Rates and Flows

Rates and Flows

Market Update: US Rates and Deposit Flows to Larger Banks

I hope everyone is enjoying their weekend.

This week, the Federal Reserve increased interest rates by 25 basis points, raising them from 4.75% to 5.0%. Although the hike was anticipated, the committee's updated language in their guidance suggests that fewer rate increases may be necessary in the future. This represents a departure from their stance just a few weeks ago, when they suggested that the terminal rate might need to be higher than what was discussed in their December meeting.

Let’s begin with a couple charts, and then we’ll take a deep dive into rates, positioning, and flows. Rolling four-week average flows have remained positive since mid-January.

FMS results show perceived risks are at their highest levels since 2009.

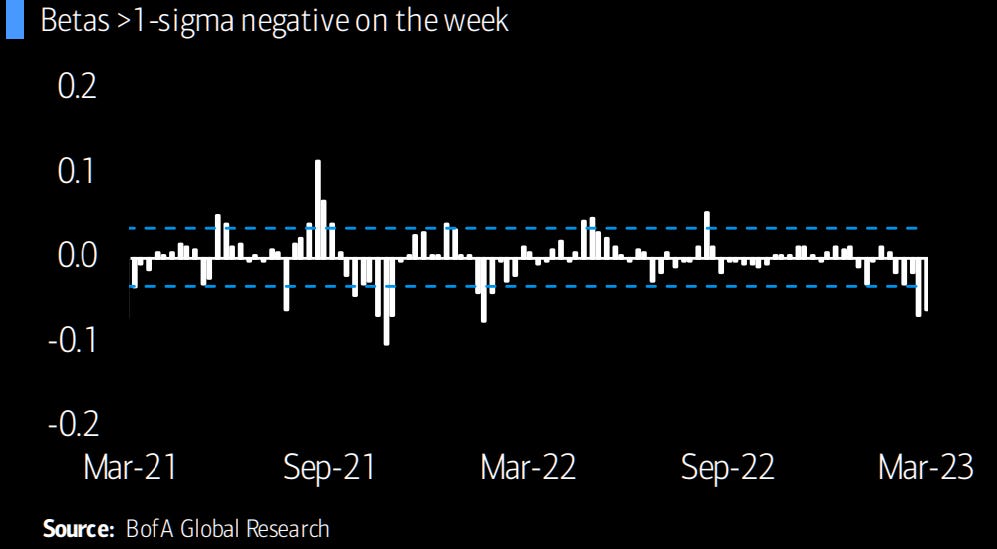

As we head into the weekend, indicators reveal significant out-of-the-money short positioning that remains exposed to covering.

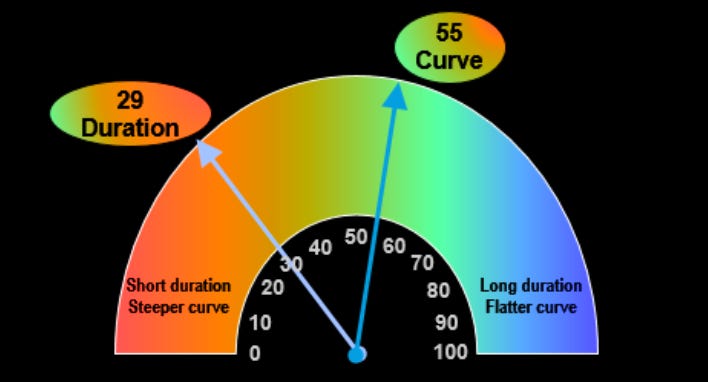

“The Curve-o-Meter”

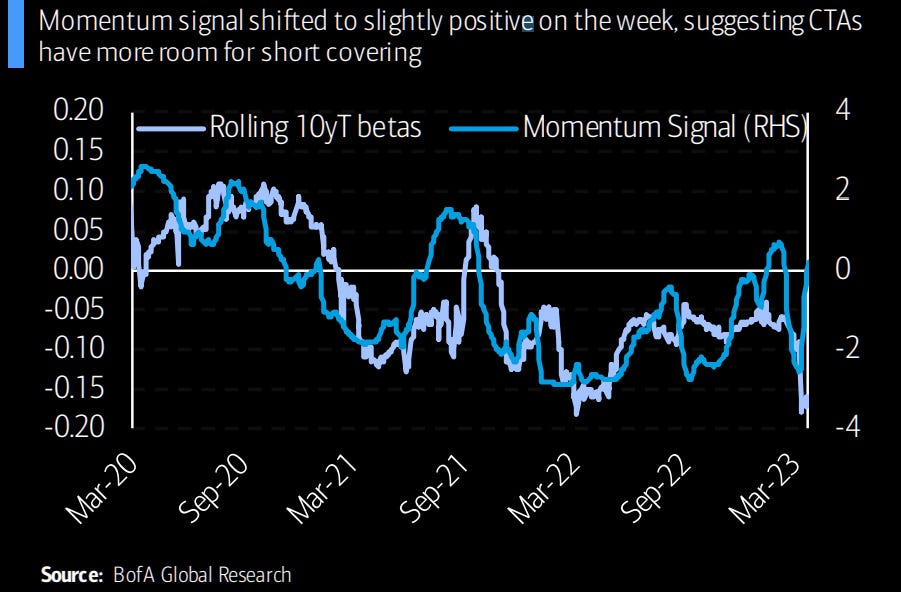

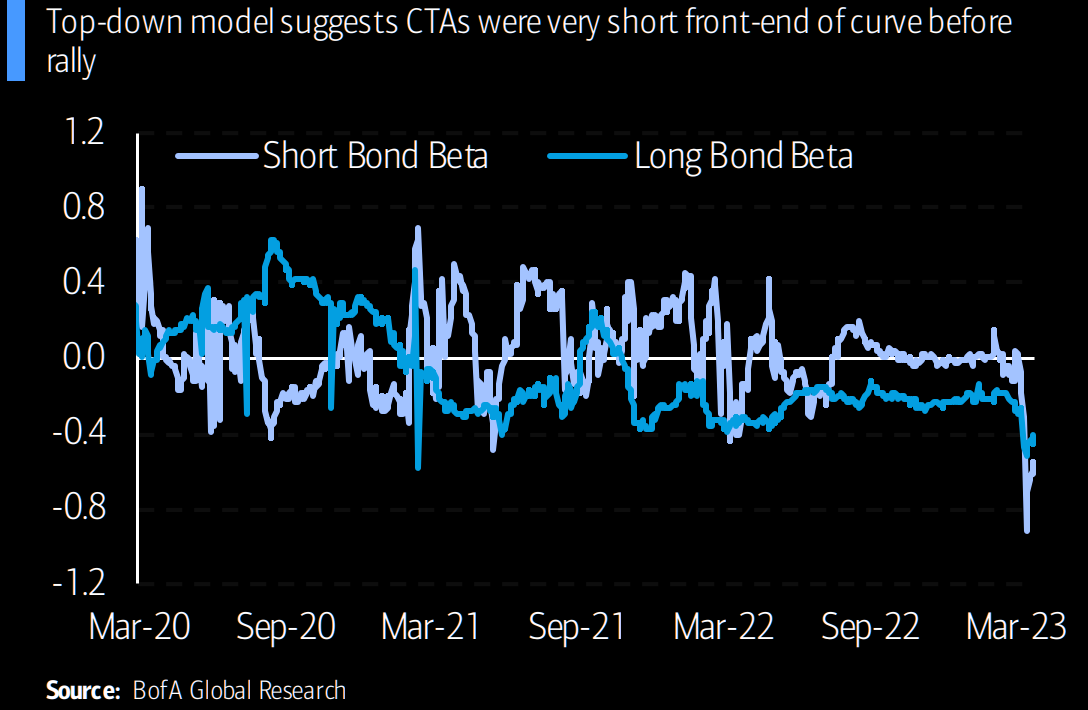

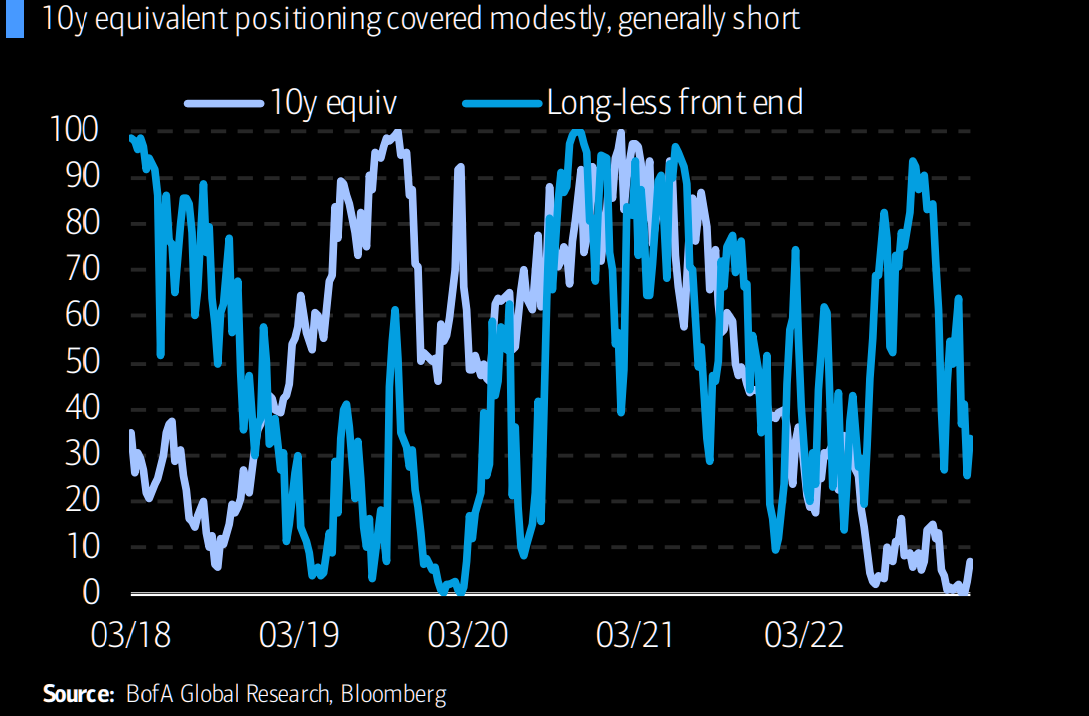

Futures positioning suggests rates are inclined to rally, while the CFTC data up to March 21 highlights a persistent short speculative community, despite some covering in SOFR futures. Momentum signals indicate CTAs would likely have covered shorts by now and be modestly long, though this deviates from the top-down model used by BofA.

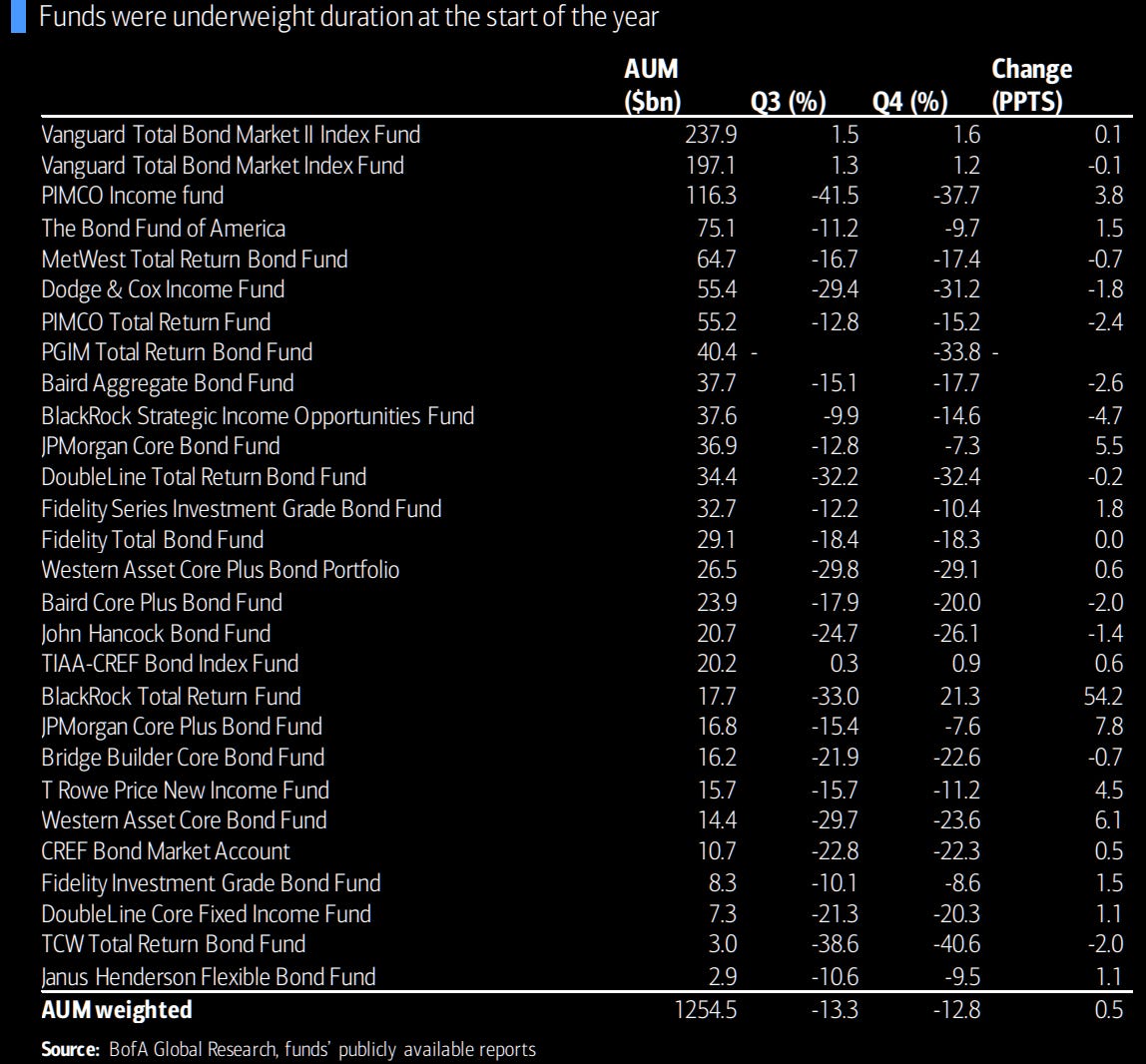

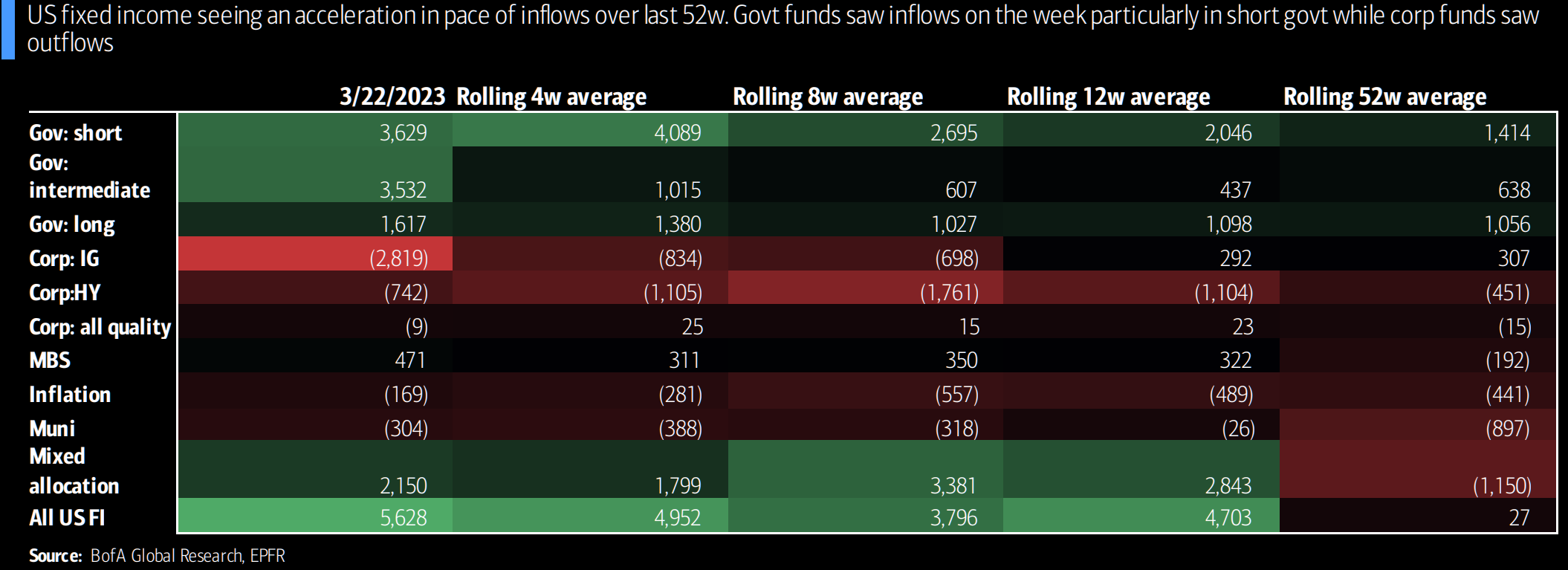

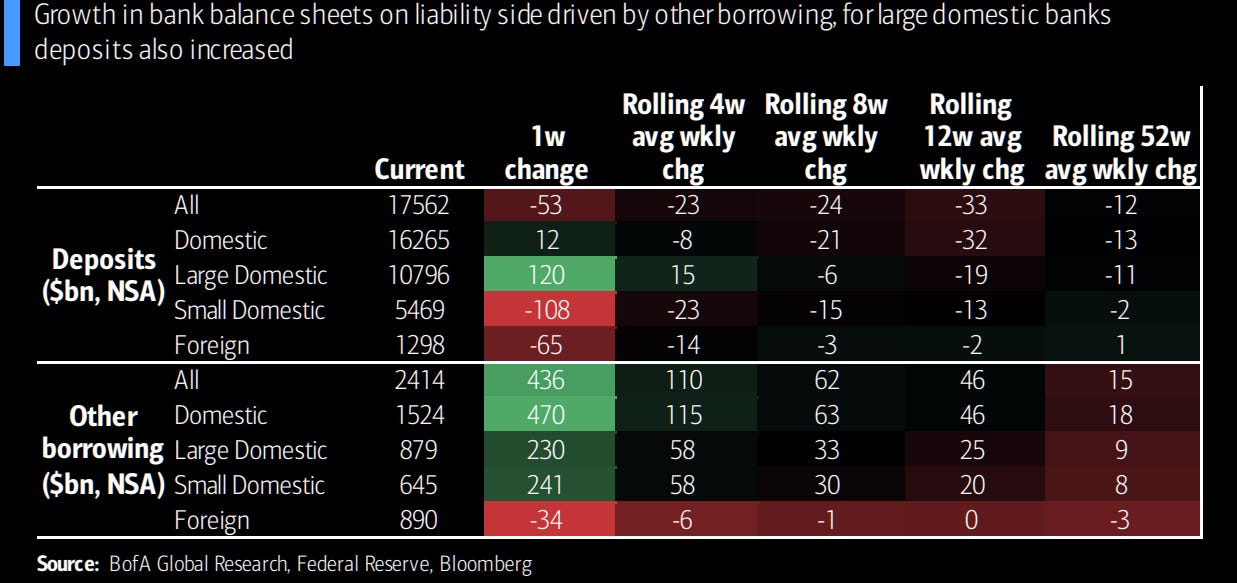

A strong flight-to-quality bias is seen in fixed income flows, with significant inflows to US government funds and outflows from credit funds. Aggregate benchmark funds may have reduced underweights given their modest outperformance during the week. Fed data reveals that US bank deposits changed little in the week ending March 15, but the data indicates a shift from smaller to larger banks.

Analysis of proxies for futures positioning: Shorts mostly OTM and prone to covering (except at the back-end.) Bias is for rates to rally.

TU: The two-year Treasury Note futures contract

FV: The five-year Treasury Note futures contract

WN: The 10-year U.S. Treasury Note futures contract

US: The 30-year Treasury Bond futures contract

UXY: The Ultra U.S. Treasury Bond futures contract

Futures positioning continues to imply a rate rally bias, particularly in FV and US, which have the highest concentration of OTM shorts. Throughout the week, open interest increased, predominantly driven by longs created in FV. Shorts were mainly concentrated at the curve's back-end, suggesting new curve steepener positions against longs established in FV.

While crossover momentum signals swung notably, they now indicate that CTAs hold a slightly long duration position. Top-down modelling reflects limited covering due to a 3-month lag in rolling 10yT beta. CTAs appear to have a more subdued reaction to the momentum signal compared to history, possibly due to their ongoing efforts to develop complex trading signals and proprietary models amid rising macro uncertainty.

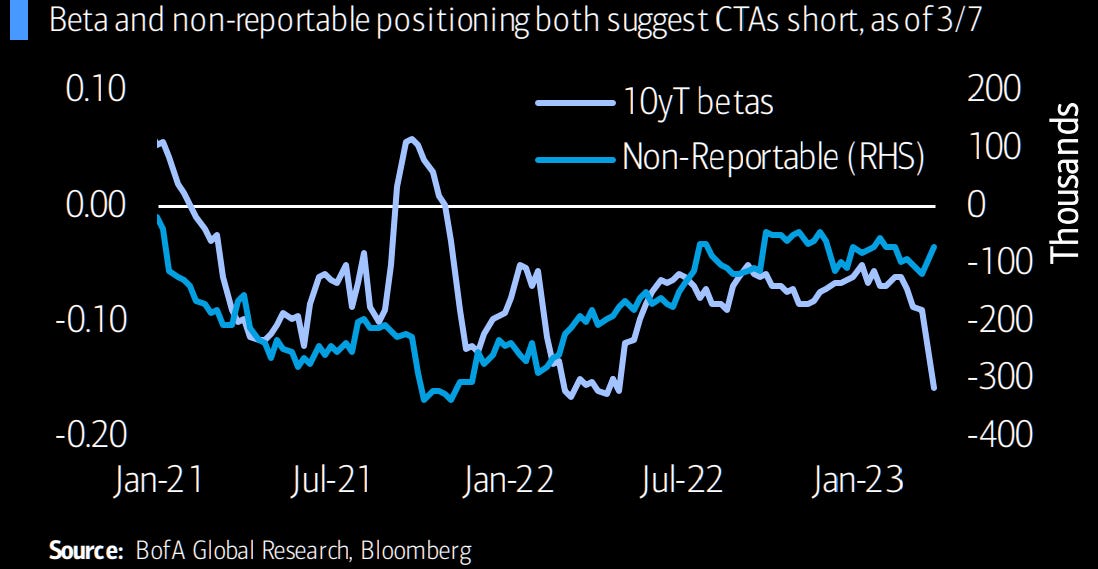

CFTC non-commercial positioning remains historically short but shows signs of covering (Image 4).

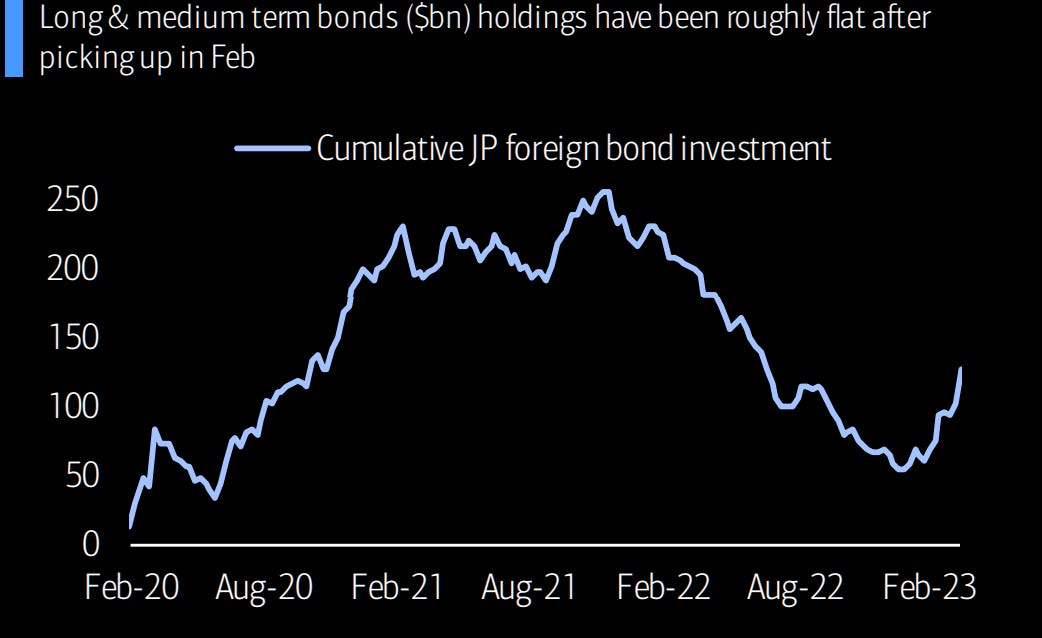

Shorts increased in FV and TY for the week ending March 21, with notable covering in SOFR and modest short covering across US, UXY, and TY. Ministry of Finance data reveals a strong Japan bid, as Japanese investors bought approximately $25 billion in foreign bonds in the week ending March 17. This likely reflects real money buying on a non-FX hedged basis, given the high hedging costs and potential window dressing behavior ahead of the Japanese fiscal year-end.

Japanese investors could re-enter the US treasury market if they gain more confidence in a bullish rates outlook for Treasuries versus uncertainty around JGBs, especially alongside expectations for a hawkish Bank of Japan rate adjustment later this year.

Foreign custodial holdings experienced a $72 billion drop from Wednesday to Wednesday. This decline largely represents US treasuries used in repo with the Fed to access USD cash rather than foreign official selling. The Fed facilities have helped prevent UST fire sales as banks and other institutions require additional liquidity in recent weeks.

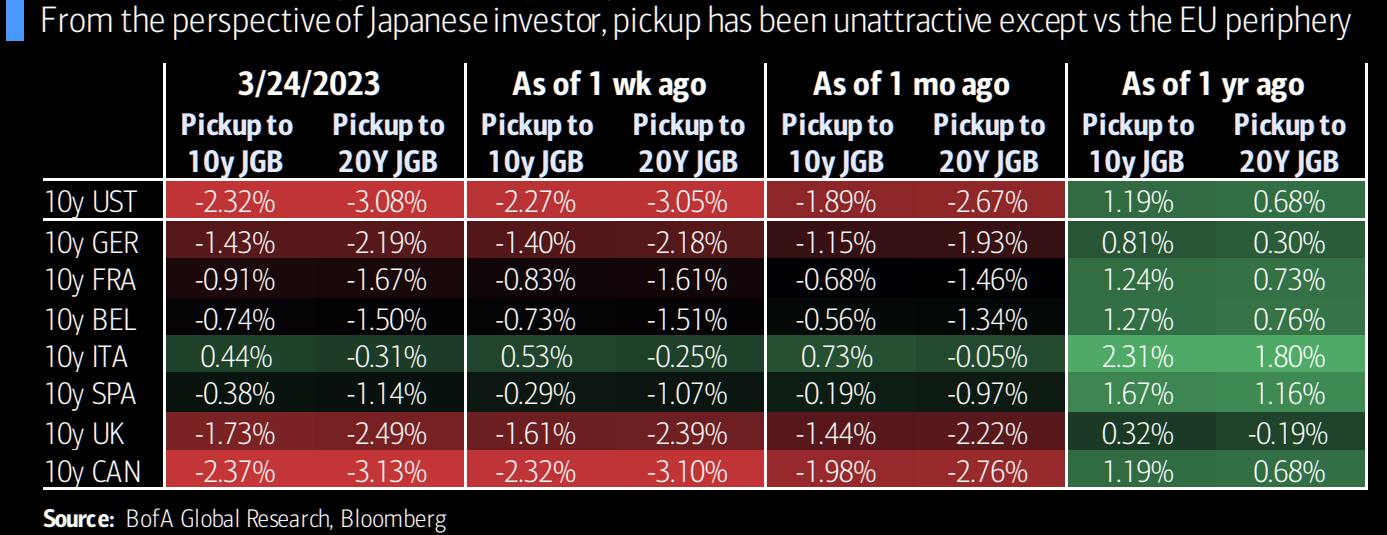

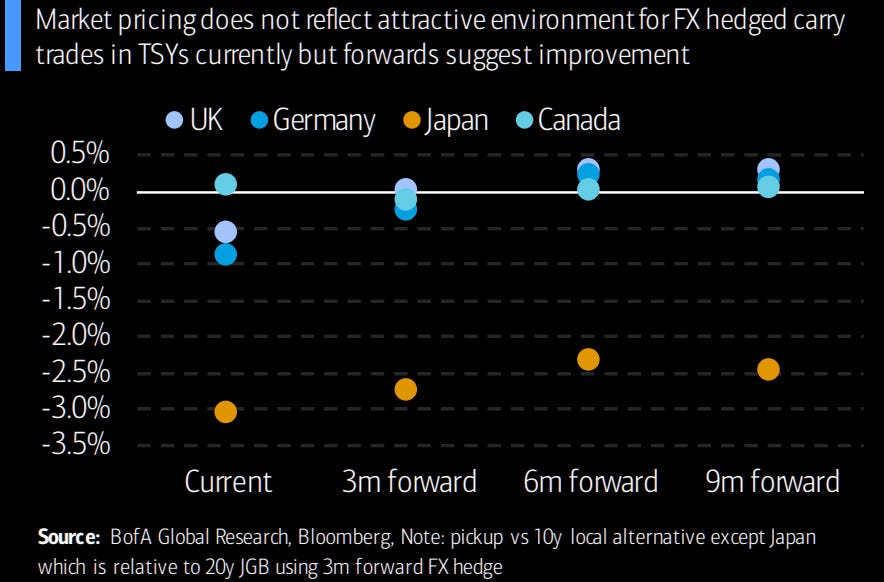

FX hedged pickup and foreign flows

FX hedged pickup of TSYs vs local alternatives implied by forwards:

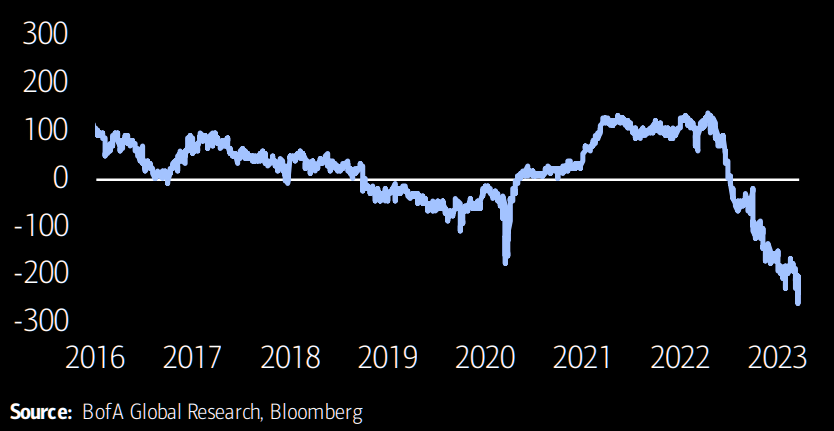

10Y UST pickup to 20Y JGB, with 3m fx hedge (bps):

10y TSY now offer very negative hedged pickup vs 10y JGBs

Fund flows and returns

US fixed income inflows accelerated this week, totaling $5.6 billion, reflecting a strong preference for UST funds versus credit. We can take a positive sign from relatively contained money market inflows, reflecting that cash may not be fleeing the banking system at large.

Aggregate benchmark funds demonstrated modest outperformance alongside the continued decline in rates, possibly due to funds covering shorts given the macro backdrop shift

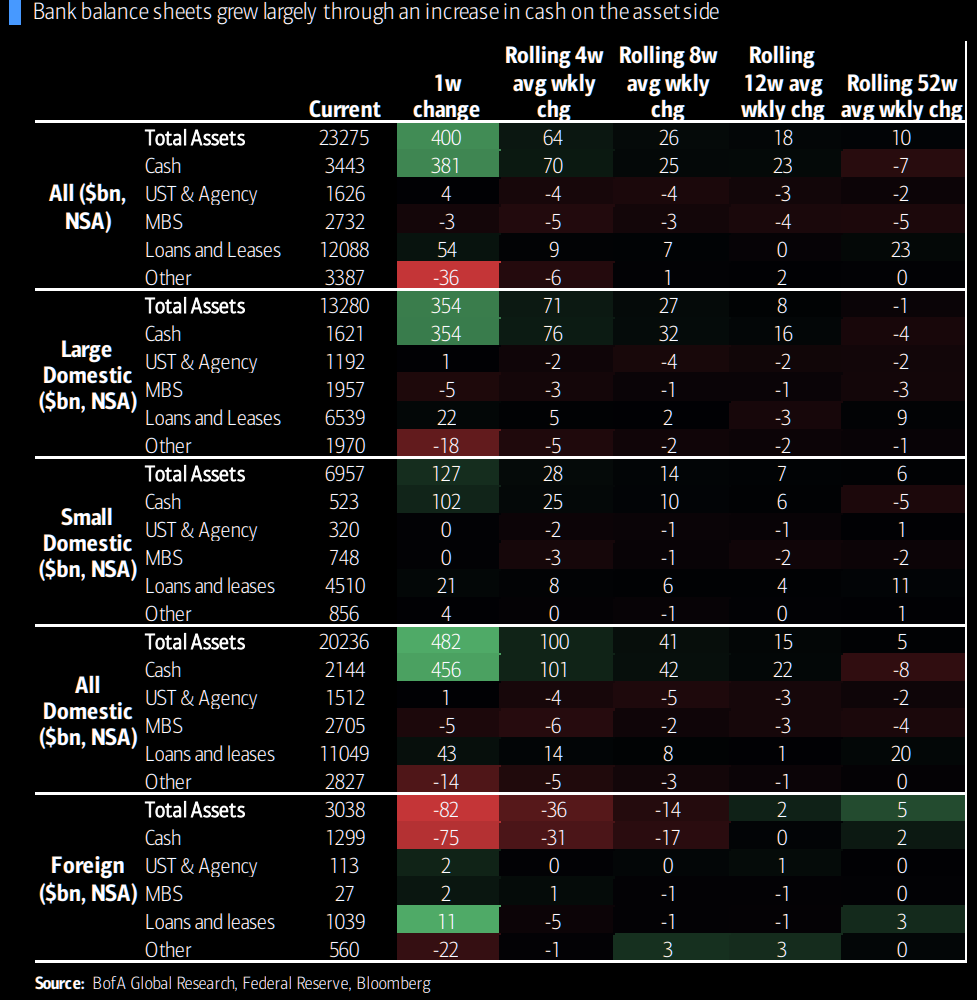

Data from March 15 shows the US banking system balance sheet grew by roughly $480 billion.

On the liability side, growth was primarily driven by borrowings from FHLBs and Fed facilities, totaling $470 billion. Although deposits remained largely unchanged, they shifted within the US from small banks (-$108 billion) to large banks (+$120 billion). This aligns with expectations of limited deposit outflow from the banking system, no significant securities sales, and high reliance on FHLBs and Fed credit facilities for cash sourcing.

Bank Balance Sheets

Private Client Stock/ETF flows

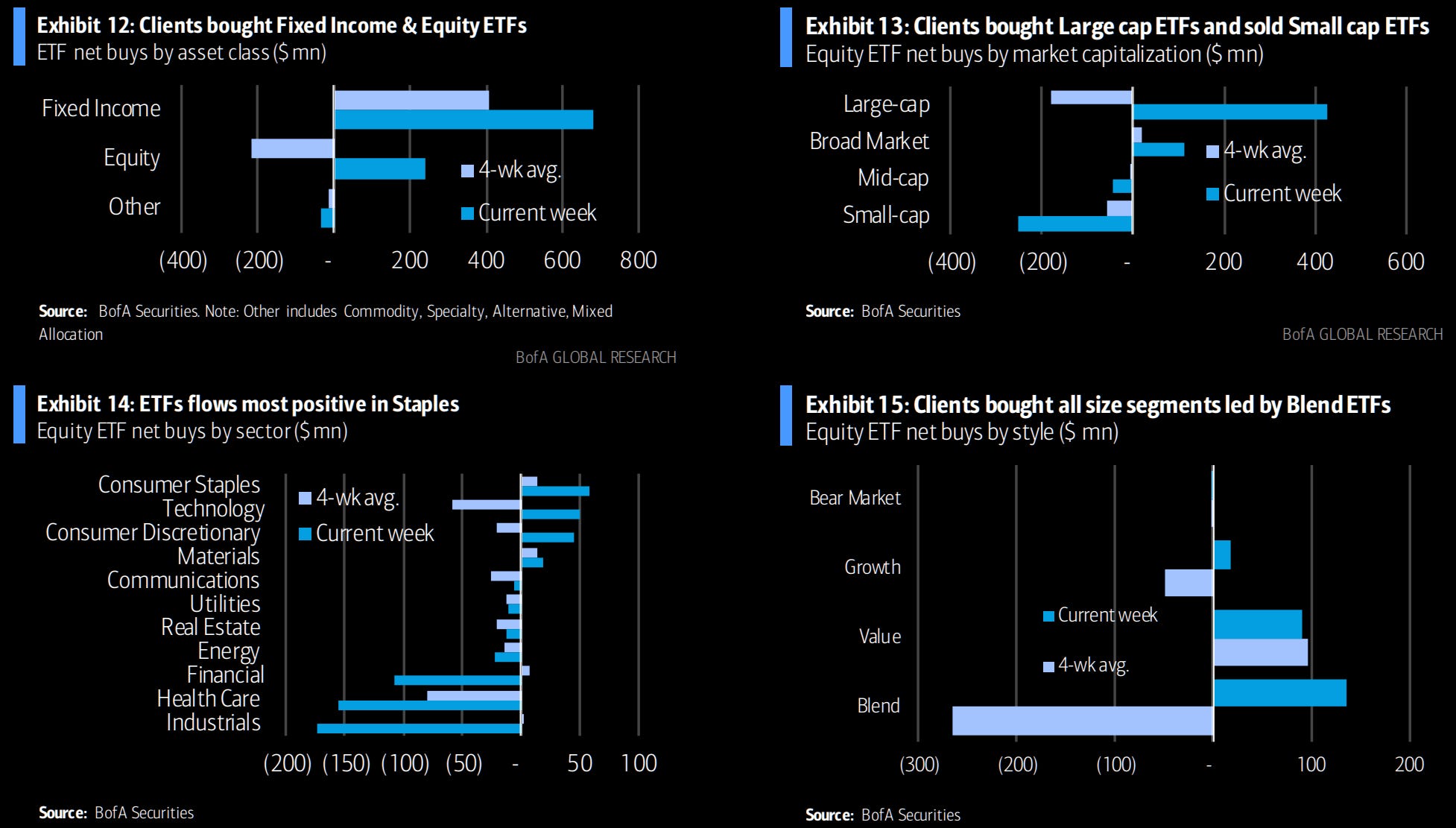

Finally, a quick look at equity flows:

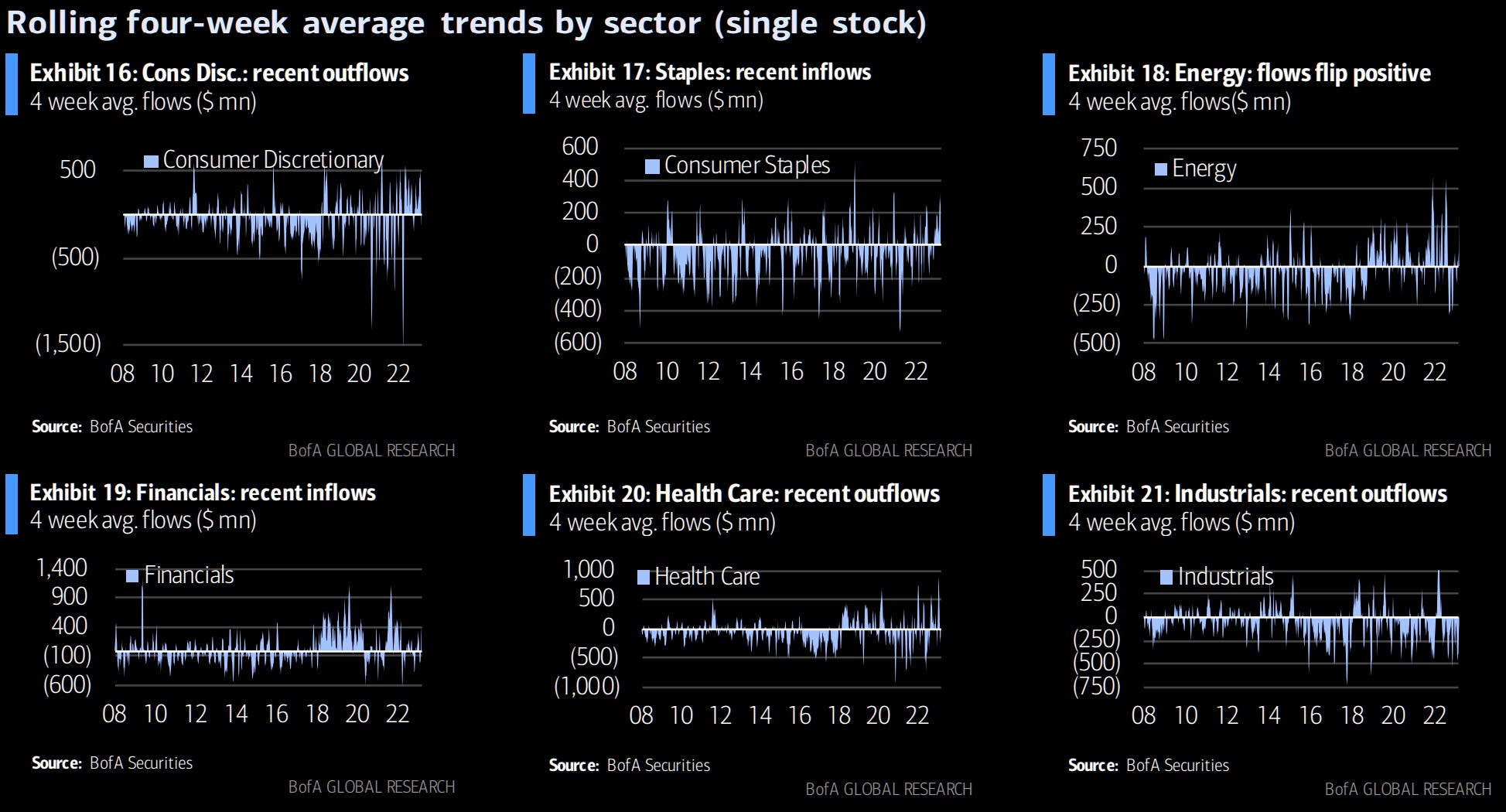

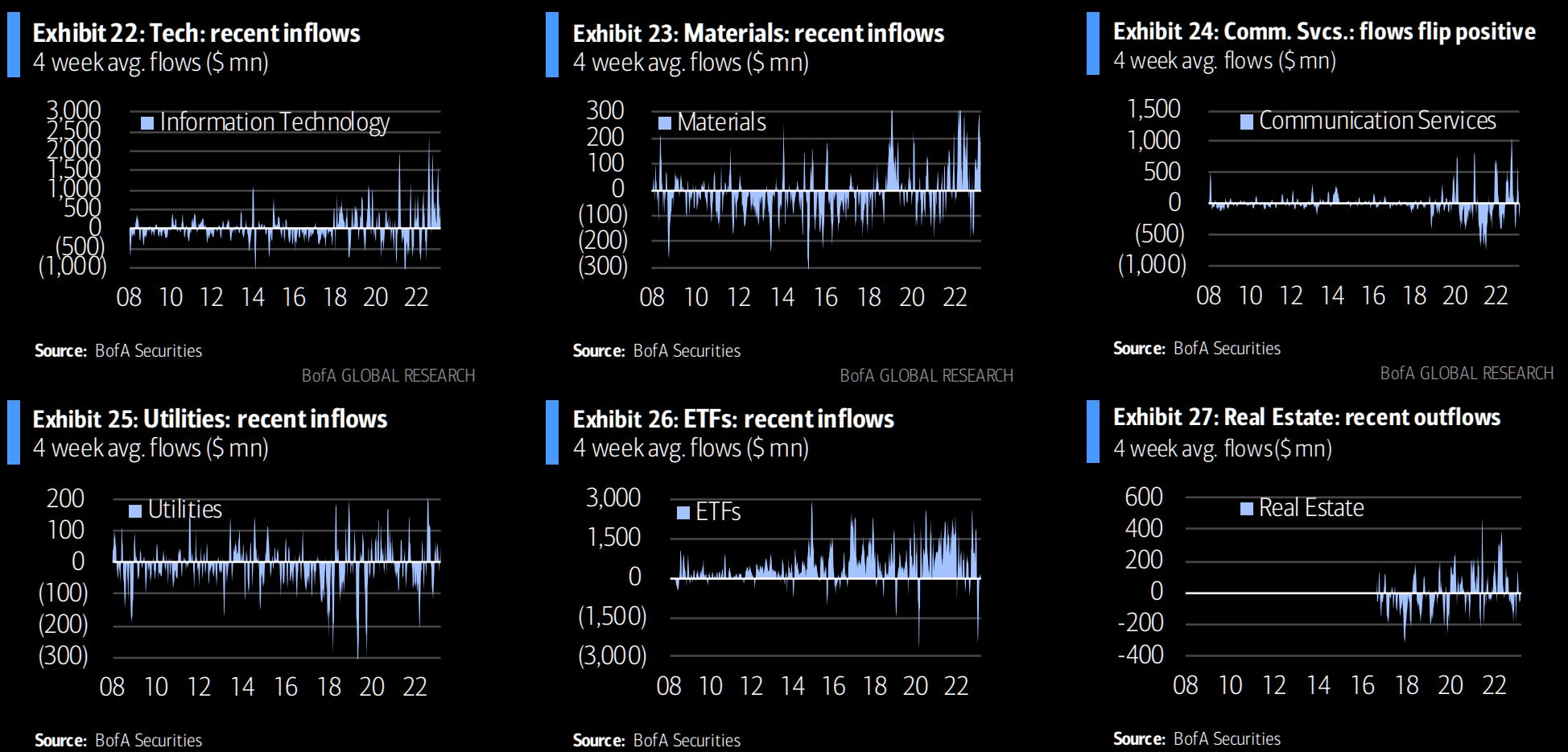

Sector trends:

Sector trends (continued):

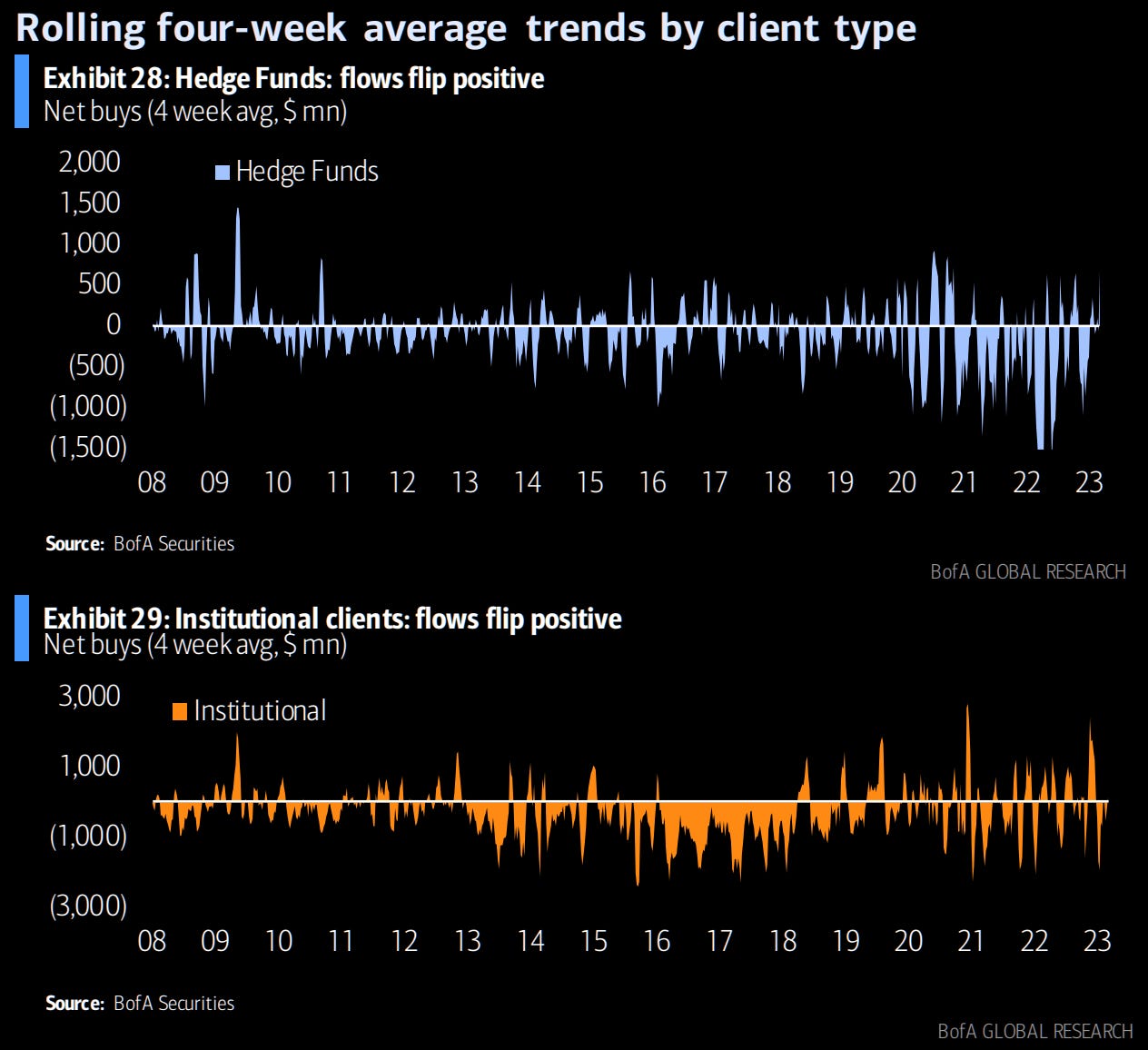

Hedge funds and institutions going long equity.

Private clients have panicked, as they are wont to do.

Buybacks have accelerated and remained healthful. Corporate client buybacks are a leading read on S&P 500 buybacks

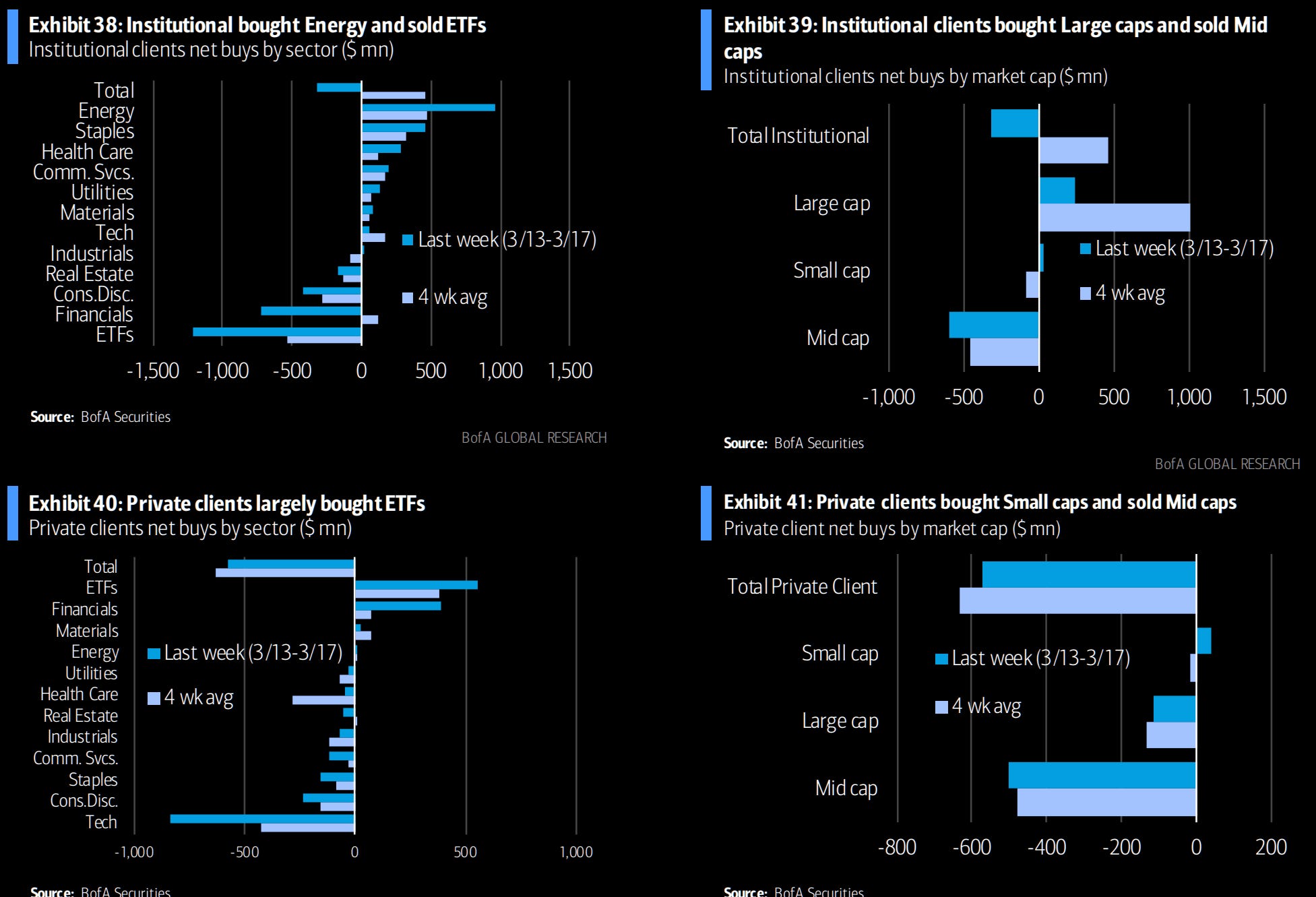

Finally, we’ve seen some interesting trends, with funds flowing into large cap names, and away from mid-caps. Financials have seen the largest inflows, but both institutional and private client flows were negative on the week.

Peroratio et Conclusio

We've observed some interesting market movements and shifts in positioning recently. From the out-of-the-money short positions that remain exposed to covering, to the continued preference for US government funds over credit funds, there's plenty to unpack. We've also seen an increased reliance on FHLBs and Fed credit facilities by larger banks, while foreign custodial holdings have experienced a decline as institutions tap into the Fed's repo facilities for liquidity.

The Federal Reserve's recent interest rate hike and the change in their guidance language signals a potential shift in monetary policy, which could have implications for the markets going forward. As we monitor these developments, it's important to stay informed and adaptable in our investing strategies.

As we wrap up this week's market commentary, I want to wish you all a pleasant weekend and continued success in your investing journeys. Remember to stay informed, be patient, and, most importantly, enjoy the process. Happy investing!

If you feel I’ve provided you with value, you can support my writing and tweets by hitting the button below, or sharing the article with your (very wealthy) friends.

All support is greatly appreciated as I am currently in the midst of an unexpected career change.

I suppose the Fed was successful at loosening the labor market, at least?

Until next time,

-Avery

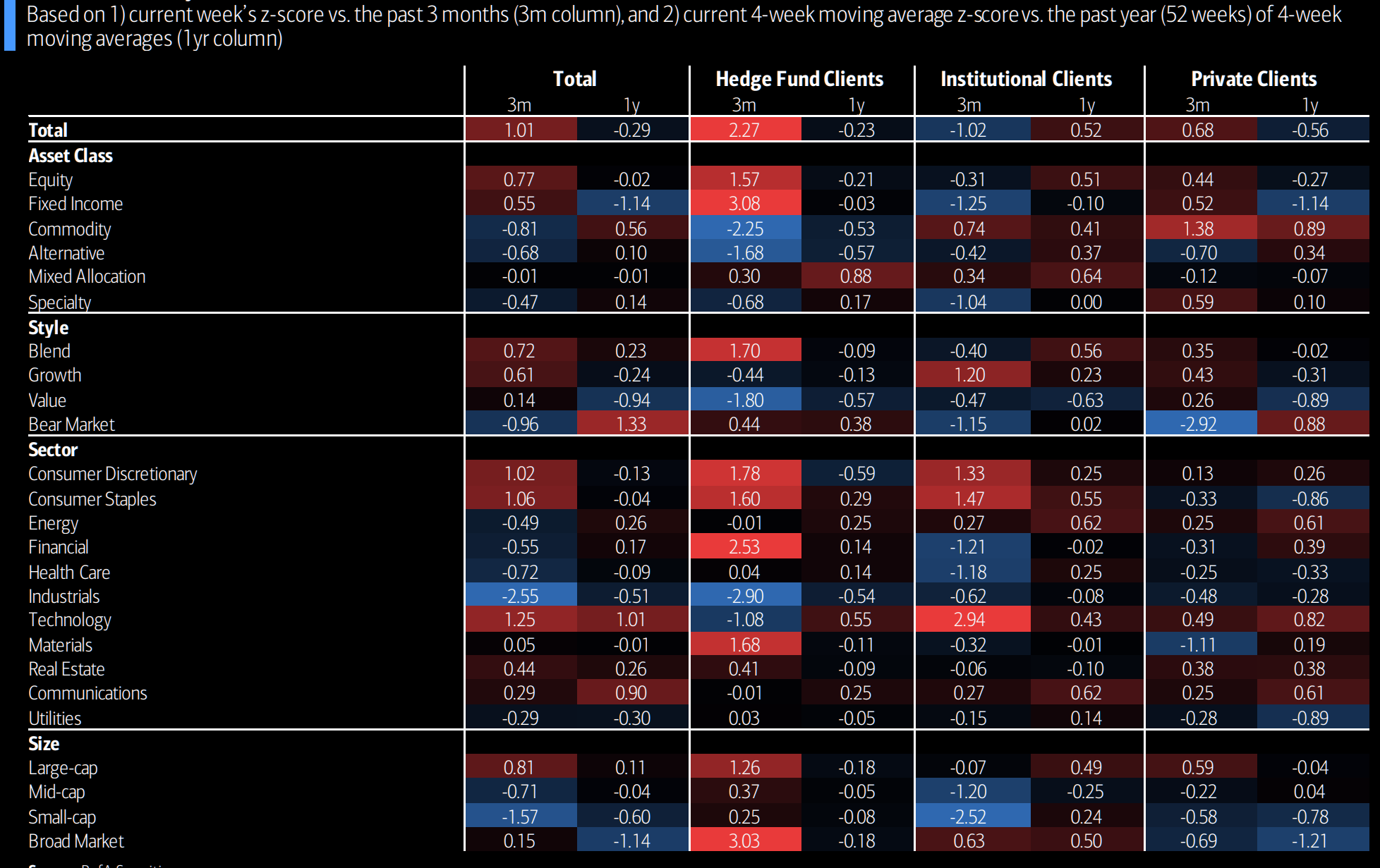

Bonus: Weekly Client ETF Flows:(z-scores as of latest week)

Great coverage as always, thank you, appreciate! Next wave in your career will come I am very confident! Have a great weekend!