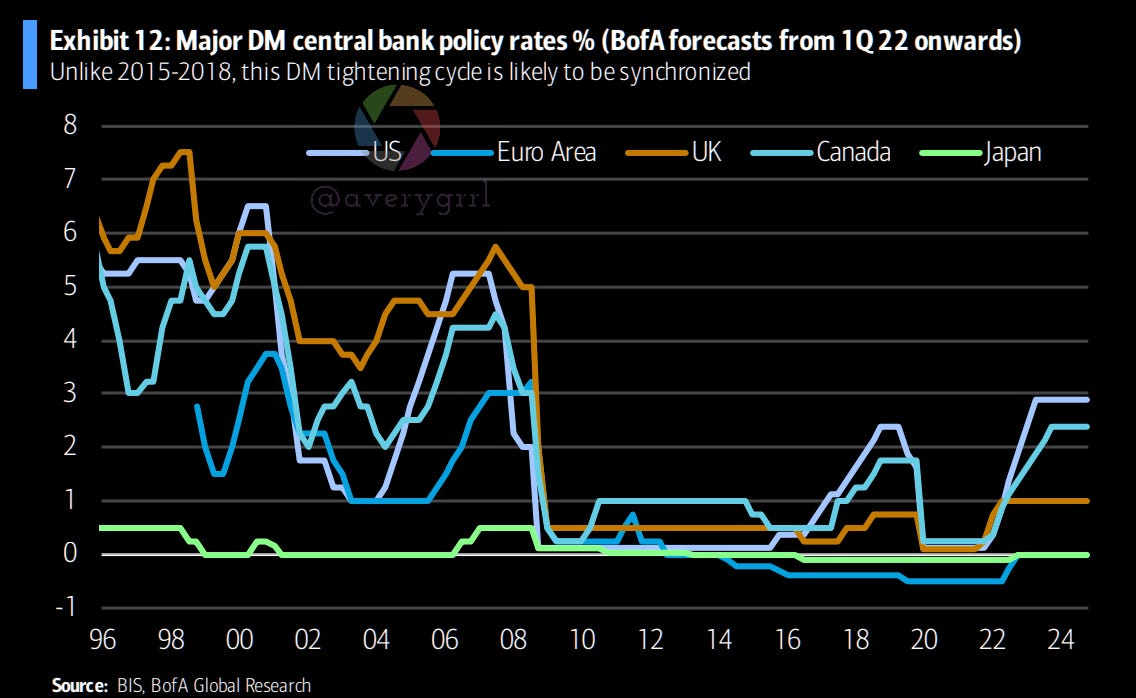

A surge in global inflation has pulled forward hiking cycles for CBs around the world. Rate hike expectations from the Fed have risen from +70bp to +140bp in 2022, and from 10bp to 40bp for the ECB.

Market pricing of Fed/ECB hikes / Headline CPI for major DMs

The BoJ does not need to follow other CBs in tightening, and Governor Kuroda has struck a dovish tone, signaling a shift in thinking within the BoJ.

In its January 2022 outlook, the BoJ policy board adjusted its view on inflation risks for the first time since October 2014 (now classified as “generally balanced”, after being “tilted to the downside” for 7.5 years.)

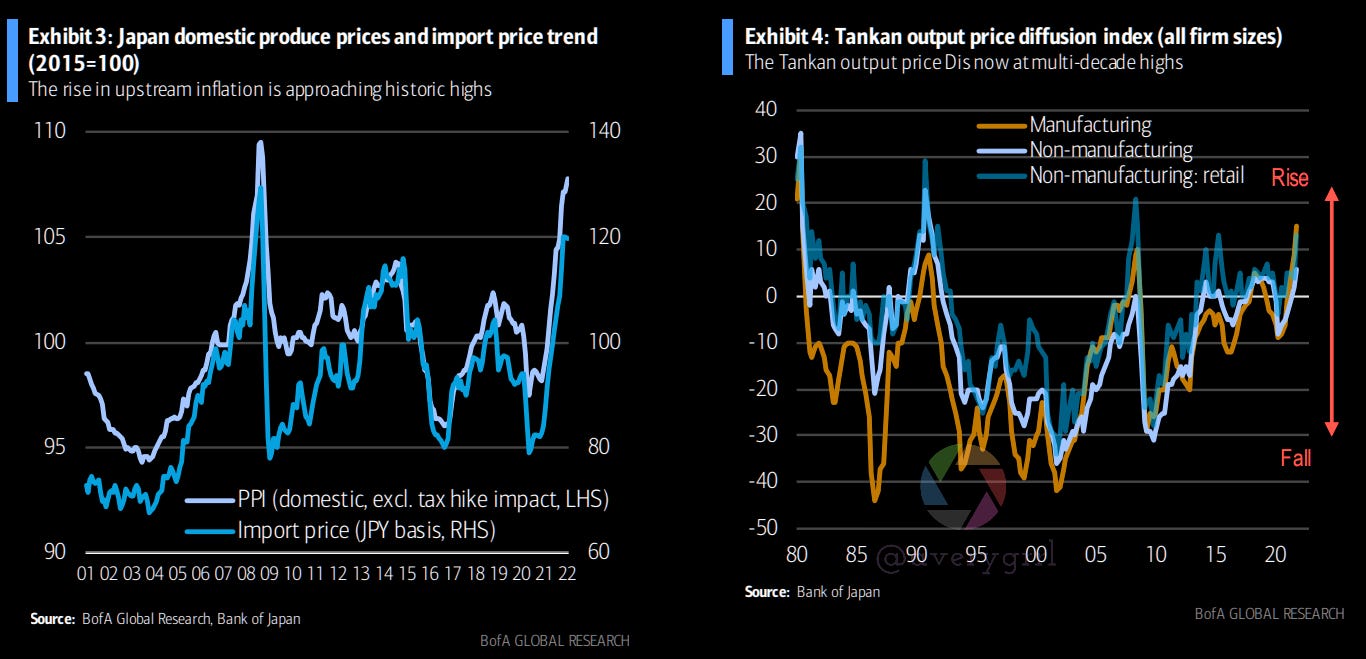

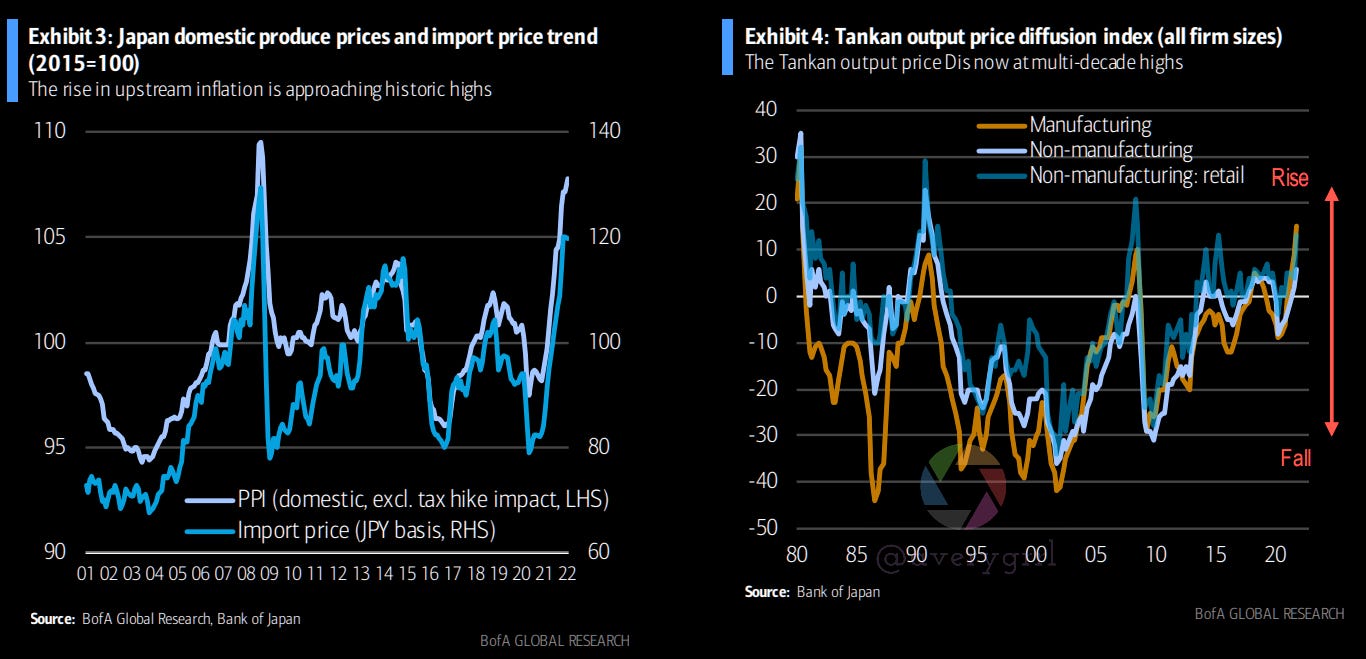

The BoJ seems to be confident about economic recovery, and the policy board also upgraded its growth assessments as the effects of CV19 have waned. Take another look at exhibits 3/4 from BofA:

Inputs costs have been rising, and consumer inflation in 2022 should be significant by historical standards. However, it does not appear that inflation above 2% can persist.

Certainly, there are risk factors and inflation could potentially remain elevated through 2023, especially with rising energy costs. There’s also potential for additional price hikes, although so far this has mostly been constrained to those dining out.

The Japanese labor market has become particularly tight for part-time workers, who are a bulk of the employees in the restaurant sector. This, coupled with reopening at home and abroad could trigger additional price hikes. This would mean ex-energy core inflation remains sticky above the 1% range for longer than consensus.

Once more, we should take a look at CPI data.

BoJ Rates and Policy Adjustments

The BoJ’s forward guidance hasn’t ruled out policy adjustments. While the BoJ’s forward guidance expects “short- and long-term policy interest rates to remain at their present or lower levels,” this does not prevent the CB from making adjustments before 2% inflation is achieved.

The guidance, introduced in Summer 2018, has been revised three times, and links the commitment to keep rates unchanged to uncertainties around CV19.

This does not mean that the BoJ will hike as soon as it judges CV19-related uncertainties have diminished, but it does create an opportunity.

BofA has a nice piece on the “four layers of BoJ forward guidance”:

As markets grow increasingly sensitive to BoJ hikes, only 1 in 48 analysts from Bloomberg’s latest policy survey (5-12 January, 2022) expected the BoJ to end NIRP by December. Only 3 respondents expected changes to the 10y yield target.

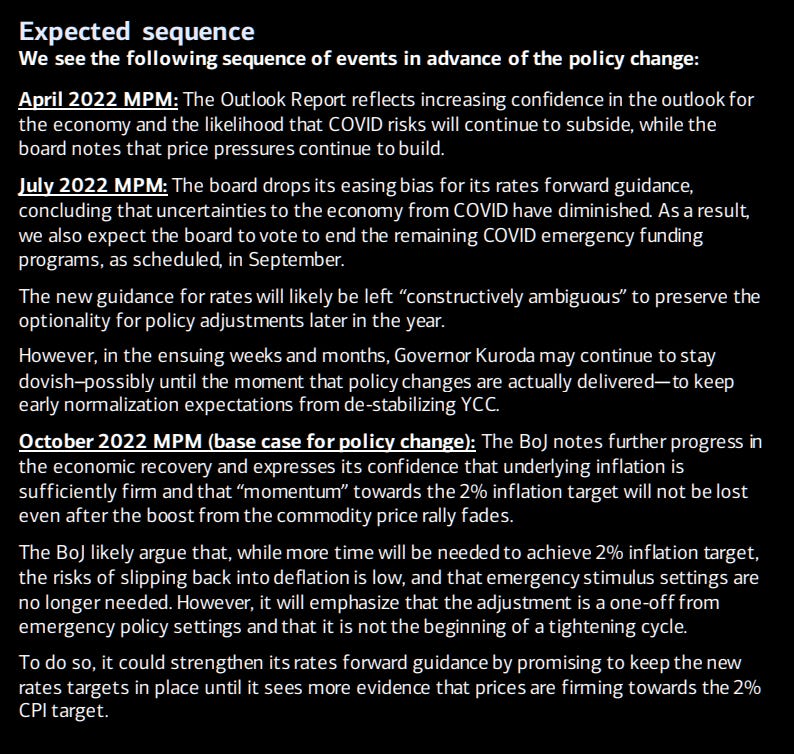

BofA has outlined the following sequence of events in their expectations. This seems very reasonable:

The BoJ seems likely to announce these changes in October, but any meeting between July ‘22 and January ‘23 are possibilities, as long as the expected jump in core inflation from April 2021 comes to pass. CV19 uncertainties will need to remain sufficiently diminished for the BoJ to change its forward rates guidance.

Beyond January ‘23, the end of Kuroda’s term, as well as the fiscal year-end loom, which may make the CB cautious about introducing volatility.

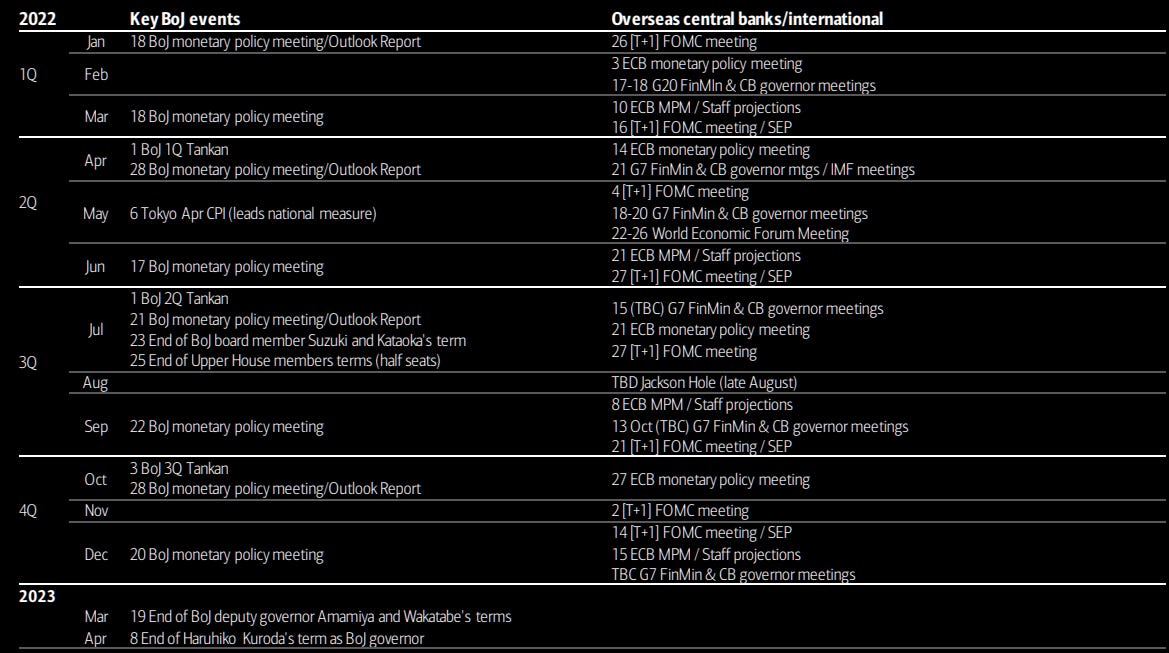

Timeline of key events:

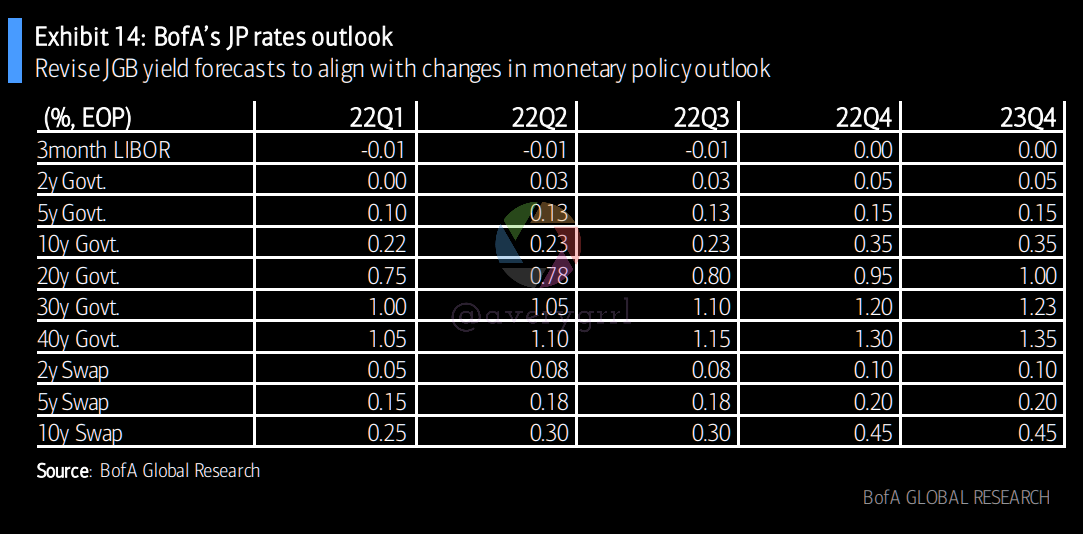

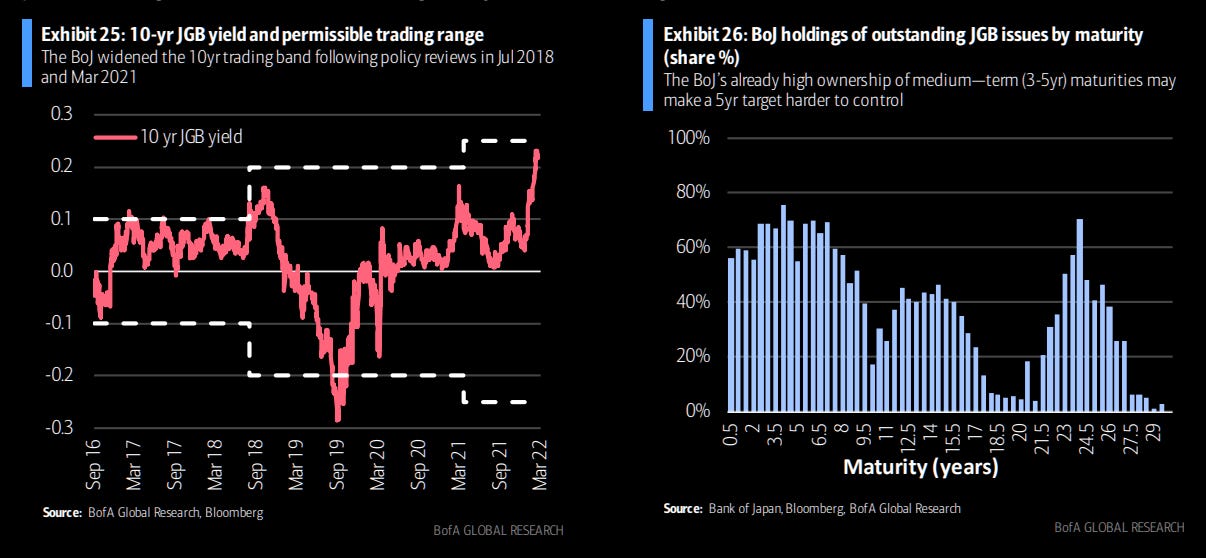

JGB yields should align with expected changes to the monetary policy outlook. Prior forecasts of a 10y JGB yield of 0.15% at the end of 2022 seem a bit off, and we should expect something in the range of 0.3-0.4%. Currently, levels are at 0.21%. With many different maturities, it’s difficult to forecast rates for specific tenors, but 10y JGBs should remain appealing compared to others, even as issuance lifts off in April.

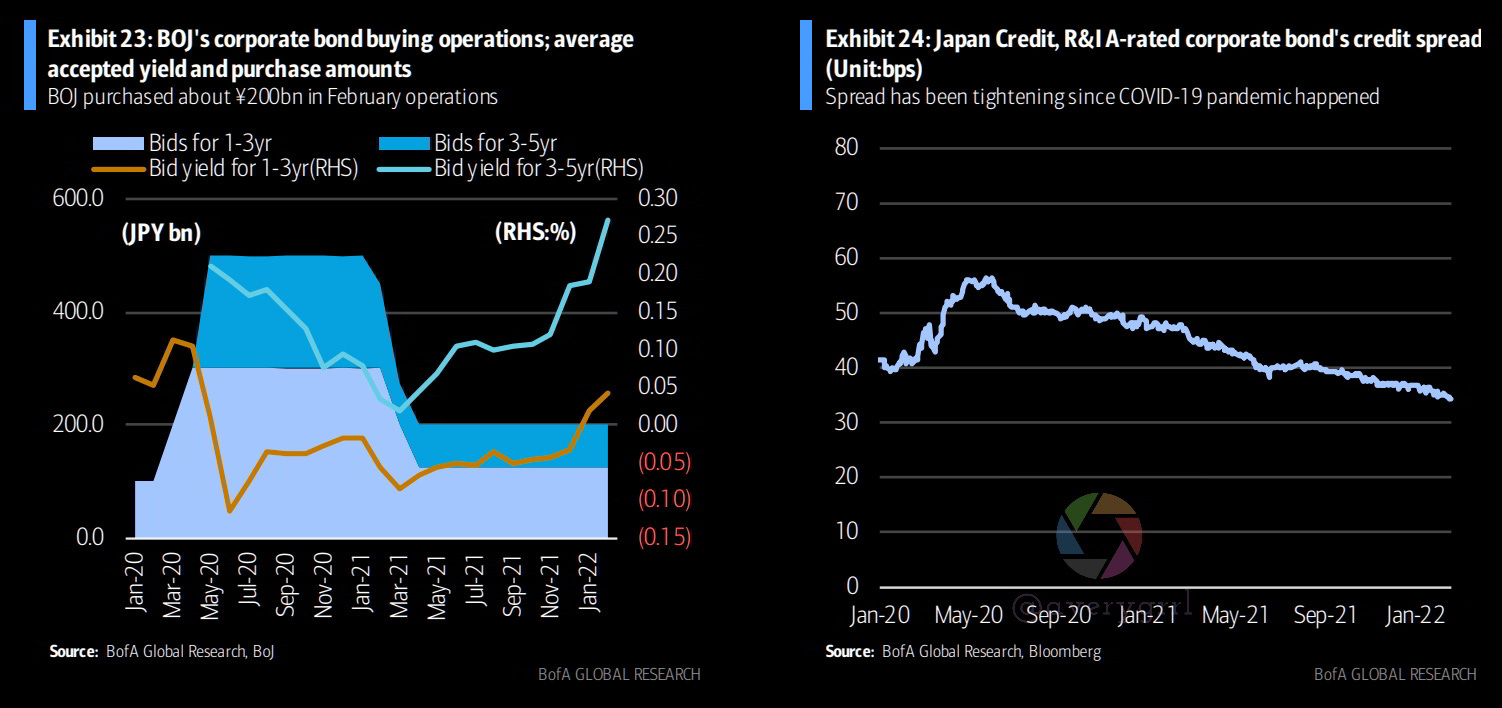

As of 10 February, the BoJ held 8.51 trillion JPY in corporate bonds. While the market is very sensitive to these holdings, the BoJ is quite unlikely to sell these bonds into the market. Reduced market intervention by the BoJ should be welcomed, as it could restore the bond market’s price discovery mechanisms.

Alternatively, investors and analysts believe the BoJ has the option to move for a YCC long-rate target, but I don’t think that’s as likely. The 5-year is more difficult to control, and when the BoJ begins shortening the long-rate target duration, markets may anticipate further shortening, de-stabilizing YCC (yield curve control).

The BoJ cannot afford to lose control over the 10y, and the market should expect guidance on how far the BoJ will let yields rise.

Have a great night.

—Avery